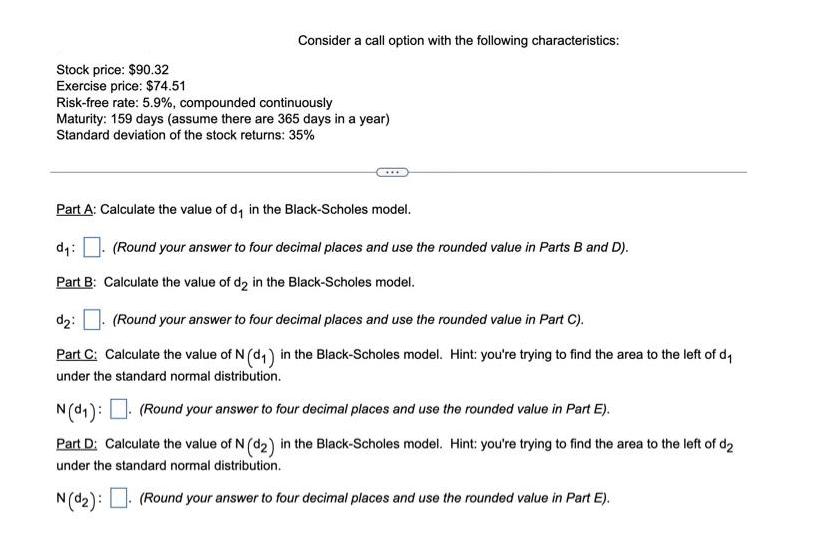

Consider a call option with the following characteristics: Stock price: $90.32 Exercise price: $74.51 Risk-free rate: 5.9%, compounded continuously Maturity: 159 days (assume there

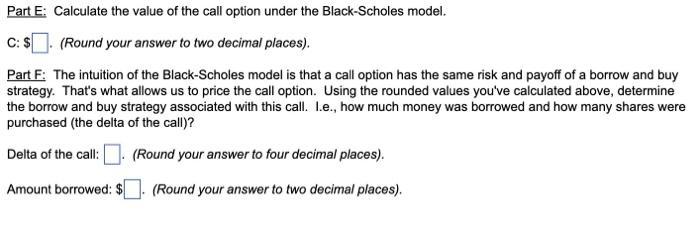

Consider a call option with the following characteristics: Stock price: $90.32 Exercise price: $74.51 Risk-free rate: 5.9%, compounded continuously Maturity: 159 days (assume there are 365 days in a year) Standard deviation of the stock returns: 35% Part A: Calculate the value of d in the Black-Scholes model. d: (Round your answer to four decimal places and use the rounded value in Parts B and D). Part B: Calculate the value of d in the Black-Scholes model. d: (Round your answer to four decimal places and use the rounded value in Part C). Part C: Calculate the value of N (d) in the Black-Scholes model. Hint: you're trying to find the area to the left of d under the standard normal distribution. N (d): (Round your answer to four decimal places and use the rounded value in Part E). Part D: Calculate the value of N (d2) in the Black-Scholes model. Hint: you're trying to find the area to the left of d2 under the standard normal distribution. N (d):. (Round your answer to four decimal places and use the rounded value in Part E). Part E: Calculate the value of the call option under the Black-Scholes model. C: $. (Round your answer to two decimal places). Part F: The intuition of the Black-Scholes model is that a call option has the same risk and payoff of a borrow and buy strategy. That's what allows us to price the call option. Using the rounded values you've calculated above, determine the borrow and buy strategy associated with this call. I.e., how much money was borrowed and how many shares were purchased (the delta of the call)? Delta of the call: (Round your answer to four decimal places). Amount borrowed: $. (Round your answer to two decimal places).

Step by Step Solution

3.43 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

The value of d is 14183 The value of d2 is 13716 The value of N d is 09087 The value of N d2 i...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Pietro Veronesi

1st edition

0470109106, 978-0470109106