Answered step by step

Verified Expert Solution

Question

1 Approved Answer

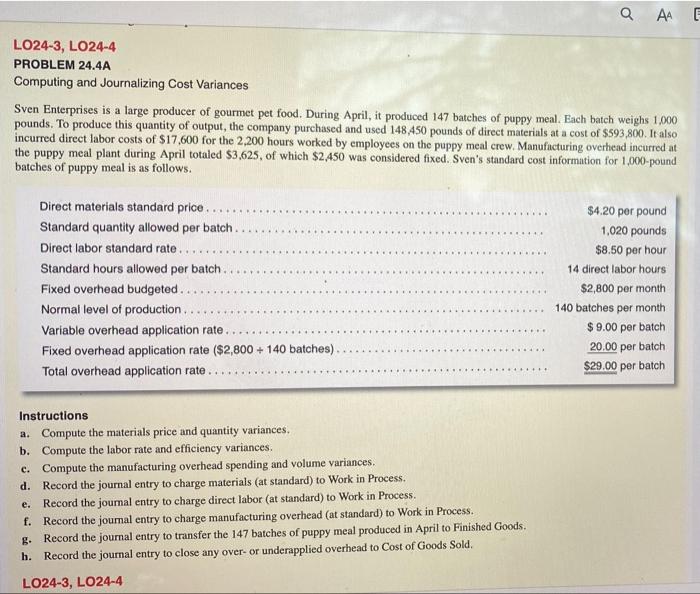

a AA LO24-3, LO24-4 PROBLEM 24.4A Computing and Journalizing Cost Variances Sven Enterprises is a large producer of gourmet pet food. During April, it produced

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

EPA Should Improve Timeliness For Resolving Audits Under Appeal

Authors: U.S. Environmental Protection Agency

1st Edition

1500105783, 978-1500105785