A, all of C, and E are my trouble spots. PLEASE SHOW ANSWERS IN AT LEAST 4 DECIMAL PLACES BECAUSE THESE ARE OFTEN QUIRKY ABOUT DECIMALS AND ROUNDING

A, all of C, and E are my trouble spots. PLEASE SHOW ANSWERS IN AT LEAST 4 DECIMAL PLACES BECAUSE THESE ARE OFTEN QUIRKY ABOUT DECIMALS AND ROUNDING

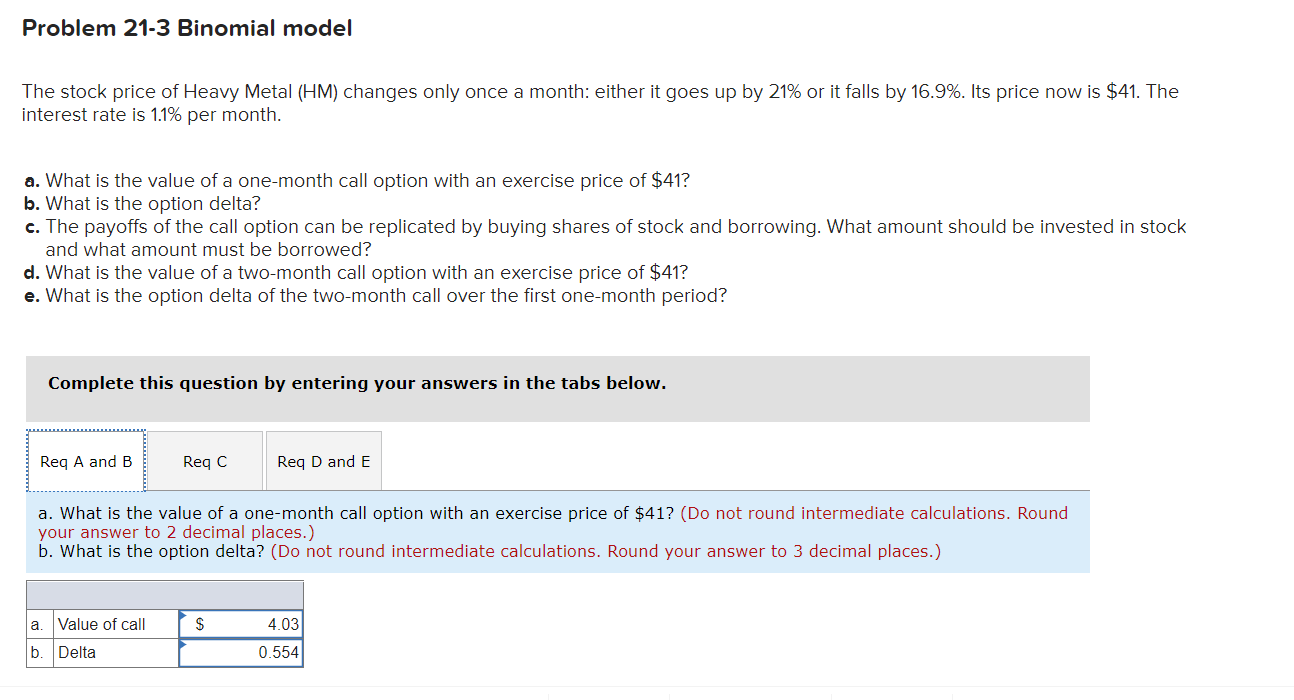

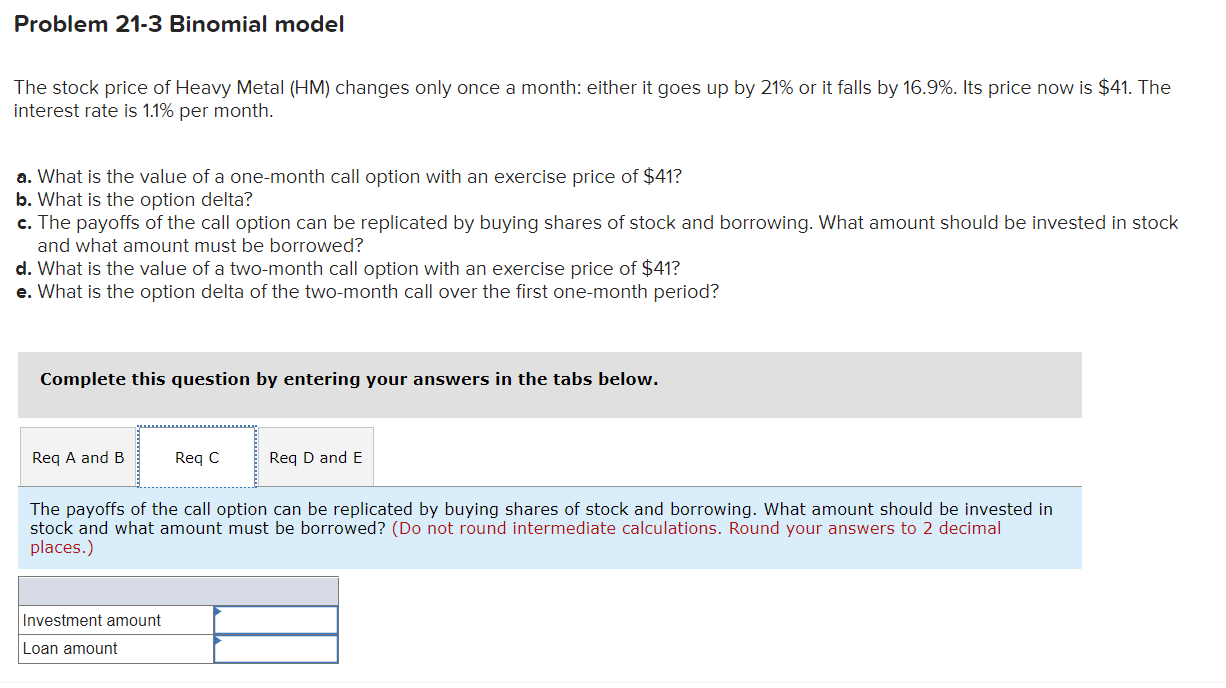

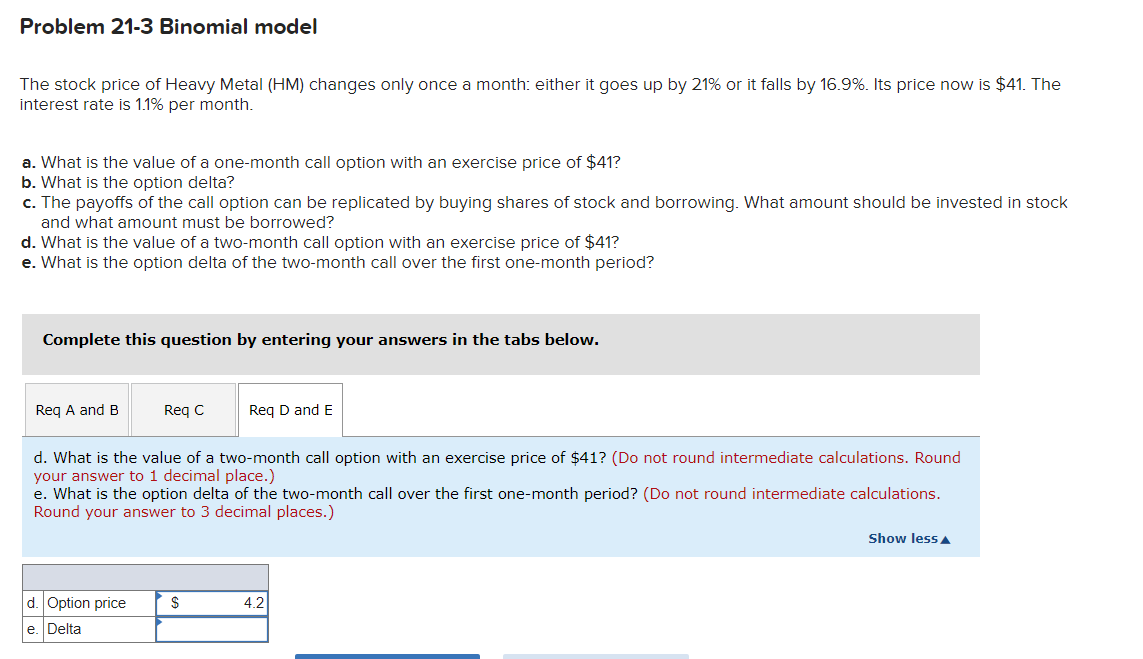

Problem 21-3 Binomial model The stock price of Heavy Metal (HM) changes only once a month: either it goes up by 21% or it falls by 16.9%. Its price now is $41. The interest rate is 1.1% per month. a. What is the value of a one-month call option with an exercise price of $41? b. What is the option delta? c. The payoffs of the call option can be replicated by buying shares of stock and borrowing. What amount should be invested in stock and what amount must be borrowed? d. What is the value of a two-month call option with an exercise price of $41? e. What is the option delta of the two-month call over the first one-month period? Complete this question by entering your answers in the tabs below. A and B Reg C D and E a. What is the value of a one-month call option with an exercise price of $41? (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. What is the option delta? (Do not round intermediate calculations. Round your answer to 3 decimal places.) a. Value of call $ 4.03 0.554 b. Delta Problem 21-3 Binomial model The stock price of Heavy Metal (HM) changes only once a month: either it goes up by 21% or it falls by 16.9%. Its price now is $41. The interest rate is 1.1% per month. a. What is the value of a one-month call option with an exercise price of $41? b. What is the option delta? c. The payoffs of the call option can be replicated by buying shares of stock and borrowing. What amount should be invested in stock and what amount must be borrowed? d. What is the value of a two-month call option with an exercise price of $41? e. What is the option delta of the two-month call over the first one-month period? Complete this question by entering your answers in the tabs below. Reg A and B Reg C Reg D and E The payoffs of the call option can be replicated by buying shares of stock and borrowing. What amount should be invested in stock and what amount must be borrowed? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Investment amount Loan amount Problem 21-3 Binomial model The stock price of Heavy Metal (HM) changes only once a month: either it goes up by 21% or it falls by 16.9%. Its price now is $41. The interest rate is 1.1% per month. a. What is the value of a one-month call option with an exercise price of $41? b. What is the option delta? c. The payoffs of the call option can be replicated by buying shares of stock and borrowing. What amount should be invested in stock and what amount must be borrowed? d. What is the value of a two-month call option with an exercise price of $41? e. What is the option delta of the two-month call over the first one-month period? Complete this question by entering your answers in the tabs below. Req A and B Reqc Reg D and E d. What is the value of a two-month call option with an exercise price of $41? (Do not round intermediate calculations. Round your answer to 1 decimal place.) e. What is the option delta of the two-month call over the first one-month period? (Do not round intermediate calculations. Round your answer to 3 decimal places.) Show less d. Option price $ 4.2 e. Delta Problem 21-3 Binomial model The stock price of Heavy Metal (HM) changes only once a month: either it goes up by 21% or it falls by 16.9%. Its price now is $41. The interest rate is 1.1% per month. a. What is the value of a one-month call option with an exercise price of $41? b. What is the option delta? c. The payoffs of the call option can be replicated by buying shares of stock and borrowing. What amount should be invested in stock and what amount must be borrowed? d. What is the value of a two-month call option with an exercise price of $41? e. What is the option delta of the two-month call over the first one-month period? Complete this question by entering your answers in the tabs below. A and B Reg C D and E a. What is the value of a one-month call option with an exercise price of $41? (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. What is the option delta? (Do not round intermediate calculations. Round your answer to 3 decimal places.) a. Value of call $ 4.03 0.554 b. Delta Problem 21-3 Binomial model The stock price of Heavy Metal (HM) changes only once a month: either it goes up by 21% or it falls by 16.9%. Its price now is $41. The interest rate is 1.1% per month. a. What is the value of a one-month call option with an exercise price of $41? b. What is the option delta? c. The payoffs of the call option can be replicated by buying shares of stock and borrowing. What amount should be invested in stock and what amount must be borrowed? d. What is the value of a two-month call option with an exercise price of $41? e. What is the option delta of the two-month call over the first one-month period? Complete this question by entering your answers in the tabs below. Reg A and B Reg C Reg D and E The payoffs of the call option can be replicated by buying shares of stock and borrowing. What amount should be invested in stock and what amount must be borrowed? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Investment amount Loan amount Problem 21-3 Binomial model The stock price of Heavy Metal (HM) changes only once a month: either it goes up by 21% or it falls by 16.9%. Its price now is $41. The interest rate is 1.1% per month. a. What is the value of a one-month call option with an exercise price of $41? b. What is the option delta? c. The payoffs of the call option can be replicated by buying shares of stock and borrowing. What amount should be invested in stock and what amount must be borrowed? d. What is the value of a two-month call option with an exercise price of $41? e. What is the option delta of the two-month call over the first one-month period? Complete this question by entering your answers in the tabs below. Req A and B Reqc Reg D and E d. What is the value of a two-month call option with an exercise price of $41? (Do not round intermediate calculations. Round your answer to 1 decimal place.) e. What is the option delta of the two-month call over the first one-month period? (Do not round intermediate calculations. Round your answer to 3 decimal places.) Show less d. Option price $ 4.2 e. Delta