Answered step by step

Verified Expert Solution

Question

1 Approved Answer

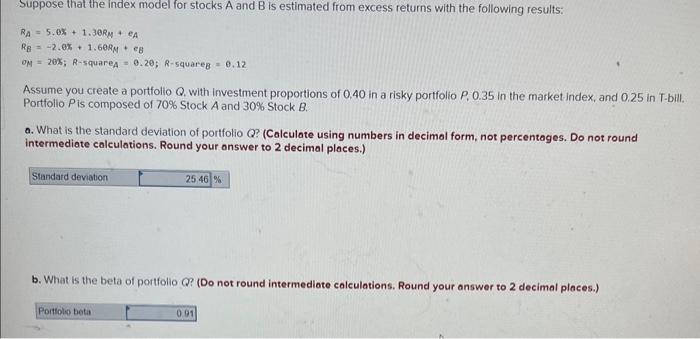

A and B are correct C is not RA=5.0%+1.30RM+eARB=2.05+1.60BM+eBoM=20%;RsquareA=0.2;R5qqareB=0.12 Assume you create a portfolio Q. with investment proportions of 0.40 in a risky portfolio P,0.35

A and B are correct C is not

RA=5.0%+1.30RM+eARB=2.05+1.60BM+eBoM=20%;RsquareA=0.2;R5qqareB=0.12 Assume you create a portfolio Q. with investment proportions of 0.40 in a risky portfolio P,0.35 in the market index, and 0.25 in T-bill. Portfollo Pis composed of 70% Stock A and 30% Stock B a. What is the standard deviation of portfolio Q ? (Calculate using numbers in decimal form, not percentages. Do not round intermediate calculations. Round your onswer to 2 decimal places.) b. What is the beta of portfolio Q? (Do not round intermediate calculations. Round your answer to 2 decimal places.) c. What is the "firm-specific" risk of portfolio Q? (Calculate using numbers in decimal form, not intermediate calculations. Round your answer to 4 decimal places.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of State Capitalism And The Firm

Authors: Mike Wright, Geoffrey T. Wood, Alvaro Cuervo-Cazurra, Pei Sun, Ilya Okhmatovskiy, Anna Grosman

1st Edition

0198837364, 978-0198837367