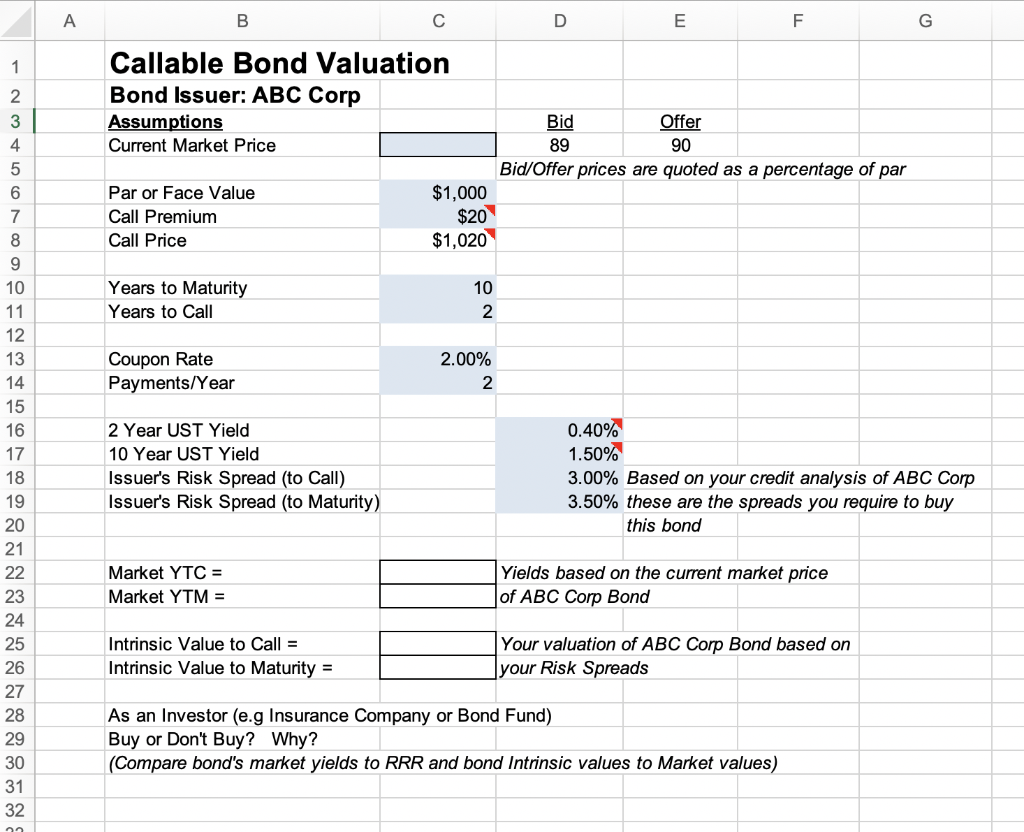

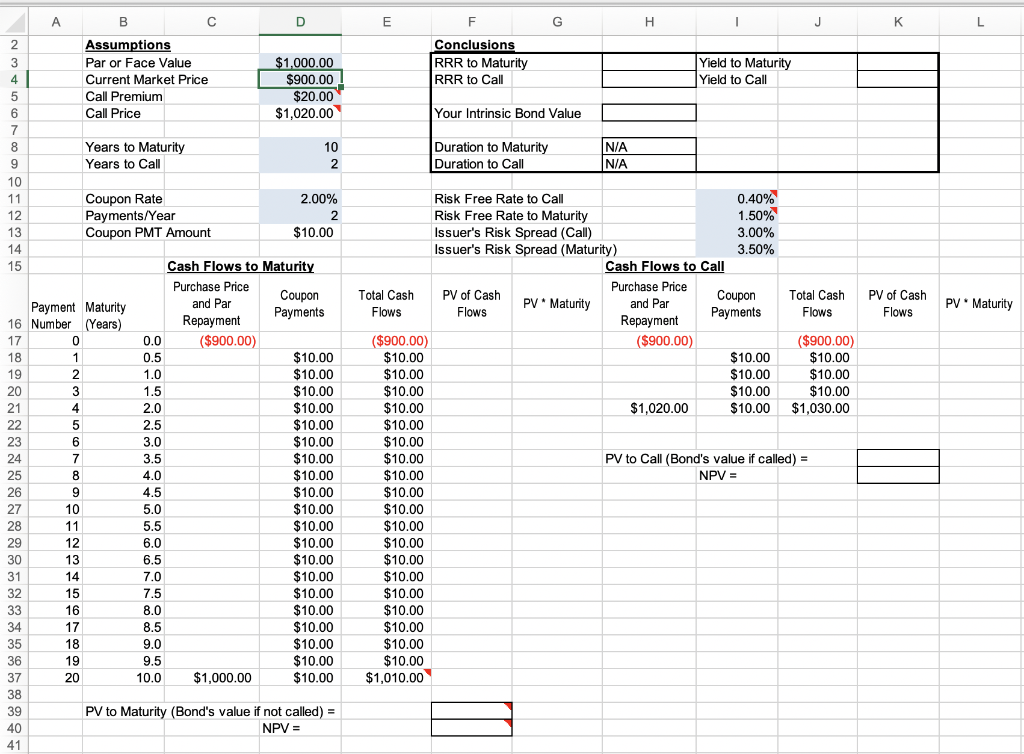

A B D E F G 1 Callable Bond Valuation Bond Issuer: ABC Corp Assumptions Current Market Price Bid Offer 89 90 Bid/Offer prices are quoted as a percentage of par $1,000 Par or Face Value Call Premium Call Price $20 $1,020 Years to Maturity Years to Call 10 2 Coupon Rate Payments/Year 2.00% 2 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 2 Year UST Yield 10 Year UST Yield Issuer's Risk Spread (to Call) Issuer's Risk Spread (to Maturity) 0.40% 1.50% 3.00% Based on your credit analysis of ABC Corp 3.50% these are the spreads you require to buy this bond Market YTC = Market YTM = Yields based on the current market price of ABC Corp Bond Intrinsic Value to Call = Intrinsic Value to Maturity = Your valuation of ABC Corp Bond based on your Risk Spreads As an Investor (e.g Insurance Company or Bond Fund) Buy or Don't Buy? Why? (Compare bond's market yields to RRR and bond Intrinsic values to Market values) A B C D E G H J K L F Conclusions RRR to Maturity RRR to Call Yield to Maturity Yield to Call Your Intrinsic Bond Value Duration to Maturity Duration to Call N/A N/A PV of Cash Flows PV Maturity Flows 2 Assumptions 3 Par or Face Value $1,000.00 4 Current Market Price $900.00 5 Call Premium $20.00 6 Call Price $1,020.00 7 8 Years to Maturity 10 9 Years to Call 2 10 11 Coupon Rate 2.00% 12 Payments/Year 2 13 Coupon PMT Amount $10.00 14 15 Cash Flows to Maturity Purchase Price Coupon Payment Maturity and Par Payments Repayment 16 Number (Years) 17 0 0.0 ($900.00) 18 1 0.5 $10.00 19 2 1.0 $10.00 20 3 1.5 $10.00 21 4 2.0 $10.00 22 5 2.5 $10.00 23 6 3.0 $10.00 24 7 3.5 $10.00 25 8 4.0 $10.00 26 9 9 4.5 $10.00 27 10 5.0 $10.00 28 11 5.5 $10.00 29 12 6.0 $10.00 30 13 6.5 $10.00 31 14 7.0 $10.00 32 15 7.5 $10.00 33 16 8.0 $10.00 34 17 8.5 $10.00 35 18 9.0 $10.00 36 19 9.5 $10.00 37 20 10.0 $1,000.00 $10.00 38 39 PV to Maturity (Bond's value if not called) = 40 NPV = 41 Risk Free Rate to Call 0.40% Risk Free Rate to Maturity 1.50% Issuer's Risk Spread (Call) 3.00% Issuer's Risk Spread (Maturity) 3.50% Cash Flows to Call Total Cash PV of Cash Purchase Price PV * Maturity Total Cash Coupon and Par Flows Flows Payments Repayment ($900.00) ($900.00) ($900.00) $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $1,020.00 $10.00 $1,030.00 $10.00 $10.00 $10.00 PV to Call (Bond's value if called) = $10.00 NPV = $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $1,010.00 8 A B D E F G 1 Callable Bond Valuation Bond Issuer: ABC Corp Assumptions Current Market Price Bid Offer 89 90 Bid/Offer prices are quoted as a percentage of par $1,000 Par or Face Value Call Premium Call Price $20 $1,020 Years to Maturity Years to Call 10 2 Coupon Rate Payments/Year 2.00% 2 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 2 Year UST Yield 10 Year UST Yield Issuer's Risk Spread (to Call) Issuer's Risk Spread (to Maturity) 0.40% 1.50% 3.00% Based on your credit analysis of ABC Corp 3.50% these are the spreads you require to buy this bond Market YTC = Market YTM = Yields based on the current market price of ABC Corp Bond Intrinsic Value to Call = Intrinsic Value to Maturity = Your valuation of ABC Corp Bond based on your Risk Spreads As an Investor (e.g Insurance Company or Bond Fund) Buy or Don't Buy? Why? (Compare bond's market yields to RRR and bond Intrinsic values to Market values) A B C D E G H J K L F Conclusions RRR to Maturity RRR to Call Yield to Maturity Yield to Call Your Intrinsic Bond Value Duration to Maturity Duration to Call N/A N/A PV of Cash Flows PV Maturity Flows 2 Assumptions 3 Par or Face Value $1,000.00 4 Current Market Price $900.00 5 Call Premium $20.00 6 Call Price $1,020.00 7 8 Years to Maturity 10 9 Years to Call 2 10 11 Coupon Rate 2.00% 12 Payments/Year 2 13 Coupon PMT Amount $10.00 14 15 Cash Flows to Maturity Purchase Price Coupon Payment Maturity and Par Payments Repayment 16 Number (Years) 17 0 0.0 ($900.00) 18 1 0.5 $10.00 19 2 1.0 $10.00 20 3 1.5 $10.00 21 4 2.0 $10.00 22 5 2.5 $10.00 23 6 3.0 $10.00 24 7 3.5 $10.00 25 8 4.0 $10.00 26 9 9 4.5 $10.00 27 10 5.0 $10.00 28 11 5.5 $10.00 29 12 6.0 $10.00 30 13 6.5 $10.00 31 14 7.0 $10.00 32 15 7.5 $10.00 33 16 8.0 $10.00 34 17 8.5 $10.00 35 18 9.0 $10.00 36 19 9.5 $10.00 37 20 10.0 $1,000.00 $10.00 38 39 PV to Maturity (Bond's value if not called) = 40 NPV = 41 Risk Free Rate to Call 0.40% Risk Free Rate to Maturity 1.50% Issuer's Risk Spread (Call) 3.00% Issuer's Risk Spread (Maturity) 3.50% Cash Flows to Call Total Cash PV of Cash Purchase Price PV * Maturity Total Cash Coupon and Par Flows Flows Payments Repayment ($900.00) ($900.00) ($900.00) $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $1,020.00 $10.00 $1,030.00 $10.00 $10.00 $10.00 PV to Call (Bond's value if called) = $10.00 NPV = $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $10.00 $1,010.00 8