Question

A bank has written $10M European call option on one stock and $10M European put option on another stock. For the first option, the stock

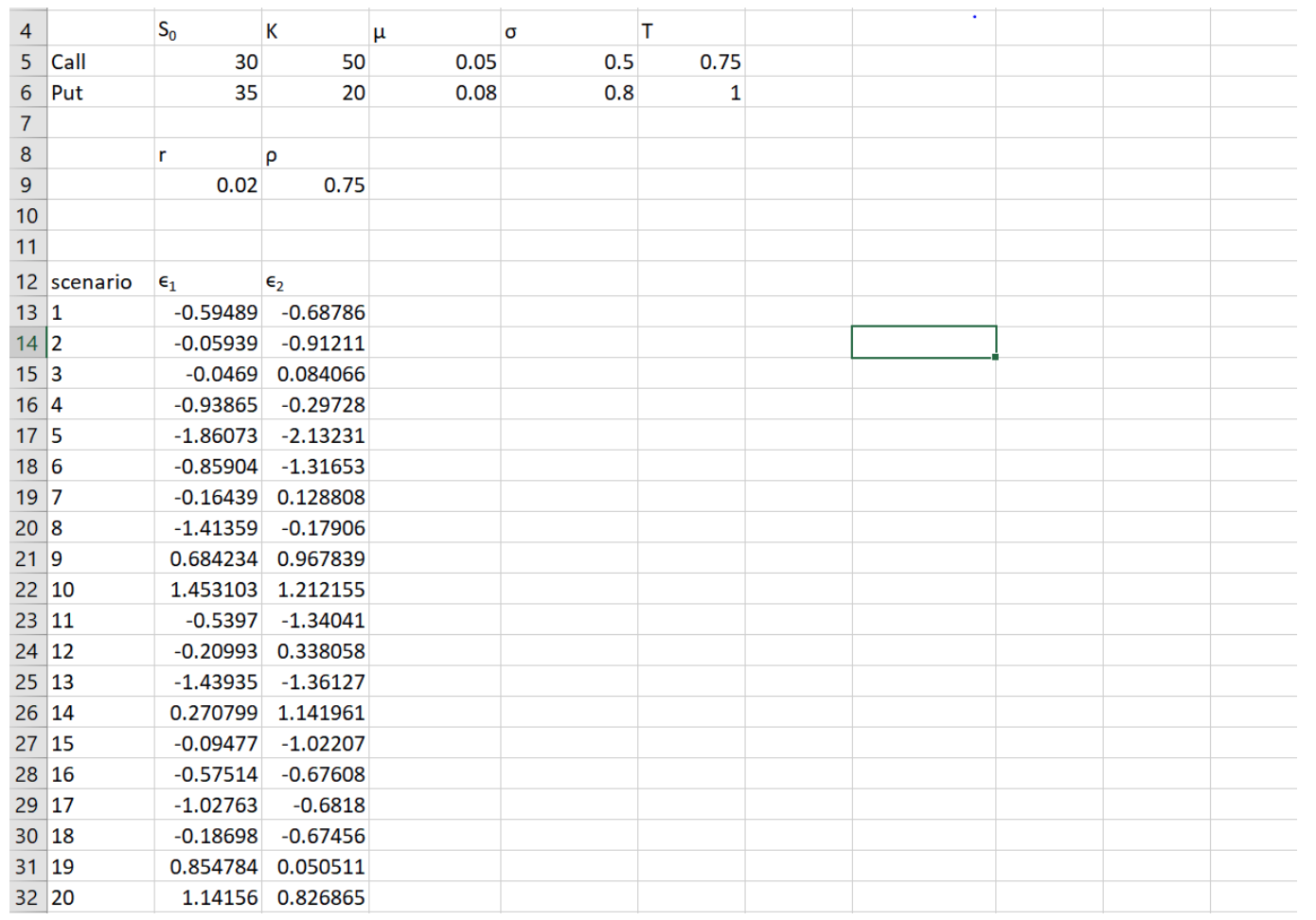

A bank has written $10M European call option on one stock and $10M European put option on another stock. For the first option, the stock price is 30, the strike price is 50, the expected return is 5% per annum, the volatility is 50% per annum, and the time to maturity is nine months. For the second option, the stock price is 35, the strike price is 20, the expected return is 8% per annum, the volatility is 80% per annum, and the time to maturity is one year. Neither stock pays a dividend, the risk-free rate is 2% per annum, and the correlation between stocks log returns is 0.75.

a. Plot the distribution of the profit/loss in 10 days as a histogram by using Monte Carlo simulation

b. Estimate the 10-day 99% VaR

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Issues In Behavioral Finance

Authors: Simon Grima

1st Edition

1787698823, 978-1787698826