Question

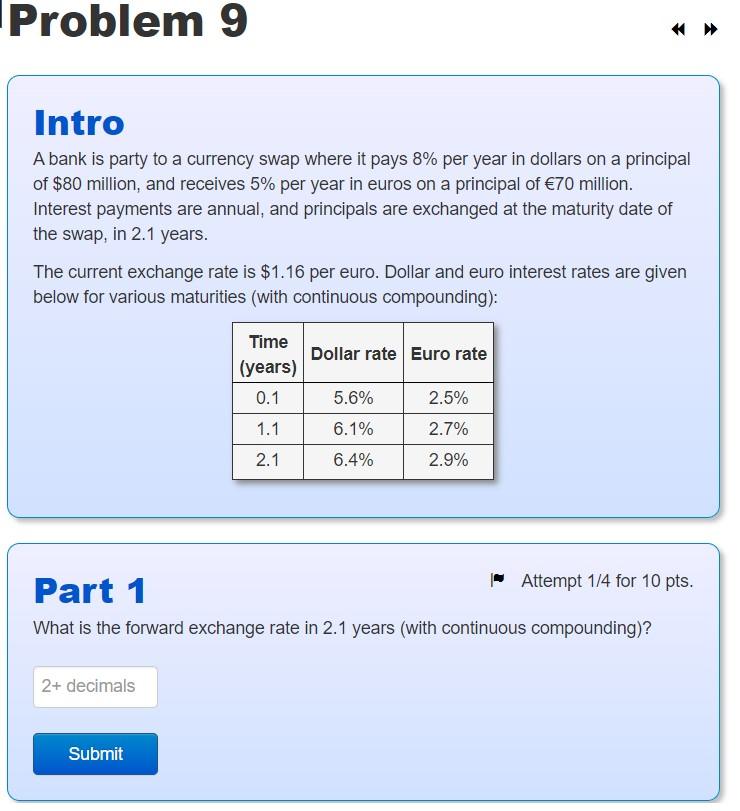

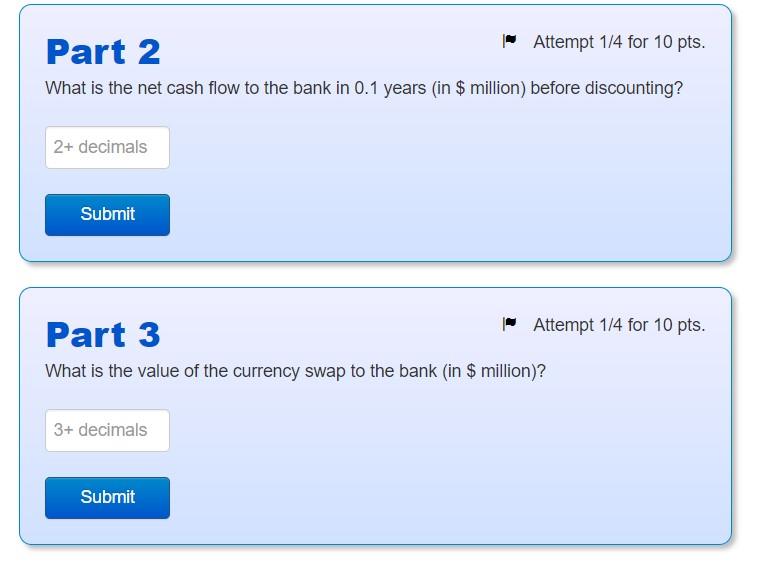

A bank is party to a currency swap where it pays 8% per year in dollars on a principal of $80 million, and receives 5%

A bank is party to a currency swap where it pays 8% per year in dollars on a principal of $80 million, and receives 5% per year in euros on a principal of 70 million. Interest payments are annual, and principals are exchanged at the maturity date of the swap, in 2.1 years. The current exchange rate is $1.16 per euro. Dollar and euro interest rates are given below for various maturities (with continuous compounding):

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Why Bitcoin

Authors: Tomer Strolight

1st Edition

9916697957, 978-9916697955