a) Based on the case, indicate the type of audit opinion you would issue, as well as the reasons for issuing the particular audit opinion.

b) Based on the case, provide four (4) factors that indicate Bloktastic satisfies the going concern assumption

c) explain if bloktastic satisfies going concern or not , give at least 4 points for both and justify answer

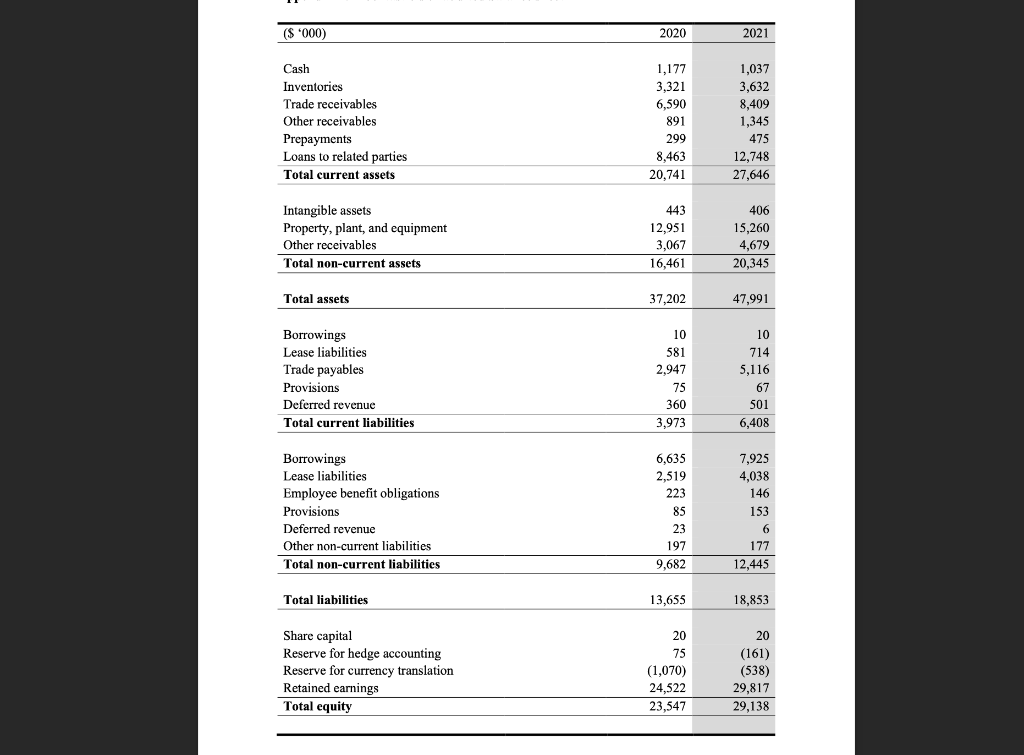

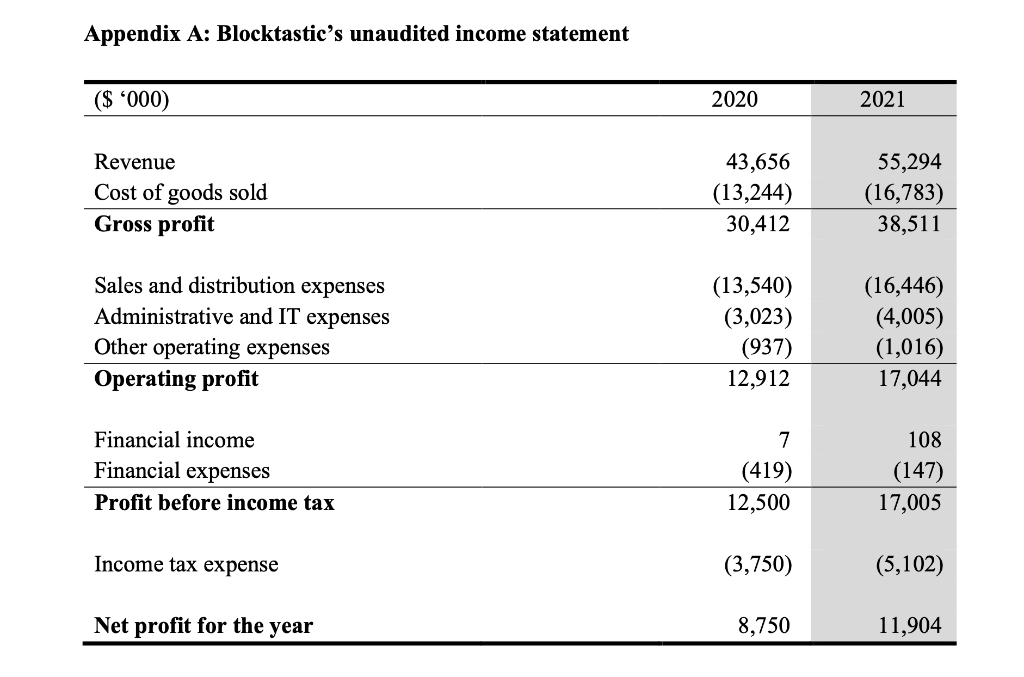

($ '000) Cash Inventories Trade receivables Other receivables Prepayments Loans to related parties Total current assets Intangible assets Property, plant, and equipment Other receivables Total non-current assets Total assets Borrowings Lease liabilities Trade payables Provisions Deferred revenue Total current liabilities Borrowings Lease liabilities Employee benefit obligations Provisions Deferred revenue Other non-current liabilities Total non-current liabilities Total liabilities Share capital Reserve for hedge accounting Reserve for currency translation Retained earnings Total equity 2020 1,177 3,321 6,590 891 299 8,463 20,741 443 12,951 3,067 16,461 37,202 10 581 2,947 75 360 3,973 6,635 2,519 223 85 23 197 9,682 13,655 20 75 (1,070) 24,522 23,547 2021 1,037 3,632 8,409 1,345 475 12,748 27,646 406 15,260 4,679 20,345 47,991 10 714 5,116 67 501 6,408 7,925 4,038 146 153 6 177 12,445 18,853 20 (161) (538) 29,817 29,138 Appendix A: Blocktastic's unaudited income statement ($ '000) Revenue Cost of goods sold Gross profit Sales and distribution expenses Administrative and IT expenses Other operating expenses Operating profit Financial income Financial expenses Profit before income tax Income tax expense Net profit for the year 2020 43,656 (13,244) 30,412 (13,540) (3,023) (937) 12,912 7 (419) 12,500 (3,750) 8,750 2021 55,294 (16,783) 38,511 (16,446) (4,005) (1,016) 17,044 108 (147) 17,005 (5,102) 11,904 Audit of Blocktastic Proprietary Limited for fiscal year ending 30 June 2021 (1) Company overview Blocktastic is a proprietary limited company that manufactures and retails toys, mainly consisting of interlocking plastic bricks. The company was founded in 2000 by Thomas Kirk, who is the current Chairperson and CEO of the company. The company first started as a small toy store in Melbourne selling hand-crafted wooden toys. More than 20 years on, the company now operates a large manufacturing plant in Truganina (a suburb about 20 kilometres from Melbourne) and multiple retail outlets throughout Australia. Blocktastic is a well-established company in a very competitive toy industry. The company competes with multiple established manufacturers and retailers, all of which have well recognised brand names. Blocktastic main competitors in the Australian plastic brick toy segment are PlayWell and LeleGo. To reduce production costs, Blocktastic imports its plastic raw materials from multiple countries depending on which supplier has the lowest price at time of purchase. Some of the purchase contracts are priced in US dollars while others are price in the supplier's domestic currency. While sourcing cheap plastic raw materials has improved profitability, the cost reduction focus has resulted in some issues for Blocktastic across the years. Most recently, in mid-June 2021, Blocktastic has had complaints about children getting sick after accidentally placing the bricks in their mouths. This has led to an immediate recall of some of its products that was manufactured using a contaminated batch of plastic. The recall still on going at the end of the fiscal year. Blocktastic sells its products in its own retail stores as well as other authorised distributors. To allow their own retail outlets to remain popular among buyers, Blocktastic has a number of exclusive products at those stores. Total sales from authorised retail stores make up about 40% of Blocktastic's annual sales. Blocktastic distributes to those authorised retail stores where Page 1 of 11 some of the stock is sold to the retailers while others are held on consignment. Major authorised distributors include large department stores such as Myer and David Jones, as well as speciality toy stores such as ToysRus. Sales information from the authorised distributors are transferred to Blocktastic with a lag of up to two weeks. Blocktastic has a mix of full-time and casual employees. Most of the full-time employees work at the manufacturing plant, while casual employees are typically based at the retail stores. There is a high volume of casual employee recruitments during the busy times to support the increase in workload. The casual employees hired during the peak periods are usually sales assistants at the retail stores or truck drivers at the manufacturing plant. There are various industrial awards (set by the Fair Work Ombudsman) that outline the salary and wage conditions of Blocktastic's employees, depending on whether they are permanent or casual and whether they work at the retail store or manufacturing plant. For example, casual employees do not receive annual or long-service leave entitlements and workers at the manufacturing plant get an extra compensation as hazard pay. (2) Senior management and directors at Blocktastic The top management team at Blocktastic are: Thomas Kirk, CEO John Lemon, CFO Ariana Ventia, COO Thomas has led the management team at Blocktastic since he founded the company 2000 John and Ariana are his best friends since university when they were all studying at the London Business School. They work very well together and have always made important decisions as a team. Thomas is very friendly to everyone, including the auditors. He frequently gives the auditors gifts including limited edition, exclusive block toys that are very expensive on the secondary market. These are the same gifts that all employees receive at the end of the year for all their hard work. Blocktastic's board consists of the following 3 directors: Thomas Kirk, Chairperson Page 2 of 11 Taylor Zwift, Independent director Leonardo Carpaccio, Independent director Thomas is the chairperson, along with two other independent directors. Board meetings are held once every quarter to discuss all the pertinent issues. As Blocktastic does not have a large board of directors, they do not have separate committees. Instead, issues relating to, for example, compensation, risk, and audit, are reviewed together during the board meetings. As part of the corporate governance function, Blocktastic also has an internal audit team. The internal audit team is deployed by senior management and the board of directors in the broad areas of evaluating risks and controls, evaluating compliance, and performing financial and operational auditing. Through these activities, internal auditors contribute to effective corporate governance within Blocktastic. (3) Financial performance Overall, 2021 was an exceptional year for Blocktastic (see draft financial statements in Appendix A and B). Revenue and profit hit double-digit growth, even with extensive investments in long-term development. Significant growth in sales that eclipsed the industry's growth was driven by a strong and diverse portfolio of brick toys and strong retailer partnerships. Revenue for the full year increased by about 27%, even with strong exchange rate headwinds. This continued revenue growth demonstrates a strong consumer demand for the Blocktastic's toys across builders of all ages and interests. In 2021, Blocktastic made significant investments that are designed to deliver long-term growth. This included increased marketing to enhance brand awareness, expanding the number of Blocktastic branded stores in Australia and increasing manufacturing capacity. Main financial ratios such as operating margin, profit margin and return on equity all improved compared to 2020. Despite this, Blocktastic is still planning to raise more private equity funds and Thomas will be asking the current audit partner to speak at an investor conference with the aim of convincing private equity funds to invest in Blocktastic. Thomas wants the current audit partner to assure the managers of private equity funds that their audit firm is the best and that Page 3 of 11 no other audit firm can do proper audits. This would help to reinforce the financial performance of Blocktastic. (4) Auditor overview James and Partners is a mid-tier accounting firm with multiple offices across Australia. They provide a range of services including audit, assurance, consulting, and tax services. Their assurance team is known for a wide range of services, from providing audits of listed firms, assurance for not-for-profits, review of integrated reports, to reports of factual findings. James and Partners' Melbourne office has 10 partners providing audit and assurance services. Robert, the managing partner of the Melbourne office, is also the engagement partner for Blocktastic. This is the first year James and Partners are the auditors of Blocktastic. To attract Blocktastic as a new client, Robert placed a quote for audit fees that was obviously too low for the audit of a firm of Blocktastic's size. This resulted in a very tight schedule to complete the audit and thus audit associates were left without supervision and did not have their work reviewed. In addition, Blocktastic's CFO, John, was also pressurising the audit team to reduce the audit fees by any means possible. To help the audit proceed smoothly, Michael was also hired join the audit team. Michael was previously the Accounting Manager at Blocktastic and his addition to the team in January 2021 has helped the audit tremendously. Robert's son really likes playing with Blocktastic bricks and enjoys displaying them in his room as well. To get his son excited for future birthday presents, Robert told his son all the new sets that would be releasing at the end of the year from the information he has received during his time at Blocktastic. This was exciting news as these sets were yet to be announced publicly. Further, given that his son loves Blocktastic toys, Robert wants the audit to proceed without any complications with management and intends to give an unmodified opinion. (5) Understanding and testing controls To guide the audit intern on the team, Robert outlined the process to identify the controls to be tested at Blocktastic. James and Partners use a top-down, risk-based approach to accomplish this. Starting with identifying the entity-level controls, the audit team then moves on to identify the significant accounts and disclosures. This helps them understand where the likely sources Page 4 of 11 of misstatements are. Based on this information, the audit team then selects which controls to test. Robert emphasised that the most critical aspect of this entire process is that the audit team must have an in-depth knowledge and understanding of Blocktastic. Without a clear understanding of the Blocktastic, it is not possible to effectively identify which controls to test as part of the audit. Robert also highlighted that the audit team does not need to test all controls only controls that are important to the audit opinion. Those controls are often referred to as "key" controls and can be preventive controls, detective controls, or a combination of both. Robert concluded by stating that identifying the controls to be tested requires professional judgment and lots of experience. Below are some examples of controls at Blocktastic documented after through discussions with entity personnel and review of entity documents: Control 1: The accounting team at Blocktastic reconciles the accounts receivable subsidiary ledger to the general ledger using a monthly reconciliation process and passed to the team's manager for review. The audit team is relying heavily on the operating effectiveness of this control. Control 2: Before generating an invoice, Blocktastic's computer system performs a three-way match of the customer order, shipping order, and bill of lading. As this control takes place for every invoice, it is performed very often. Control 3: The cash payments team at Blocktastic make a cash disbursement only after they have matched the vendor invoice to the receiving report and purchase order. Those documents would be attached together and marked as paid. As this control takes place for every cash disbursement, it is performed very often. Control 4: Blocktastic has a policy of numbering all suppliers' invoices using pre- numbered vouchers. This control works with a number of other controls to ensure all purchases are recorded. Page 5 of 11 (6) Substantive tests The overall objective of substantive procedures is to determine whether the underlying accounting records contain material misstatements and to derive an appropriate audit opinion. Robert stressed that finding an appropriate combination of audit procedures to minimise an engagement's audit risk at an acceptable cost is important for James and Partners to remain profitable. He emphasised that the audit program should match the nature, timing, and extent of substantive procedures to the audit risk model. There are many different types of substantive procedures to choose from, including analytical procedures, tests of key items, representative sampling, tests of underlying transactions and data, and using computers to assist in performing substantive procedures. There are also various levels of audit evidence that the audit team can obtain from the various substantive procedures. Importantly, the audit team must be able to conclude whether the accounts being audited are materially misstated or not. Among the many common substantive procedures performed are bank and debtor confirmations. Appendix C and D provides examples of the bank and debtor confirmation request letters. (7) Subsequent events In the briefing relating to subsequent events, Robert noted that while Blocktastic's financial report is prepared on the basis of conditions existing at the end of the fiscal year, significant events, can occur after the end of the fiscal year that, unless included in the financial report or disclosed appropriately, could make Blocktastic's financial report misleading. These events could both favourable and unfavourable to Blocktastic. To perform the subsequent events review, Robert planned the following procedures that are to be performed nearer to the date he will sign the audit report: Reading minutes of the meetings of Blocktastic's top management and the board of directors held after year-end and inquiring about matters discussed at meetings for which minutes are not available. Reading and analysing Blocktastic's latest available interim financial report and cash flow forecasts. Extending analytical procedures performed during Blocktastic's audit to include the latest available period. Page 6 of 11 Enquiring and extending previous written enquiries of the Blocktastic's legal counsel concerning any litigation and claims. . Assessing Blocktastic's continued compliance with any borrowing limits and loan covenants. Enquiring of those charged with governance at Blocktastic as to whether any subsequent events have occurred that might affect the financial report. (8) Engagement wrap-up Robert is yet to decide on the audit opinion for the 2021 audit of Blocktastic. An example of an unmodified audit opinion would look like the following: We have audited the financial report of Blocktastic Pty. Ltd. (the Company), which comprises the statement of financial position as of 30 June 2021, the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies, and the directors' declaration. In our opinion, the financial report of Blocktastic Pty. Ltd is in accordance with the Corporations Act 2001, including: a. giving a true and fair view of the Company's financial position as of 30 June 2021 and of its performance for the year then ended; and b. complying with Australian Accounting Standards and the Corporations Regulations 2001. Before he makes his decision on the audit opinion, Robert called for a team meeting to evaluate all the audit evidence gathered throughout the audit. Robert also wants the audit team to consider the appropriateness of management's use of the going concern assumption in the preparation of the financial report, including any material uncertainties about the Blocktastic's ability to continue as a going concern tha to be disclosed in the financial report. This is important as the going c assumption is a fundamental principle in the preparation of the financial report. Page 7 of 11