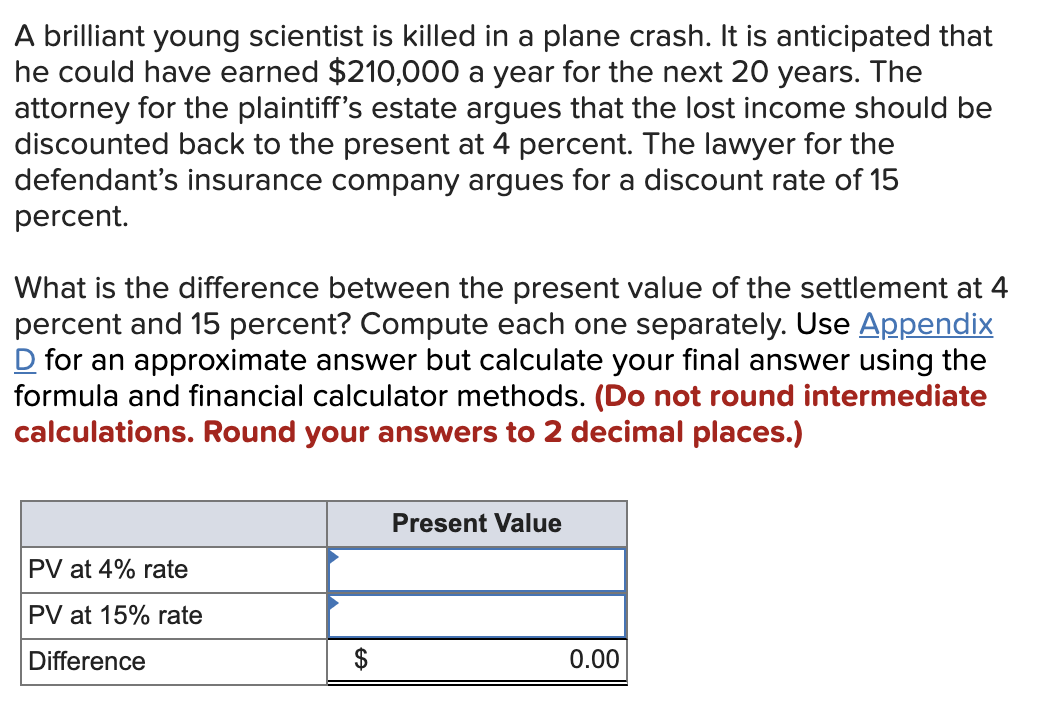

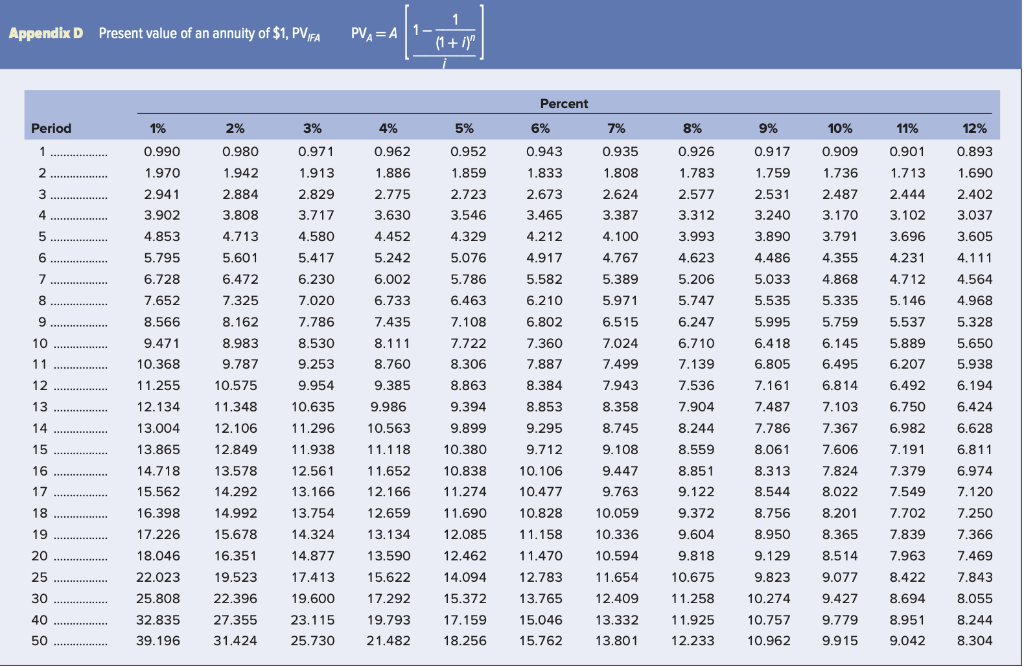

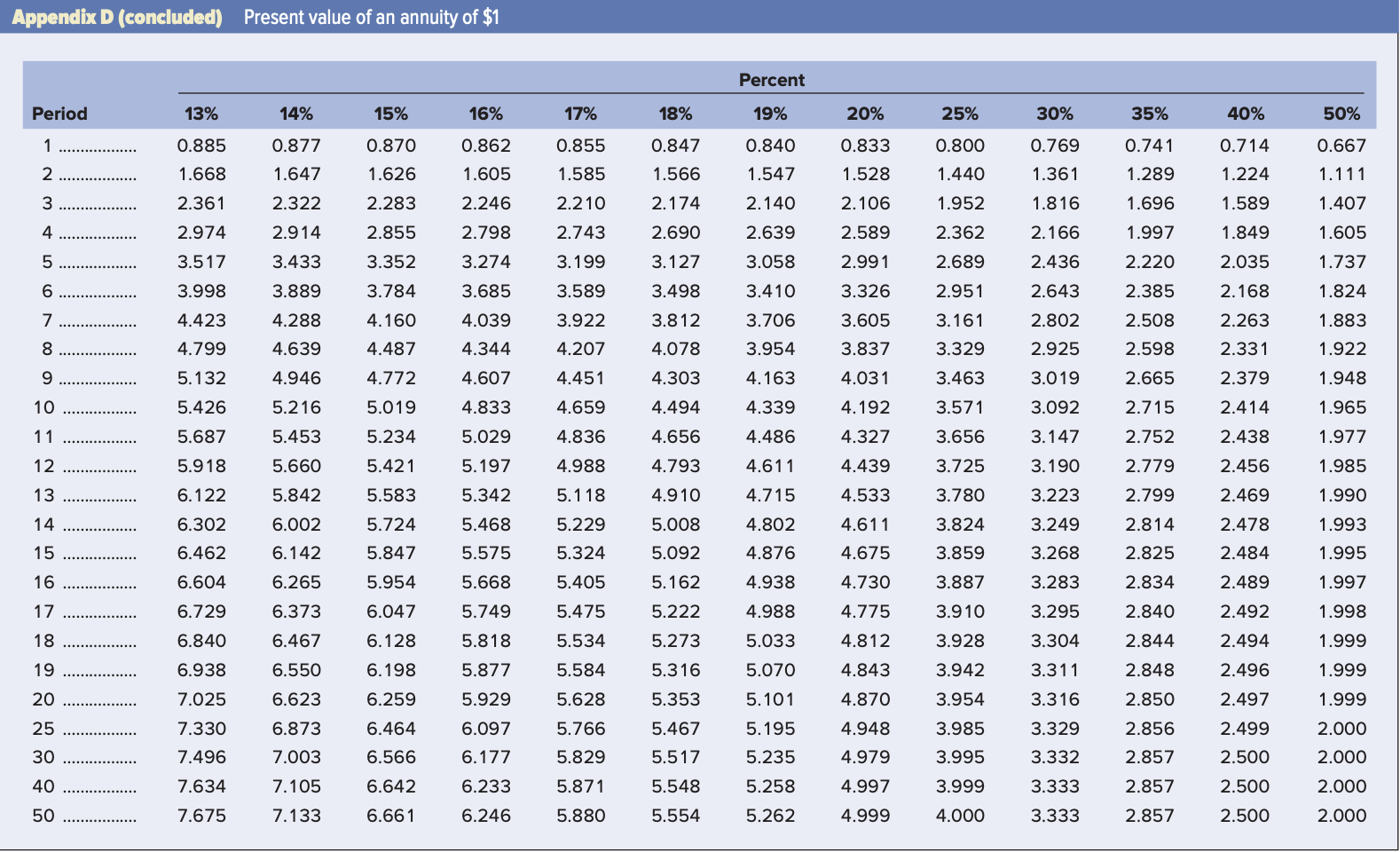

A brilliant young scientist is killed in a plane crash. It is anticipated that he could have earned $210,000 a year for the next 20 years. The attorney for the plaintiff's estate argues that the lost income should be discounted back to the present at 4 percent. The lawyer for the defendant's insurance company argues for a discount rate of 15 percent. What is the difference between the present value of the settlement at 4 percent and 15 percent? Compute each one separately. Use Appendix D for an approximate answer but calculate your final answer using the formula and financial calculator methods. (Do not round intermediate calculations. Round your answers to 2 decimal places.) Present Value PV at 4% rate PV at 15% rate Difference 0.00 Appendix D Present value of an annuity of $1, PVFA PVA=A (1+1) Percent 1% 8% 9% 10% 11% 12% Period 1 2 4% 0.962 5% 0.952 1.859 0.926 0.909 0.901 0.893 0.917 1.759 1.690 0.990 1.970 2.941 3.902 4.853 3% 0.971 1.913 2.829 3.717 4.580 3 6% 0.943 1.833 2.673 3.465 4.212 2.531 2% 0.980 1.942 2.884 3.808 4.713 5.601 6.472 7.325 8.162 1.886 2.775 3.630 4.452 5.242 4 1.713 2.444 3.102 7% 0.935 1.808 2.624 3.387 4.100 4.767 5.389 5.971 2.402 3.037 3.605 5 6 5.417 7 6.002 4.917 5.582 6.210 1.736 2.487 3.170 3.791 4.355 4.868 5.335 5.759 6.145 6.495 5.795 6.728 7.652 8.566 9.471 10.368 6.230 7.020 7.786 4.111 4.564 4.968 8 2.723 3.546 4.329 5.076 5.786 6.463 7.108 7.722 8.306 8.863 9.394 9.899 3.696 4.231 4.712 5.146 5.537 9 3.240 3.890 4.486 5.033 5.535 5.995 6.418 6.805 7.161 7.487 7.786 6.733 7.435 8.111 8.760 9.385 9.986 10 8.983 9.787 5.889 6.207 5.328 5.650 5.938 11 12 6.814 6.194 13 6.424 11.255 12.134 13.004 13.865 14.718 14 1.783 2.577 3.312 3.993 4.623 5.206 5.747 6.247 6.710 7.139 7.536 7.904 8.244 8.559 8.851 9.122 9.372 9.604 9.818 10.675 11.258 11.925 12.233 8.530 9.253 9.954 10.635 11.296 11.938 12.561 13.166 13.754 6.492 6.750 6.982 7.191 6.628 15 10.380 8.061 6.811 16 10.838 7.379 ME 6.802 7.360 7.887 8.384 8.853 9.295 9.712 10.106 10.477 10.828 11.158 11.470 12.783 13.765 15.046 15.762 6.515 7.024 7.499 7.943 8.358 8.745 9. 108 9.447 9.763 10.059 10.336 10.594 11.654 12.409 13.332 13.801 8.313 8.544 17 10.575 11.348 12.106 12.849 13.578 14.292 14.992 15.678 16.351 19.523 22.396 27.355 31.424 15.562 10.563 11.118 11.652 12.166 12.659 13.134 13.590 15.622 11.274 7.103 7.367 7.606 7.824 8.022 8.201 8.365 8.514 9.077 18 6.974 7.120 7.250 7.366 11.690 8.756 19 14.324 12.085 16.398 17.226 18.046 22.023 8.950 7.549 7.702 7.839 7.963 8.422 20 7.469 9.129 9.823 25 7.843 30 25.808 14.877 17.413 19.600 23.115 25.730 12.462 14.094 15.372 17.159 18.256 8.694 17.292 19.793 21.482 40 32.835 39.196 10.274 10.757 10.962 8.055 8.244 9.427 9.779 9.915 8.951 9.042 50 8.304 Appendix D (concluded) Present value of an annuity of $1 Percent Period 13% 14% 15% 16% 17% 18% 19% 20% 25% 30% 35% 40% 50% 1 0.885 0.862 0.855 0.847 0.769 0.714 0.667 0.877 1.647 0.870 1.626 0.840 1.547 0.833 1.528 1.668 1.605 1.566 0.800 1.440 1.952 1.361 1.224 1.585 2.210 1.111 2.322 2.283 2.174 2.106 2.361 2.974 1.589 2.246 2.798 1.816 2.166 0.741 1.289 1.696 1.997 2.220 2.914 2.855 2.743 2.690 mm 00 2.589 2.991 1.407 1.605 1.737 3.517 3.352 3.127 2.436 2.643 3.498 2.140 2.639 3.058 3.410 3.706 3.954 3.433 3.889 4.288 4.639 4.946 5.216 3.998 4.423 4.799 1.824 3.274 3.685 4.039 4.344 3.784 4.160 4.487 3.199 3.589 3.922 4.207 4.451 1.849 2.035 2.168 2.263 2.331 3.812 4.078 2.362 2.689 2.951 3.161 3.329 3.463 3.571 2.385 2.508 2.598 2.802 2.925 1.883 1.922 9 5.132 4.607 4.163 3.326 3.605 3.837 4.031 4.192 4.327 4.439 2.665 4.772 5.019 2.379 10 5.426 4.659 4.303 4.494 4.656 4.793 3.019 3.092 3.147 3.190 2.414 2.438 11 4.833 5.029 5.197 5.342 5.453 1.948 1.965 1.977 1.985 5.687 5.918 5.234 5.421 4.339 4.486 4.611 4.715 4.836 4.988 2.715 2.752 2.779 3.656 3.725 12 5.660 2.456 13 6.122 5.842 5.583 5.118 4.910 4.533 3.780 3.223 2.799 2.469 1.990 14 6.002 5.724 5.468 5.229 5.008 3.824 2.814 1.993 6.302 6.462 4.611 4.675 3.249 3.268 15 6.142 5.847 5.575 5.324 5.092 3.859 2.825 2.478 2.484 2.489 1.995 16 6.265 5.954 5.668 5.405 4.802 4.876 4.938 4.988 5.033 4.730 3.283 6.604 6.729 6.840 5.162 5.222 2.834 2.840 17 6.373 6.047 5.749 4.775 3.295 2.492 1.997 1.998 1.999 1.999 18 6.128 5.818 3.304 2.844 2.494 6.467 6.550 5.273 5.316 4.812 4.843 19 6.938 6.198 5.877 5.070 3.887 3.910 3.928 3.942 3.954 3.985 3.995 3.311 5.475 5.534 5.584 5.628 5.766 5.829 2.848 20 6.623 5.101 25 7.025 7.330 7.496 6.873 7.003 6.259 6.464 6.566 5.929 6.097 6.177 5.353 5.467 5.517 5.548 5.554 5.195 5.235 4.870 4.948 4.979 3.316 3.329 3.332 2.850 2.856 2.857 2.496 2.497 2.499 2.500 2.500 2.500 1.999 2.000 2.000 30 7.634 7.105 6.642 6.233 5.871 5.258 4.997 3.999 2.857 40 50 3.333 3.333 2.000 2.000 7.675 7.133 6.661 6.246 5.880 5.262 4.999 4.000 2.857