Answered step by step

Verified Expert Solution

Question

1 Approved Answer

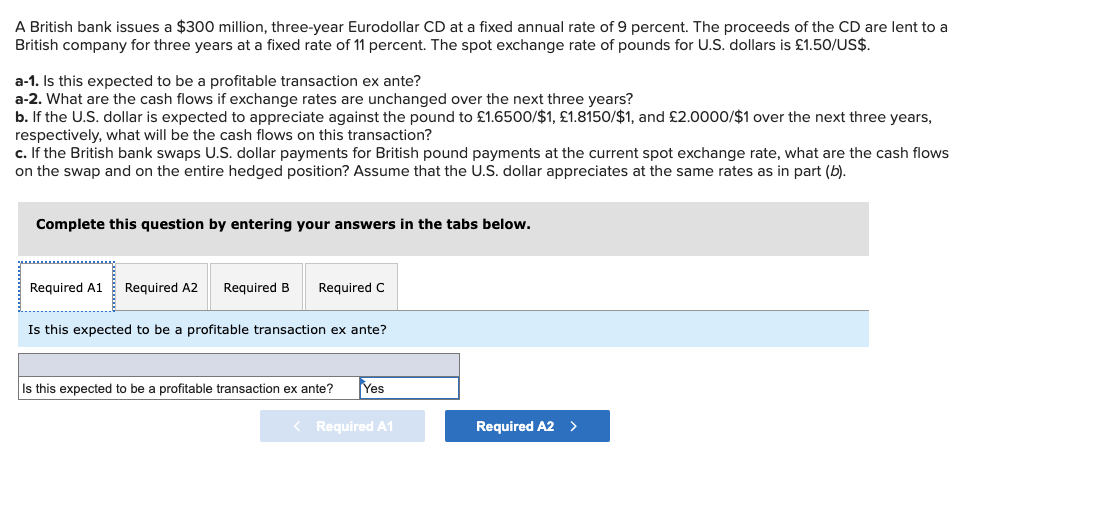

A British bank issues a $300 million, three-year Eurodollar CD at a fixed annual rate of 9 percent. The proceeds of the CD are lent

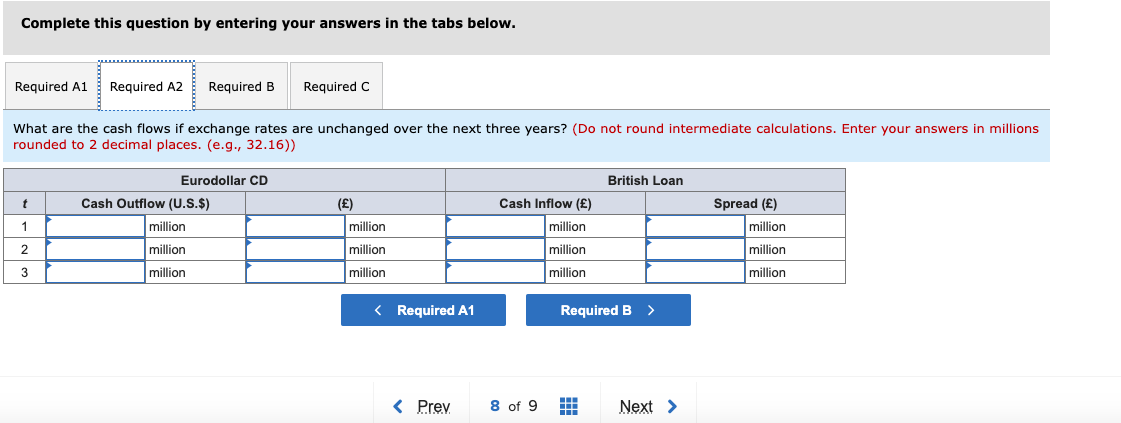

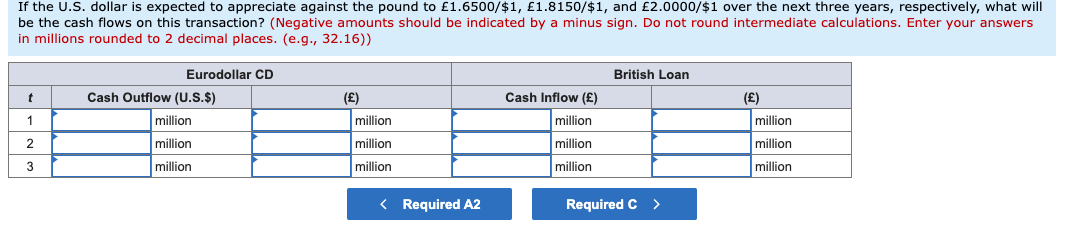

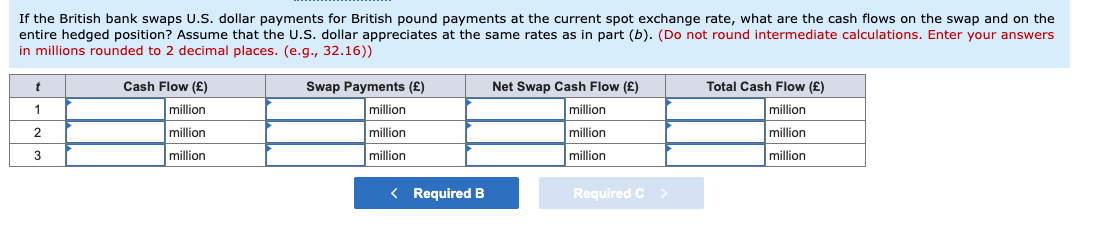

A British bank issues a $300 million, three-year Eurodollar CD at a fixed annual rate of 9 percent. The proceeds of the CD are lent to a British company for three years at a fixed rate of 11 percent. The spot exchange rate of pounds for U.S. dollars is 1.50/US$. a-1. Is this expected to be a profitable transaction ex ante? a-2. What are the cash flows if exchange rates are unchanged over the next three years? b. If the U.S. dollar is expected to appreciate against the pound to 1.6500/$1, 1.8150/$1, and 2.0000/$1 over the next three years, respectively, what will be the cash flows on this transaction? c. If the British bank swaps U.S. dollar payments for British pound payments at the current spot exchange rate, what are the cash flows on the swap and on the entire hedged position? Assume that the U.S. dollar appreciates at the same rates as in part (b). Complete this question by entering your answers in the tabs below. Required A1 Required A2 Required B Required C Is this expected to be a profitable transaction ex ante? Is this expected to be a profitable transaction ex ante? Yes Complete this question by entering your answers in the tabs below. Required A1 Required A2 Required B Required C What are the cash flows if exchange rates are unchanged over the next three years? (Do not round intermediate calculations. Enter your answers in millions rounded to 2 decimal places. (e.g., 32.16)) Eurodollar CD British Loan t Cash Outflow (U.S.$) () Cash Inflow () Spread () million 1 million million million million million million million million million million million If the U.S. dollar is expected to appreciate against the pound to 1.6500/$1, 1.8150/$1, and 2.0000/$1 over the next three years, respectively, what will be the cash flows on this transaction? (Negative amounts should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers in millions rounded to 2 decimal places. (e.g., 32.16)) Eurodollar CD British Loan t Cash Outflow (U.S.$) million 1 () million million Cash Inflow () million million () million million million 2 million 3 million million million Complete this question by entering your answers in the tabs below. Required A1 Required A2 Required B Required C What are the cash flows if exchange rates are unchanged over the next three years? (Do not round intermediate calculations. Enter your answers in millions rounded to 2 decimal places. (e.g., 32.16)) Eurodollar CD British Loan t Cash Outflow (U.S.$) () Cash Inflow () Spread () million 1 million million million million million million million million million million million If the U.S. dollar is expected to appreciate against the pound to 1.6500/$1, 1.8150/$1, and 2.0000/$1 over the next three years, respectively, what will be the cash flows on this transaction? (Negative amounts should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers in millions rounded to 2 decimal places. (e.g., 32.16)) Eurodollar CD British Loan t Cash Outflow (U.S.$) million 1 () million million Cash Inflow () million million () million million million 2 million 3 million million million

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multifractal Financial Markets An Alternative Approach To Asset And Risk Management

Authors: Yasmine Hayek Kobeissi

1st Edition

1461444896, 978-1461444893