Answered step by step

Verified Expert Solution

Question

1 Approved Answer

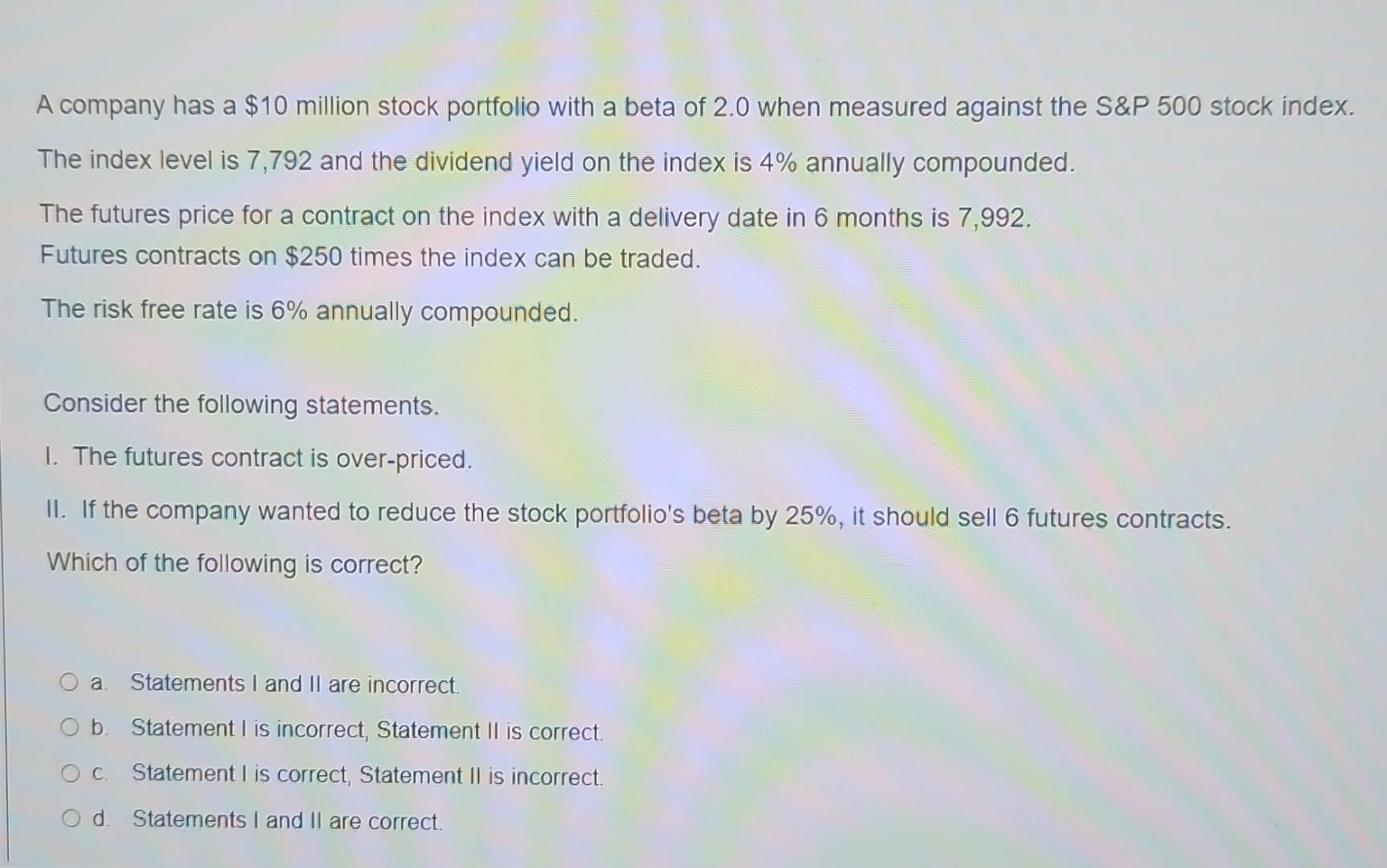

A company has a $10 million stock portfolio with a beta of 2.0 when measured against the S&P 500 stock inde The index level is

A company has a $10 million stock portfolio with a beta of 2.0 when measured against the S\&P 500 stock inde The index level is 7,792 and the dividend yield on the index is 4% annually compounded. The futures price for a contract on the index with a delivery date in 6 months is 7,992 . Futures contracts on $250 times the index can be traded. The risk free rate is 6% annually compounded. Consider the following statements. 1. The futures contract is over-priced. II. If the company wanted to reduce the stock portfolio's beta by 25%, it should sell 6 futures contracts. Which of the following is correct? a. Statements I and II are incorrect. b. Statement I is incorrect, Statement II is correct. c. Statement I is correct, Statement II is incorrect. d. Statements I and II are correct

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing The Audit Function A Corporate Audit Department Procedures Guide

Authors: Michael P. Cangemi

2nd Edition

0471012556, 978-0471012559