Answered step by step

Verified Expert Solution

Question

1 Approved Answer

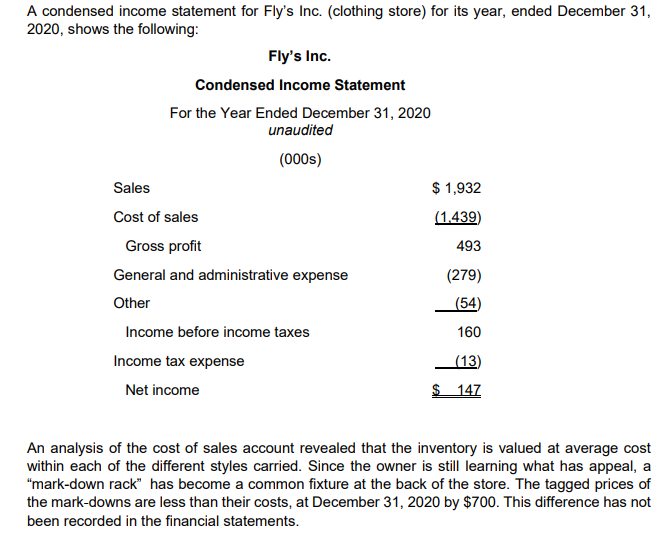

A condensed income statement for Fly's Inc. (clothing store) for its year, ended December 31, 2020, shows the following: Fly's Inc. Condensed Income Statement

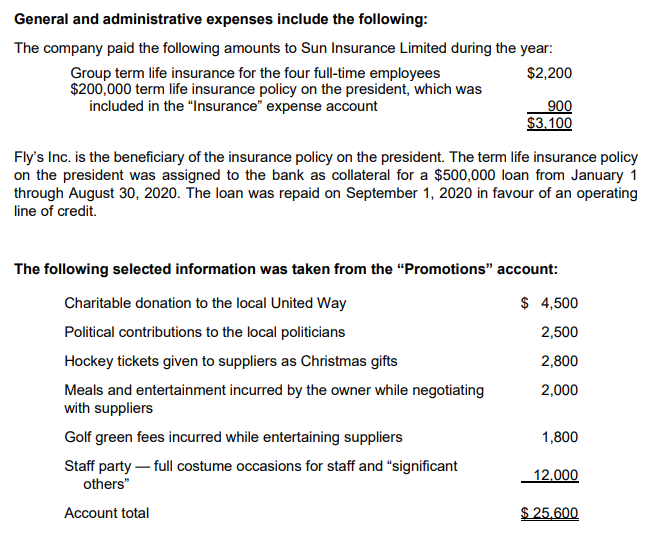

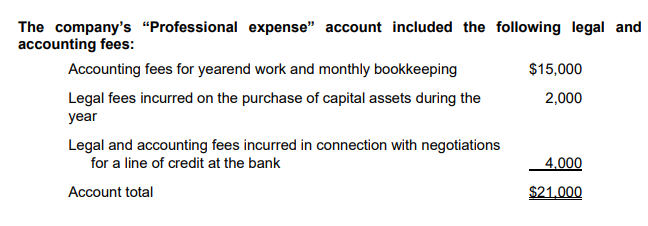

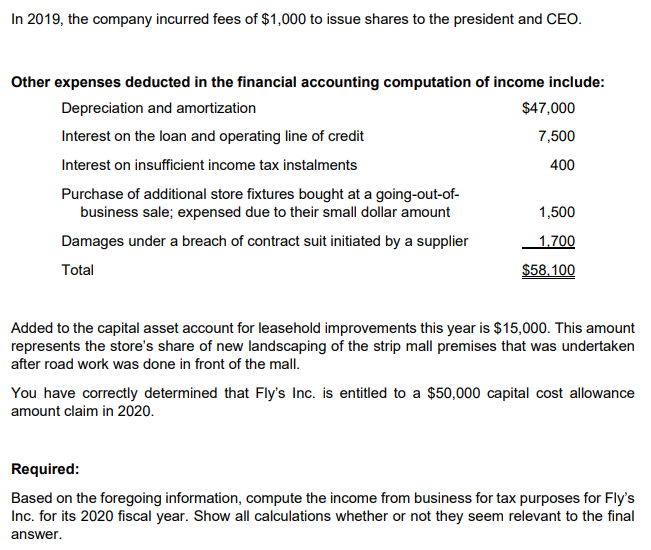

A condensed income statement for Fly's Inc. (clothing store) for its year, ended December 31, 2020, shows the following: Fly's Inc. Condensed Income Statement For the Year Ended December 31, 2020 unaudited (000s) Sales Cost of sales $ 1,932 (1.439) Gross profit 493 General and administrative expense (279) Other Income before income taxes Income tax expense (54) 160 (13) Net income $ 147 An analysis of the cost of sales account revealed that the inventory is valued at average cost within each of the different styles carried. Since the owner is still learning what has appeal, a "mark-down rack" has become a common fixture at the back of the store. The tagged prices of the mark-downs are less than their costs, at December 31, 2020 by $700. This difference has not been recorded in the financial statements. Cost of goods sold includes a charge of $1,800 to set up an allowance for returns (at 0.1% of sales) that are not subsequently saleable at full retail price. No such allowance was recorded last year-end because the company only discovered that the allowance was necessary this year. General and administrative expenses include the following: The company paid the following amounts to Sun Insurance Limited during the year: Group term life insurance for the four full-time employees $200,000 term life insurance policy on the president, which was included in the "Insurance" expense account $2,200 900 $3,100 Fly's Inc. is the beneficiary of the insurance policy on the president. The term life insurance policy on the president was assigned to the bank as collateral for a $500,000 loan from January 1 through August 30, 2020. The loan was repaid on September 1, 2020 in favour of an operating line of credit. The following selected information was taken from the "Promotions" account: Charitable donation to the local United Way Political contributions to the local politicians $ 4,500 2,500 Hockey tickets given to suppliers as Christmas gifts 2,800 Meals and entertainment incurred by the owner while negotiating with suppliers 2,000 Golf green fees incurred while entertaining suppliers 1,800 Staff party-full costume occasions for staff and "significant 12,000 others" Account total $25,600 The company's "Professional expense" account included the following legal and accounting fees: Accounting fees for yearend work and monthly bookkeeping Legal fees incurred on the purchase of capital assets during the year Legal and accounting fees incurred in connection with negotiations for a line of credit at the bank Account total $15,000 2,000 4,000 $21,000 In 2019, the company incurred fees of $1,000 to issue shares to the president and CEO. Other expenses deducted in the financial accounting computation of income include: Depreciation and amortization Interest on the loan and operating line of credit Interest on insufficient income tax instalments Purchase of additional store fixtures bought at a going-out-of- business sale; expensed due to their small dollar amount Damages under a breach of contract suit initiated by a supplier Total $47,000 7,500 400 1,500 1,700 $58,100 Added to the capital asset account for leasehold improvements this year is $15,000. This amount represents the store's share of new landscaping of the strip mall premises that was undertaken after road work was done in front of the mall. You have correctly determined that Fly's Inc. is entitled to a $50,000 capital cost allowance amount claim in 2020. Required: Based on the foregoing information, compute the income from business for tax purposes for Fly's Inc. for its 2020 fiscal year. Show all calculations whether or not they seem relevant to the final answer.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting Volume 2

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield, Irene M. Wiecek, Bruce J. McConomy

12th Canadian Edition

1119497043, 978-1119497042