Answered step by step

Verified Expert Solution

Question

1 Approved Answer

a detailed answer and step by step process with general equations will be greatly appreciated! Q14. You are to price a butterfly spread on a

a detailed answer and step by step process with general equations will be greatly appreciated!

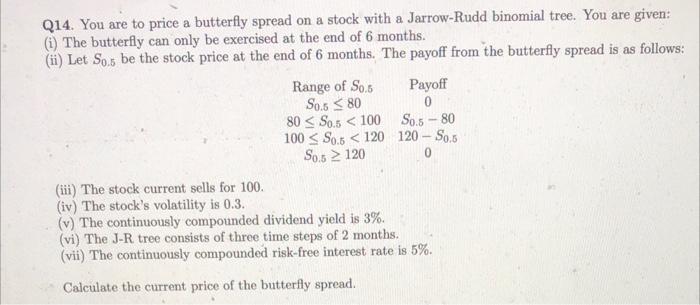

Q14. You are to price a butterfly spread on a stock with a Jarrow-Rudd binomial tree. You are given: (i) The butterfly can only be exercised at the end of 6 months. (ii) Let So be the stock price at the end of 6 months. The payoff from the butterfly spread is as follows: Range of So, Payoff S0.5 120 0 (iii) The stock current sells for 100. (iv) The stock's volatility is 0.3. (v) The continuously compounded dividend yield is 3%. (vi) The J-R tree consists of three time steps of 2 months. (vii) The continuously compounded risk-free interest rate is 5%. Calculate the current price of the butterfly spread. Q14. You are to price a butterfly spread on a stock with a Jarrow-Rudd binomial tree. You are given: (i) The butterfly can only be exercised at the end of 6 months. (ii) Let So be the stock price at the end of 6 months. The payoff from the butterfly spread is as follows: Range of So, Payoff S0.5 120 0 (iii) The stock current sells for 100. (iv) The stock's volatility is 0.3. (v) The continuously compounded dividend yield is 3%. (vi) The J-R tree consists of three time steps of 2 months. (vii) The continuously compounded risk-free interest rate is 5%. Calculate the current price of the butterfly spread Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance Building Your Future

Authors: Robert B. Walker, Kristy P. Walker

1st edition

9780077861728, 978-0073530659