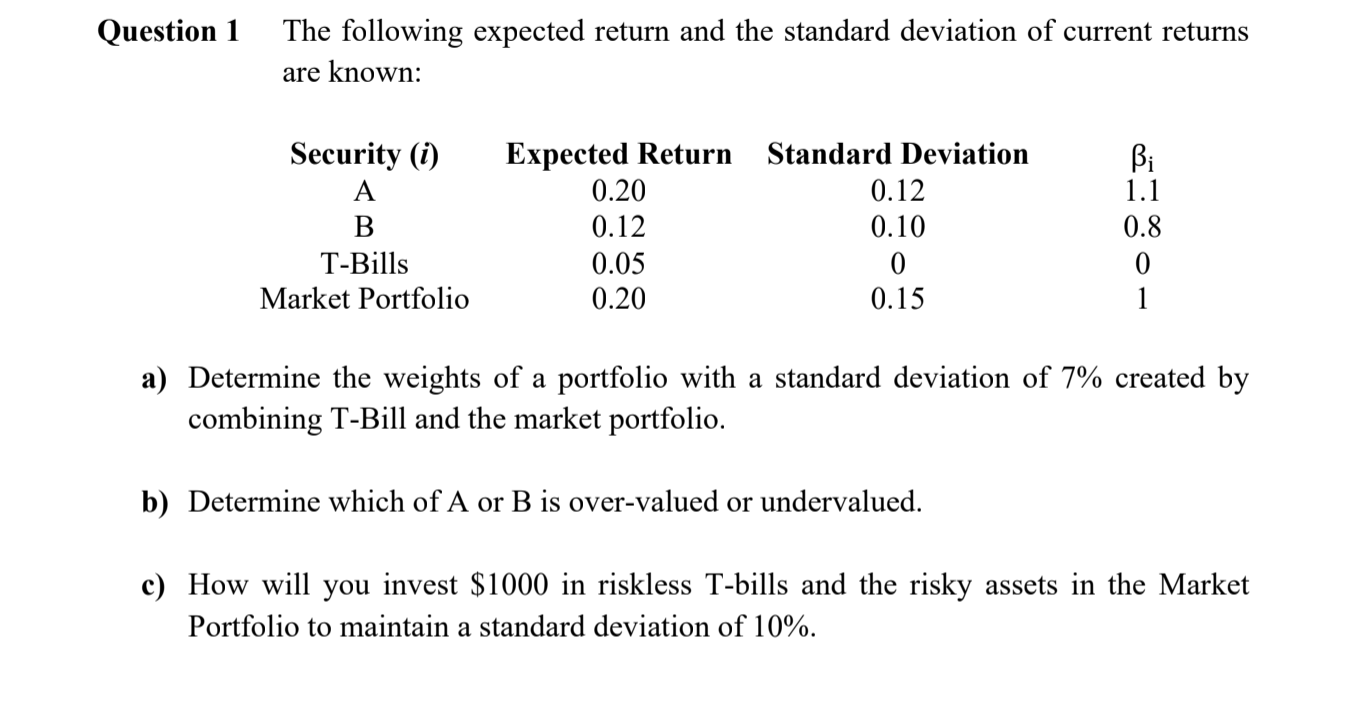

Question

a) Determine the weights of a portfolio with a standard deviation of 7% created by combining T-Bill and the market portfolio. b) Determine which of

a) Determine the weights of a portfolio with a standard deviation of 7% created by combining T-Bill and the market portfolio. b) Determine which of A or B is over-valued or undervalued. c) How will you invest $1000 in riskless T-bills and the risky assets in the Market Portfolio to maintain a standard deviation of 10%.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurship In Finance Successfully Launching And Managing A Hedge Fund In Asia

Authors: Henri Arslanian

1st Edition

331943912X,3319439138