Question

A European binary ( or Digital) option pays $5 if stock ends above $56 after 3 months and nothing otherwise. The following 3-period binomial tree

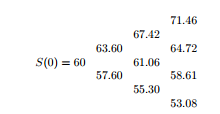

A European binary ( or Digital) option pays $5 if stock ends above $56 after 3 months and nothing otherwise. The following 3-period binomial tree represents the MONTHLY stock price movements:

Assuming continuously compounded interest rate of r=3% and no dividends, find the REPLICATING PORTFOLIOS for each date if the stock prices moves according to

S(0) = 60 --> S(1) = 63.60 ---> S(2) = 61.06 ---> S(3) = 58.61

Verify that your replicating strategy is self-financing at each step.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

DeFi And The Future Of Finance

Authors: Campbell R. Harvey, Ashwin Ramachandran, Joey Santoro, Vitalik Buterin, Fred Ehrsam

1st Edition

1119836018, 978-1119836018