Answered step by step

Verified Expert Solution

Question

1 Approved Answer

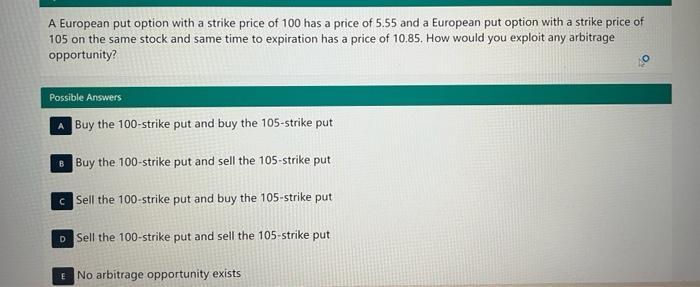

A European put option with a strike price of 100 has a price of 5.55 and a European put option with a strike price

A European put option with a strike price of 100 has a price of 5.55 and a European put option with a strike price of 105 on the same stock and same time to expiration has a price of 10.85. How would you exploit any arbitrage opportunity? Possible Answers A Buy the 100-strike put and buy the 105-strike put 8 Buy the 100-strike put and sell the 105-strike put c Sell the 100-strike put and buy the 105-strike put D Sell the 100-strike put and sell the 105-strike put E No arbitrage opportunity exists

Step by Step Solution

★★★★★

3.42 Rating (158 Votes )

There are 3 Steps involved in it

Step: 1

The detailed answer for the above question is provided below One way to check whether arbit...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Business Analytics

Authors: Jeffrey Camm, James Cochran, Michael Fry, Jeffrey Ohlmann, David Anderson, Dennis Sweeney, Thomas Williams

1st Edition

128518727X, 978-1337360135, 978-1285187273