Question

a) Explain the answer? b) An option's delta changes over the option's life. 1q))The current price of a non-dividend paying stock is $50. Use a

a) Explain the answer? b) An option's delta changes over the option's life.

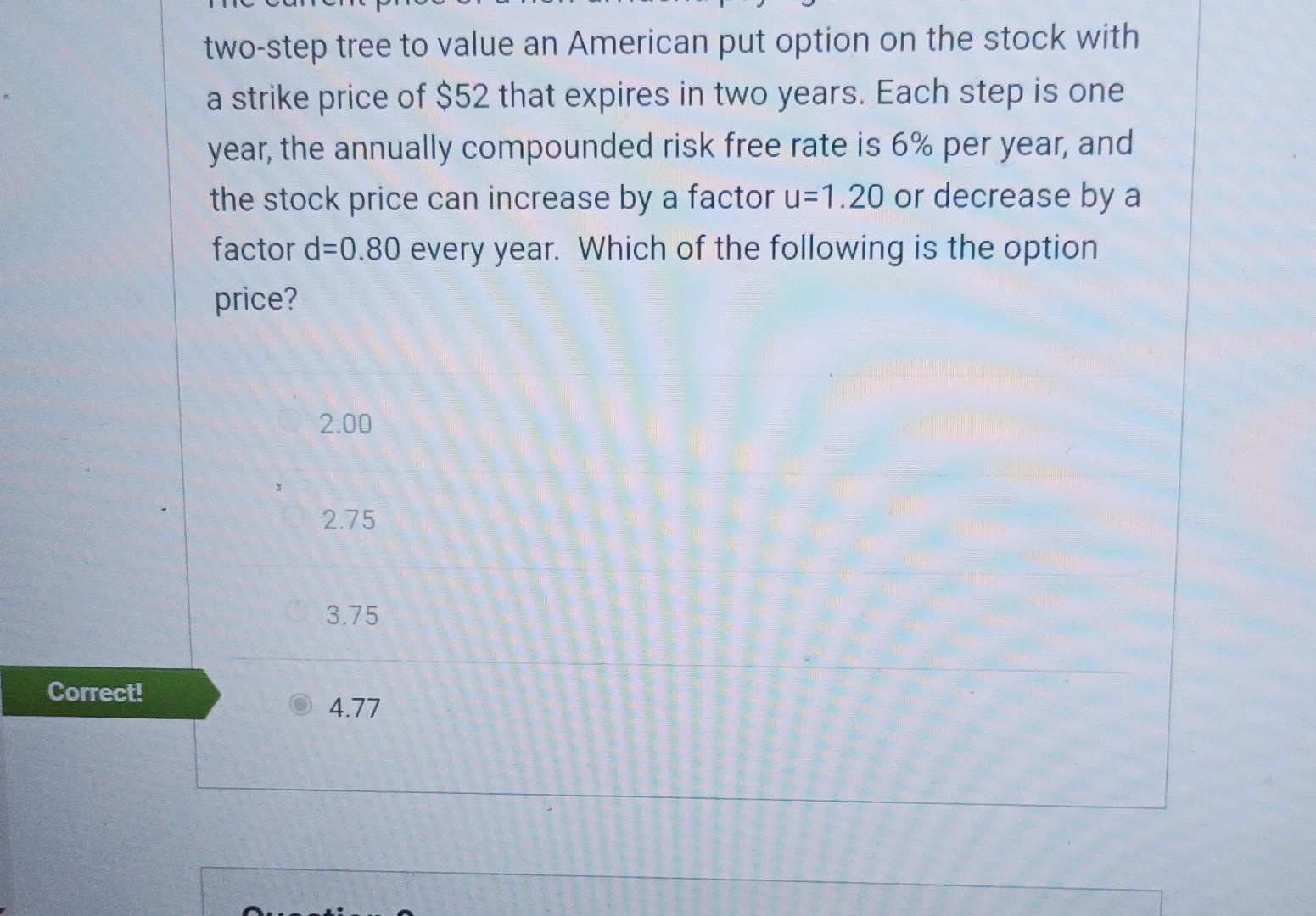

1q))The current price of a non-dividend paying stock is $50. Use a two-step tree to value an American put option on the stock with a strike price of $52 that expires in two years. Each step is one year, the annually compounded risk free rate is 6% per year, and the stock price can increase by a factor u=1.20 or decrease by a factor d=0.80 every year. Which of the following is the option price?

a)2.00

b)2.75

C)3.75

d)4.77

2q)) An option's delta changes over the option's life. a) True b) False

3q)) The current price of a non-dividend-paying stock is $40. Over the next six months it is expected to rise to $44 or fall to $36. Assume the risk-free rate is zero. An investor buys a protective put on the stock (i.e., buy 1 share of the stock and buy 1 European put option on the stock). The put option has a strike price of $42. Which of the following is the hedge ratio of the position?

a)0.25

b) -0.50

c) -0.75

d) 0.0 The position is without any risk.

please answer the 3 questions with explanation and correct answers for 1q is 4.77, 2q is True, 3q is 0.25. Give me ur contact address for further questions please .

two-step tree to value an American put option on the stock with a strike price of $52 that expires in two years. Each step is one year, the annually compounded risk free rate is 6% per year, and the stock price can increase by a factor u=1.20 or decrease by a factor d=0.80 every year. Which of the following is the option price? 2.00 2.75 3.75 4.77Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Ultimate Beginners Guide To Understanding NFTs

Authors: LM Anderson

1st Edition

1739781732, 978-1739781736