Answered step by step

Verified Expert Solution

Question

1 Approved Answer

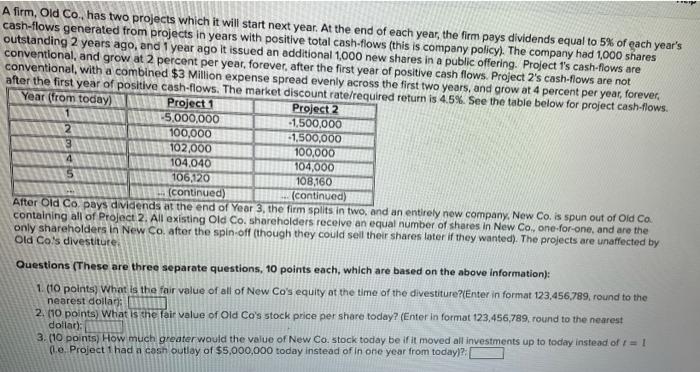

A firm, Old Co., has two projects which it will start next year. At the end of each year, the firm pays dividends equal to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Rise Of The AiCCOUNTANTS The What Why And How Of Artificial Intelligence For Accountants

Authors: Hitendra R. Patil

1st Edition

B0BTKSP6M8, 979-8374511352