a) Fixed costs; Variable costs and Mixed costs (semi-variable).

b) Separate from mixed costs variable cost (per unit) and fixed costs per week. Please show calculations.

c) calculate total production fixed costs per week.

d) total production variable cost per unit.

e) total non-production variable cost per unit?

f) total non-production fixed costs per week.

g) total fixed costs per week

h) total variable cost per unit?

i) If the selling price of the product is $ 7.00, how much is the contribution margin per unit?

j) If the selling price of the product is 7.00, What is the break-even point in units?

k) If (Table 5) selling price is $8.00 , commission increases to $ 1.20 per unit . How much is the contribution margin per unit? What is the break-even point in units?

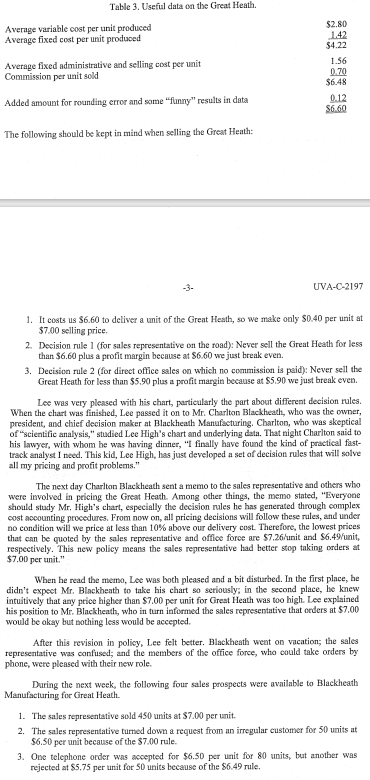

1. It costs us $6.60 to deliver a unit of the Great Heath, 50 we make only $0.40 per unit at $7.00 selling price. 2. Decision rule 1 (for sales representative on the road): Never sell the Great Heath for less than $6.60 plus a profit margin because at $6.60 we just break even. 3. Decision rule 2 (for direct office sales on which no commission is peid): Never sell the Great Heath for less than $5.50 plus a profit margin because at $5.90 we just break even. Lee was very plensed with his chart, particularly the part about different decision rules. When the chart was finished, Lee passed it on to Mr. Charlton Blackheath, who was the owner, president, and chief decision maker at Blackheath Manufacturing. Charlton, who was skeptical of "scientific analysis," studied Lee High's chart and underlying data. That night Charlton said to his lawyer, with whom be was having dinner, "I finally have found the kind of practical fasttrack analyst I need. This kid, Lee High, has just developed a set of decision rules that will solve all my pricing and profit problems." The next day Charlton Blackheath sent a memo to the sales representative and others who were involved in pricing the Great Heath. Among ofher things, the memo stated, "Everyone should study Mr. High's chart, especially the decision rules he has generated through complex cost acoounting procedures. From now on, all pricing decisions will follow these rules, and under no condition will we price at less than 10% above our delivery cost. Therefore, the lowest prices that can be quoted by the sales representative and office force are $7.26 iunit and $6.49 /unit, respectively. This new policy means the sales representative had better stop taking orders at $7.00 per unit." When he read the memo, Lee was both pleased and a bit tisturbed. In the first place, be didn't expect Mr. Blackhenth to take his chart so seriously; in the second place, be knew intultively that any price higher than $7.00 per unit for Great Heath was too high. Lee explained his position to Mr. Blackheath, who in turn informed the sales representative that erders at $7.00 would be oksy but nothing less would be accepted. After this revision in policy, Lee felt better. Blackheath weat on vacation; the sales representative was confused; and the members of the office force, who could take orders by phone, were pleased with their new role. During the next week, the following four sales prospects were available to Blackheath Manufacturing for Great Heath. 1. The sales representative sold 450 units at $7.00 per unit. 2. The sales representative turned down a request from an irregular customer for 50 units at $6.50per unit because of the $7.00 rule. 3. One telephone order was aceepted for $6.50 per unit for 80 units, but another was 1. It costs us $6.60 to deliver a unit of the Great Heath, 50 we make only $0.40 per unit at $7.00 selling price. 2. Decision rule 1 (for sales representative on the road): Never sell the Great Heath for less than $6.60 plus a profit margin because at $6.60 we just break even. 3. Decision rule 2 (for direct office sales on which no commission is peid): Never sell the Great Heath for less than $5.50 plus a profit margin because at $5.90 we just break even. Lee was very plensed with his chart, particularly the part about different decision rules. When the chart was finished, Lee passed it on to Mr. Charlton Blackheath, who was the owner, president, and chief decision maker at Blackheath Manufacturing. Charlton, who was skeptical of "scientific analysis," studied Lee High's chart and underlying data. That night Charlton said to his lawyer, with whom be was having dinner, "I finally have found the kind of practical fasttrack analyst I need. This kid, Lee High, has just developed a set of decision rules that will solve all my pricing and profit problems." The next day Charlton Blackheath sent a memo to the sales representative and others who were involved in pricing the Great Heath. Among ofher things, the memo stated, "Everyone should study Mr. High's chart, especially the decision rules he has generated through complex cost acoounting procedures. From now on, all pricing decisions will follow these rules, and under no condition will we price at less than 10% above our delivery cost. Therefore, the lowest prices that can be quoted by the sales representative and office force are $7.26 iunit and $6.49 /unit, respectively. This new policy means the sales representative had better stop taking orders at $7.00 per unit." When he read the memo, Lee was both pleased and a bit tisturbed. In the first place, be didn't expect Mr. Blackhenth to take his chart so seriously; in the second place, be knew intultively that any price higher than $7.00 per unit for Great Heath was too high. Lee explained his position to Mr. Blackheath, who in turn informed the sales representative that erders at $7.00 would be oksy but nothing less would be accepted. After this revision in policy, Lee felt better. Blackheath weat on vacation; the sales representative was confused; and the members of the office force, who could take orders by phone, were pleased with their new role. During the next week, the following four sales prospects were available to Blackheath Manufacturing for Great Heath. 1. The sales representative sold 450 units at $7.00 per unit. 2. The sales representative turned down a request from an irregular customer for 50 units at $6.50per unit because of the $7.00 rule. 3. One telephone order was aceepted for $6.50 per unit for 80 units, but another was