Answered step by step

Verified Expert Solution

Question

1 Approved Answer

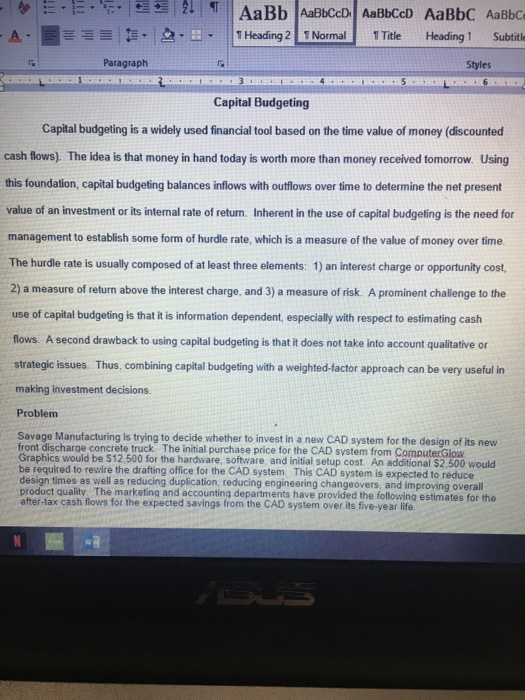

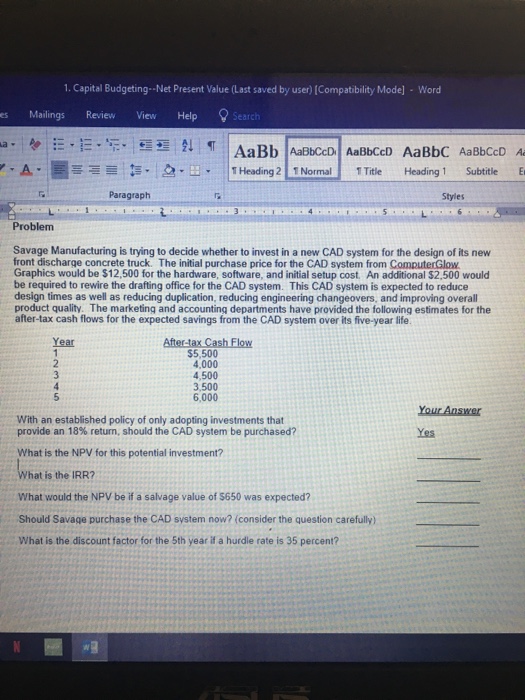

A. ?F.la-B: ||THeading 2LNormal! 1Title Heading 1 Subtitle Paragraph Styles Capital Budgeting Capital budgeting is a widely used financial tool based on the time value

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Future Of Real Estate Early Warning Realtors

Authors: Anya Bartholomew

1st Edition

1975711149, 978-1975711146