Answered step by step

Verified Expert Solution

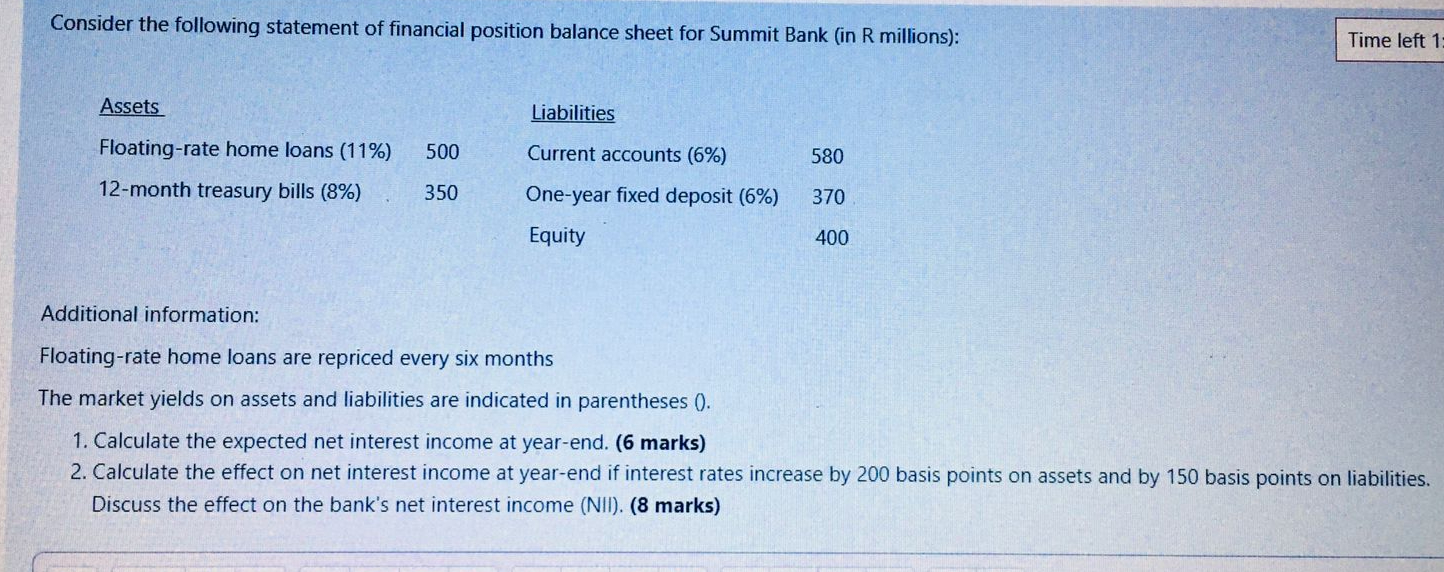

Question

1 Approved Answer

A four - year option - free bond has a par value of R 1 0 0 0 , has an annual coupon rate of

A fouryear optionfree bond has a par value of R has an annual coupon rate of percent and trades at a yield to maturity of percent. The current bond price is R The yield to maturity is expected to increase by bp

Calculate the duration of the bond. marks

Assuming that the bonds convexity is use durationwithconvexity to calculate the price of the bond at the new yield. marks

Show all workings.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Venture Capital Investment Process

Authors: Darek Klonowski

1st Edition

0230612881, 023011007X, 9780230612884, 9780230110076