Answered step by step

Verified Expert Solution

Question

1 Approved Answer

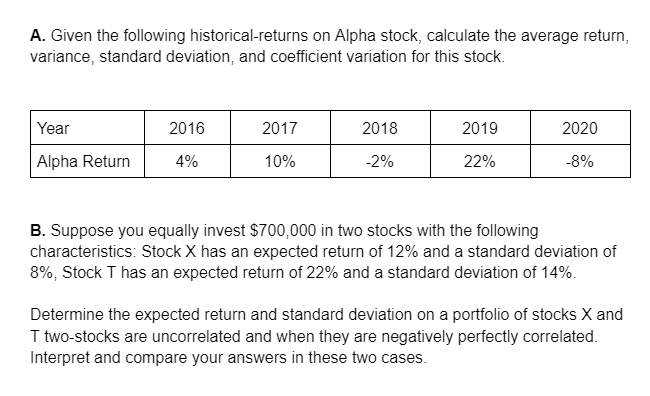

A. Given the following historical-returns on Alpha stock, calculate the average return, variance, standard deviation, and coefficient variation for this stock. Year 2016 2017

A. Given the following historical-returns on Alpha stock, calculate the average return, variance, standard deviation, and coefficient variation for this stock. Year 2016 2017 2018 2019 2020 Alpha Return 4% 10% -2% 22% -8% B. Suppose you equally invest $700,000 in two stocks with the following characteristics: Stock X has an expected return of 12% and a standard deviation of 8%, Stock T has an expected return of 22% and a standard deviation of 14%. Determine the expected return and standard deviation on a portfolio of stocks X and T two-stocks are uncorrelated and when they are negatively perfectly correlated. Interpret and compare your answers in these two cases.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Average return for Alpha stock 52 Variance 9314 Standard Deviation 965 Coefficient of Variation 18558 Expected return on the portfolio of stocks X and ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Managerial Finance

Authors: Chad Zutter, Scott Smart

16th Global Edition

1292400641, 978-1292400648