Answered step by step

Verified Expert Solution

Question

1 Approved Answer

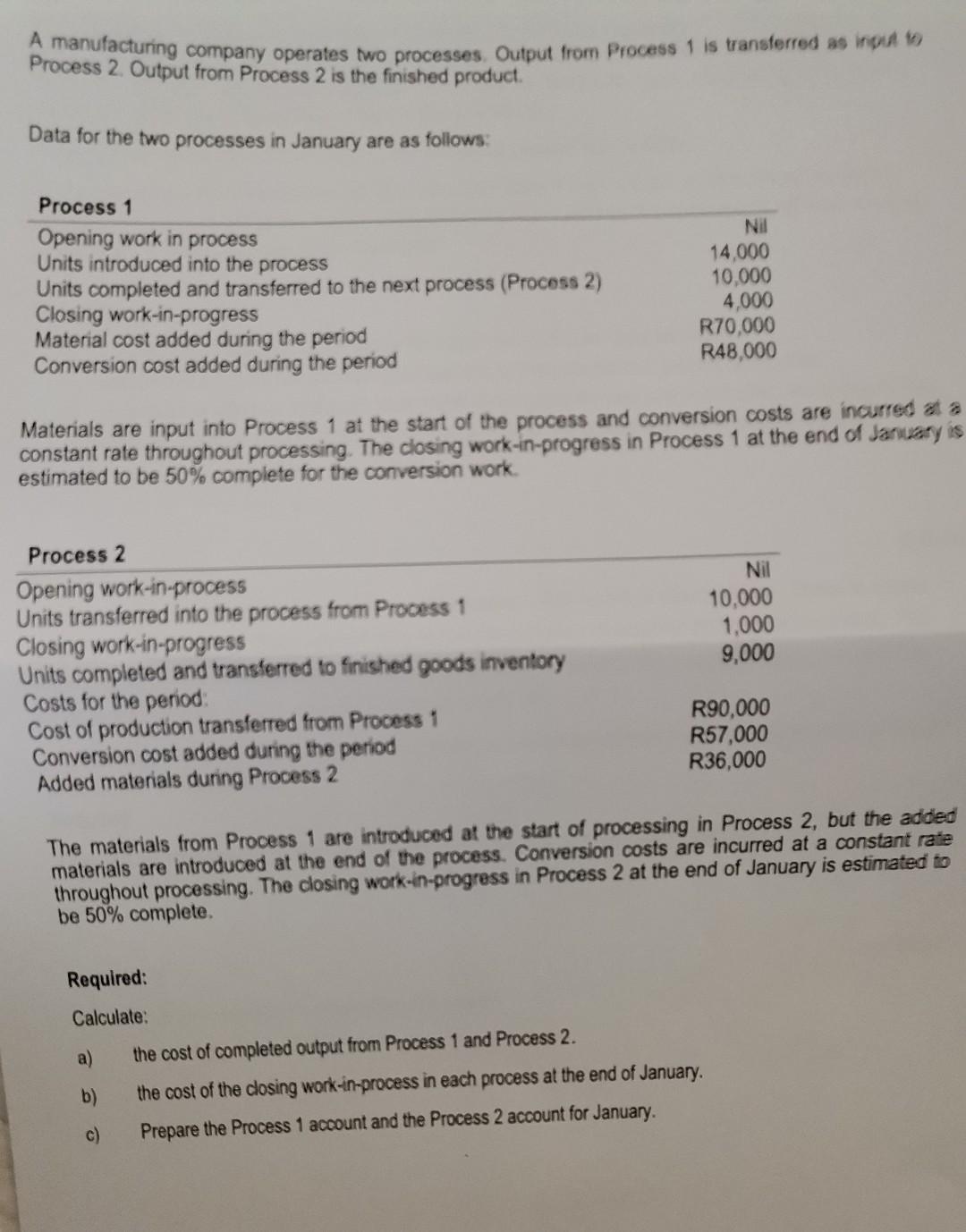

A manufacturing company operates two processes. Output from Process 1 is transferred as input to Process 2. Output from Process 2 is the finished product.

A manufacturing company operates two processes. Output from Process 1 is transferred as input to Process 2. Output from Process 2 is the finished product. Data for the two processes in January are as follows: Process 1 Opening work in process Units introduced into the process Units completed and transferred to the next process (Process 2) Closing work-in-progress Material cost added during the period Conversion cost added during the period Process 2 Opening work-in-process Units transferred into the process from Process 1 Closing work-in-progress Units completed and transferred to finished goods inventory Costs for the period: Cost of production transferred from Process 1 Conversion cost added during the period Added materials during Process 2 Materials are input into Process 1 at the start of the process and conversion costs are incurred at a constant rate throughout processing. The closing work-in-progress in Process 1 at the end of January is estimated to be 50% complete for the conversion work. Required: Calculate: a) b) Nil 14,000 10,000 4,000 R70,000 R48,000 The materials from Process 1 are introduced at the start of processing in Process 2, but the added materials are introduced at the end of the process. Conversion costs are incurred at a constant rate throughout processing. The closing work-in-progress in Process 2 at the end of January is estimated to be 50% complete. c) Nil 10,000 1,000 9,000 R90,000 R57,000 R36,000 the cost of completed output from Process 1 and Process 2. the cost of the closing work-in-process in each process at the end of January. Prepare the Process 1 account and the Process 2 account for January

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting A Smart Approach

Authors: Mary Carey, Cathy Knowles, Jane Towers-Clark

3rd Edition

0198745133, 978-0198745136