Question

Given the results from the tests above about serial correlation, multicollinearity, and heteroskedasticity, is it appropriate to use the estimated coefficients for statistical inference without

Given the results from the tests above about serial correlation, multicollinearity, and heteroskedasticity, is it appropriate to use the estimated coefficients for statistical inference without trying any fixes? Explain why or why not.

What suggestions would you have for another estimation of this regression? (For example, dropping some variable, changing the functional form, re-estimating using the Prais-Winsten GLS method, compute Newey-West standard errors, or compute White heteroskedasticity corrected standard errors.)

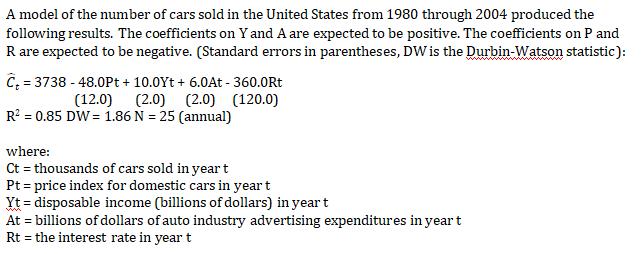

A model of the number of cars sold in the United States from 1980 through 2004 produced the following results. The coefficients on Y and A are expected to be positive. The coefficients on P and R are expected to be negative. (Standard errors in parentheses, DW is the Durbin-Watson statistic): C = 3738 - 48.0Pt + 10.0Yt + 6.0At - 360.0Rt (2.0) (120.0) (12.0) (2.0) R = 0.85 DW = 1.86 N = 25 (annual) where: Ct = thousands of cars sold in year t Pt = price index for domestic cars in year t Yt = disposable income (billions of dollars) in year t At = billions of dollars of auto industry advertising expenditures in year t Rt the interest rate in year t

Step by Step Solution

3.47 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

a Given the results from the tests above about serial correlation multicollinearity and heteroskedas...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Statistics Communicating With Numbers

Authors: Sanjiv Jaggia

3rd Edition

1259957616, 978-1259957611