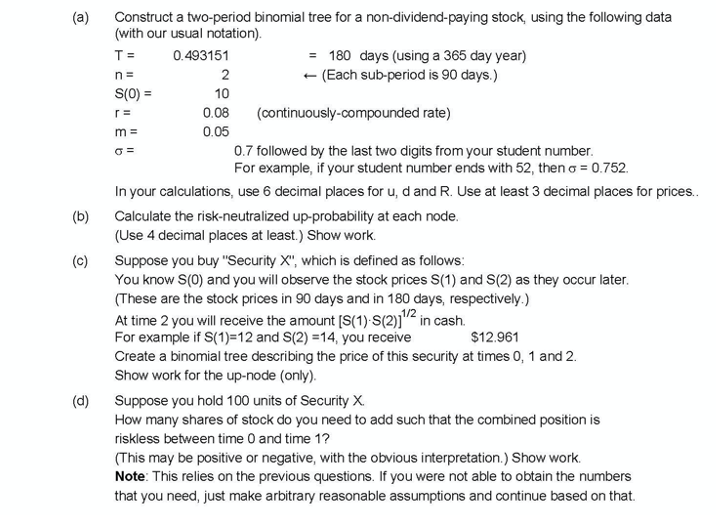

(a) n = m = (b) c) Construct a two-period binomial tree for a non-dividend-paying stock, using the following data (with our usual notation) T= 0.493151 = 180 days (using a 365 day year) 2 (Each sub-period is 90 days.) S(O) = 10 0.08 (continuously-compounded rate) 0.05 0.7 followed by the last two digits from your student number. For example, if your student number ends with 52, then o = 0.752. In your calculations, use 6 decimal places for u, d and R. Use at least 3 decimal places for prices.. Calculate the risk-neutralized up-probability at each node. (Use 4 decimal places at least.) Show work. Suppose you buy "Security X", which is defined as follows: You know S(O) and you will observe the stock prices S(1) and S(2) as they occur later. (These are the stock prices in 90 days and in 180 days, respectively.) At time 2 you will receive the amount [S(1) S(2)1'2 in cash. For example if S(1)=12 and S(2) =14, you receive $12.961 Create a binomial tree describing the price of this security at times 0, 1 and 2. Show work for the up-node (only) Suppose you hold 100 units of Security X How many shares of stock do you need to add such that the combined position is riskless between time and time 1? (This may be positive or negative, with the obvious interpretation.) Show work. Note: This relies on the previous questions. If you were not able to obtain the numbers that you need, just make arbitrary reasonable assumptions and continue based on that. (a) n = m = (b) c) Construct a two-period binomial tree for a non-dividend-paying stock, using the following data (with our usual notation) T= 0.493151 = 180 days (using a 365 day year) 2 (Each sub-period is 90 days.) S(O) = 10 0.08 (continuously-compounded rate) 0.05 0.7 followed by the last two digits from your student number. For example, if your student number ends with 52, then o = 0.752. In your calculations, use 6 decimal places for u, d and R. Use at least 3 decimal places for prices.. Calculate the risk-neutralized up-probability at each node. (Use 4 decimal places at least.) Show work. Suppose you buy "Security X", which is defined as follows: You know S(O) and you will observe the stock prices S(1) and S(2) as they occur later. (These are the stock prices in 90 days and in 180 days, respectively.) At time 2 you will receive the amount [S(1) S(2)1'2 in cash. For example if S(1)=12 and S(2) =14, you receive $12.961 Create a binomial tree describing the price of this security at times 0, 1 and 2. Show work for the up-node (only) Suppose you hold 100 units of Security X How many shares of stock do you need to add such that the combined position is riskless between time and time 1? (This may be positive or negative, with the obvious interpretation.) Show work. Note: This relies on the previous questions. If you were not able to obtain the numbers that you need, just make arbitrary reasonable assumptions and continue based on that