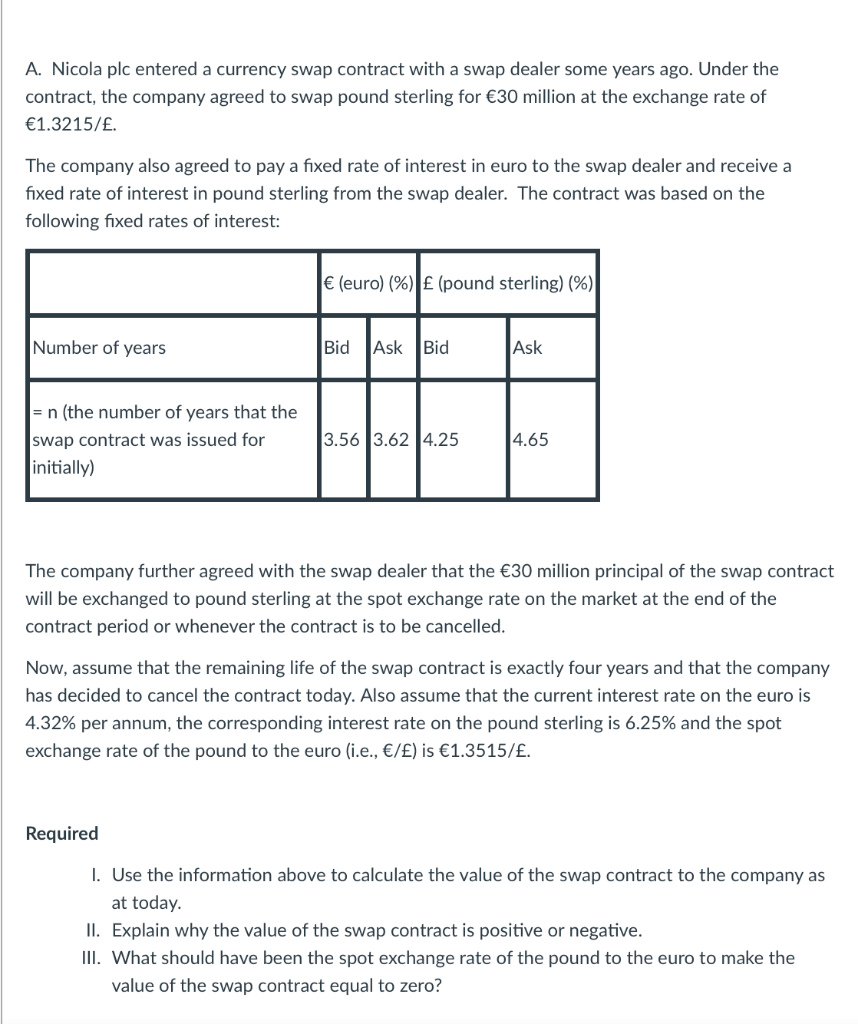

A. Nicola plc entered a currency swap contract with a swap dealer some years ago. Under the contract, the company agreed to swap pound sterling for 30 million at the exchange rate of 1.3215/. The company also agreed to pay a fixed rate of interest in euro to the swap dealer and receive a fixed rate of interest in pound sterling from the swap dealer. The contract was based on the following fixed rates of interest: (euro) (%) (pound sterling) (%) Number of years Bid Ask Bid Ask = n (the number of years that the swap contract was issued for initially) 3.56 3.62 4.25 4.65 The company further agreed with the swap dealer that the 30 million principal of the swap contract will be exchanged to pound sterling at the spot exchange rate on the market at the end of the contract period or whenever the contract is to be cancelled. Now, assume that the remaining life of the swap contract is exactly four years and that the company has decided to cancel the contract today. Also assume that the current interest rate on the euro is 4.32% per annum, the corresponding interest rate on the pound sterling is 6.25% and the spot exchange rate of the pound to the euro (i.e., /) is 1.3515/. Required 1. Use the information above to calculate the value of the swap contract to the company as at today. II. Explain why the value of the swap contract is positive or negative. III. What should have been the spot exchange rate of the pound to the euro to make the value of the swap contract equal to zero? A. Nicola plc entered a currency swap contract with a swap dealer some years ago. Under the contract, the company agreed to swap pound sterling for 30 million at the exchange rate of 1.3215/. The company also agreed to pay a fixed rate of interest in euro to the swap dealer and receive a fixed rate of interest in pound sterling from the swap dealer. The contract was based on the following fixed rates of interest: (euro) (%) (pound sterling) (%) Number of years Bid Ask Bid Ask = n (the number of years that the swap contract was issued for initially) 3.56 3.62 4.25 4.65 The company further agreed with the swap dealer that the 30 million principal of the swap contract will be exchanged to pound sterling at the spot exchange rate on the market at the end of the contract period or whenever the contract is to be cancelled. Now, assume that the remaining life of the swap contract is exactly four years and that the company has decided to cancel the contract today. Also assume that the current interest rate on the euro is 4.32% per annum, the corresponding interest rate on the pound sterling is 6.25% and the spot exchange rate of the pound to the euro (i.e., /) is 1.3515/. Required 1. Use the information above to calculate the value of the swap contract to the company as at today. II. Explain why the value of the swap contract is positive or negative. III. What should have been the spot exchange rate of the pound to the euro to make the value of the swap contract equal to zero