Answered step by step

Verified Expert Solution

Question

1 Approved Answer

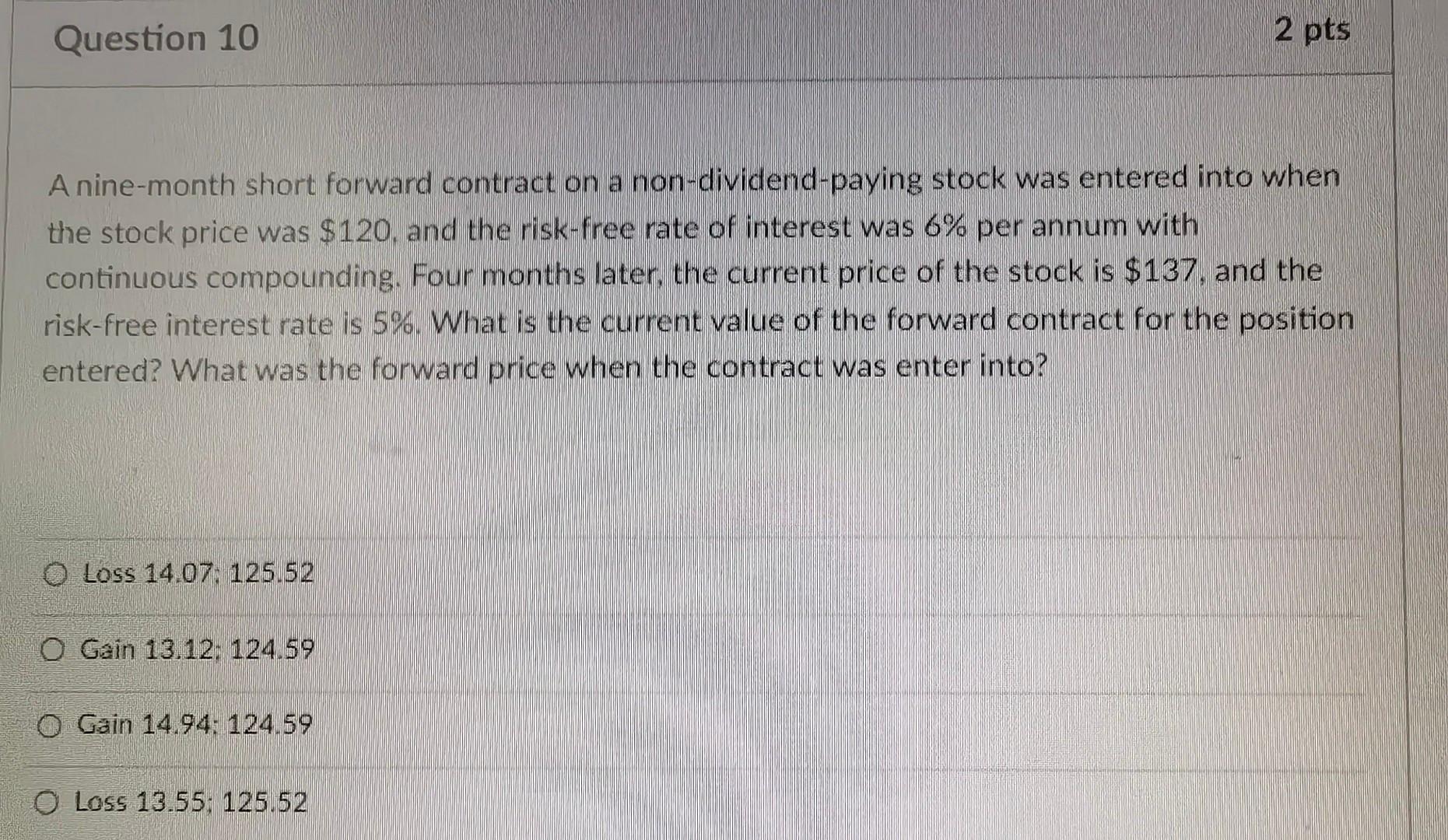

A nine-month short forward contract on a non-dividend-paying stock was entered into when the stock price was $120, and the risk-free rate of interest was

A nine-month short forward contract on a non-dividend-paying stock was entered into when the stock price was $120, and the risk-free rate of interest was 6% per annum with continuous compounding. Four months later, the current price of the stock is $137, and the risk-free interest rate is 5%. What is the current value of the forward contract for the position entered? What was the forward price when the contract was enter into? Loss 14.07;125.52 Gain 13.12;124.59 Gain 14.94:124.59 Loss 13.55;125.52

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Private Equity Value Creation Analysis Volume I

Authors: Michael David Reinard

1st Edition

1736077821, 978-1736077825