Answered step by step

Verified Expert Solution

Question

1 Approved Answer

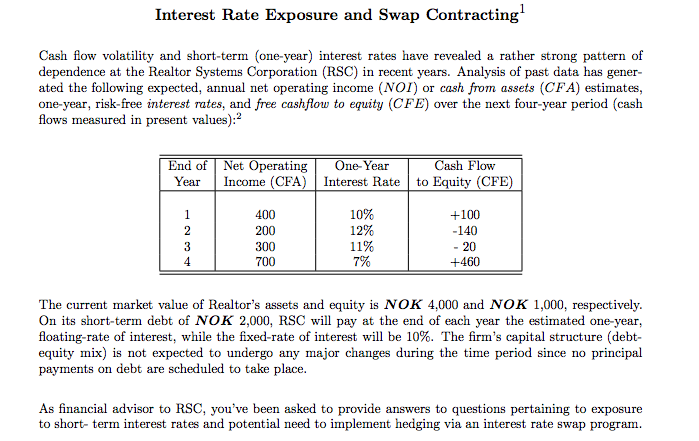

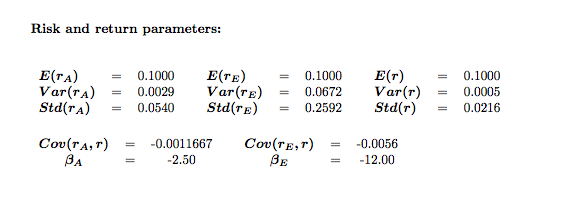

(a) Of total variation (variance) in equity-return, whats the proportion caused by short-term interest rate fluctuations? (b) What is the estimated exposure to short-term interest

(a) Of total variation (variance) in equity-return, whats the proportion caused by short-term interest rate fluctuations?

(b) What is the estimated exposure to short-term interest rate fluctuations over the four-year period?

(c) What type of interest rate swap with respect to notional principal (the NOK-amount) and the position (long or short), is required to hedge the estimated interest rate exposure?

(d) To what extent does the swap-contract suggested in part (c) seem to do the trick in terms of hedging the interest rate exposure?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started