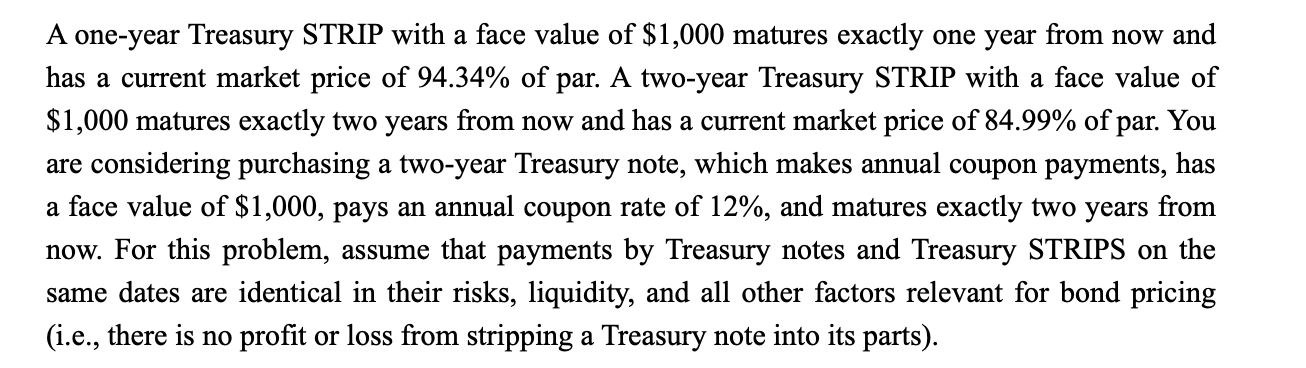

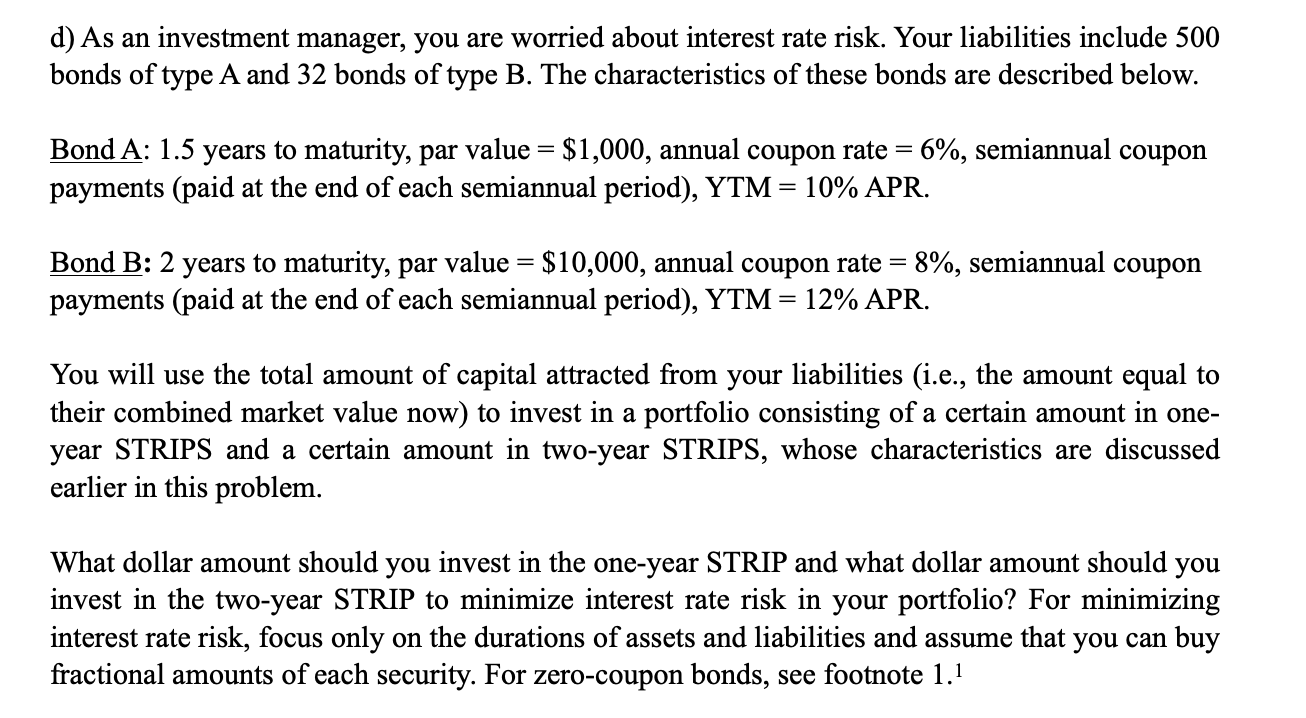

A one-year Treasury STRIP with a face value of $1,000 matures exactly one year from now and has a current market price of 94.34% of par. A two-year Treasury STRIP with a face value of $1,000 matures exactly two years from now and has a current market price of 84.99% of par. You are considering purchasing a two-year Treasury note, which makes annual coupon payments, has a face value of $1,000, pays an annual coupon rate of 12%, and matures exactly two years from now. For this problem, assume that payments by Treasury notes and Treasury STRIPS on the same dates are identical in their risks, liquidity, and all other factors relevant for bond pricing (i.e., there is no profit or loss from stripping a Treasury note into its parts). d) As an investment manager, you are worried about interest rate risk. Your liabilities include 500 bonds of type A and 32 bonds of type B. The characteristics of these bonds are described below. Bond A: 1.5 years to maturity, par value = $1,000, annual coupon rate = 6%, semiannual coupon payments (paid at the end of each semiannual period), YTM = 10% APR. = = Bond B: 2 years to maturity, par value = $10,000, annual coupon rate = 8%, semiannual coupon payments (paid at the end of each semiannual period), YTM = 12% APR. = You will use the total amount of capital attracted from your liabilities (i.e., the amount equal to their combined market value now) to invest in a portfolio consisting of a certain amount in one- year STRIPS and a certain amount in two-year STRIPS, whose characteristics are discussed earlier in this problem. What dollar amount should you invest in the one-year STRIP and what dollar amount should you invest in the two-year STRIP to minimize interest rate risk in your portfolio? For minimizing interest rate risk, focus only on the durations of assets and liabilities and assume that you can buy fractional amounts of each security. For zero-coupon bonds, see footnote 1.1 A one-year Treasury STRIP with a face value of $1,000 matures exactly one year from now and has a current market price of 94.34% of par. A two-year Treasury STRIP with a face value of $1,000 matures exactly two years from now and has a current market price of 84.99% of par. You are considering purchasing a two-year Treasury note, which makes annual coupon payments, has a face value of $1,000, pays an annual coupon rate of 12%, and matures exactly two years from now. For this problem, assume that payments by Treasury notes and Treasury STRIPS on the same dates are identical in their risks, liquidity, and all other factors relevant for bond pricing (i.e., there is no profit or loss from stripping a Treasury note into its parts). d) As an investment manager, you are worried about interest rate risk. Your liabilities include 500 bonds of type A and 32 bonds of type B. The characteristics of these bonds are described below. Bond A: 1.5 years to maturity, par value = $1,000, annual coupon rate = 6%, semiannual coupon payments (paid at the end of each semiannual period), YTM = 10% APR. = = Bond B: 2 years to maturity, par value = $10,000, annual coupon rate = 8%, semiannual coupon payments (paid at the end of each semiannual period), YTM = 12% APR. = You will use the total amount of capital attracted from your liabilities (i.e., the amount equal to their combined market value now) to invest in a portfolio consisting of a certain amount in one- year STRIPS and a certain amount in two-year STRIPS, whose characteristics are discussed earlier in this problem. What dollar amount should you invest in the one-year STRIP and what dollar amount should you invest in the two-year STRIP to minimize interest rate risk in your portfolio? For minimizing interest rate risk, focus only on the durations of assets and liabilities and assume that you can buy fractional amounts of each security. For zero-coupon bonds, see foot