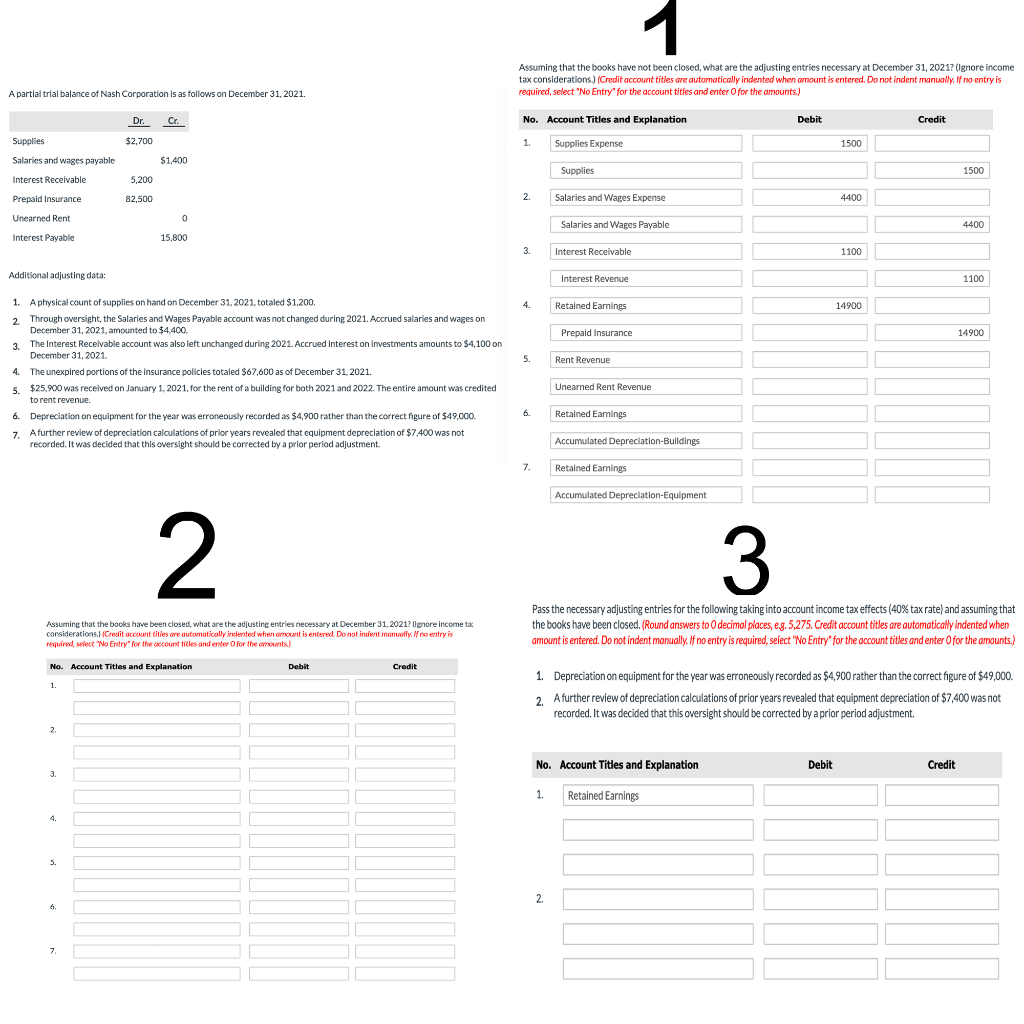

A partial trial balance of Nash Corporation is as follows on December 31, 2021.

Assuming that the books have not been closed, what are the adjusting entries necessary at December 31, 2021? (Ignore income tax considerations.) (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry for the account titles and enter for the amounts) A partial trial balance of Nash Corporation is as follows on December 31, 2021. Cr. No. Account Titles and Explanation Debit Dr. $2,700 Credit 1. Supplies Expense 1500 Supplies Salaries and wages payable Interest Receivable $1,400 Supplies 1500 5,200 82,500 Prepaid Insurance Salaries and Wages Expense 4400 Unearned Rent Salaries and Wages Payable 4400 Interest Pavable 15,800 3. Interest Receivable 1100 Additional adjusting data: Interest Revenue 1100 Retained Earnings 14900 Prepaid Insurance 14900 5. Rent Revenue 1. A physical count of supplies on hand on December 31, 2021, totaled $1,200. 2. Through oversight, the Salaries and Wages Payable account was not changed during 2021. Accrued salaries and wages on December 31, 2021, amounted to $4.400. 3. The Interest Receivable account was also left unchanged during 2021. Accrued Interest on Investments amounts to $4,100 on December 31, 2021 4. The unexpired portions of the insurance policies totaled $67,600 as of December 31, 2021. 5. $25.900 was received on January 1, 2021, for the rent of a building for both 2021 and 2022. The entire amount was credited torent revenue. 6. Depreciation on equipment for the year was erroneously recorded as $4.900 rather than the correct figure of $49.000. 7. A further review of depreciation calculations of prior years revealed that equipment depreciation of $7,400 was not recorded. It was decided that this oversight should be corrected by a prior period adjustment Unearned Rent Revenue Retained Earnings Accumulated Depreciation-Buildings Retained Earnings Accumulated Depreciation-Equipment Assuming that the books have been closed, what are the adjusting entries necessary at December 31, 2021? llenore income ta. considerations.1 Credit account titles are automatically indeed when runt is entered. Do not indent manually. If no entry is required, select "No Entry for the account titles and enter for the amounts? Pass the necessary adjusting entries for the following taking into account income tax effects (40% tax rate) and assuming that the books have been closed. (Round answers to decimal places, eg. 5,275. Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select 'No Entry for the account titles and enter for the amounts.) No. Account Titles and Explanation Debit Credit 1. Depreciation on equipment for the year was erroneously recorded as $4,900 rather than the correct figure of $49,000. 2. Afurther review of depreciation calculations of prior years revealed that equipment depreciation of $7,400 was not recorded. It was decided that this oversight should be corrected by a prior period adjustment. No. Account Titles and Explanation Debit Credit 1. Retained Earnings