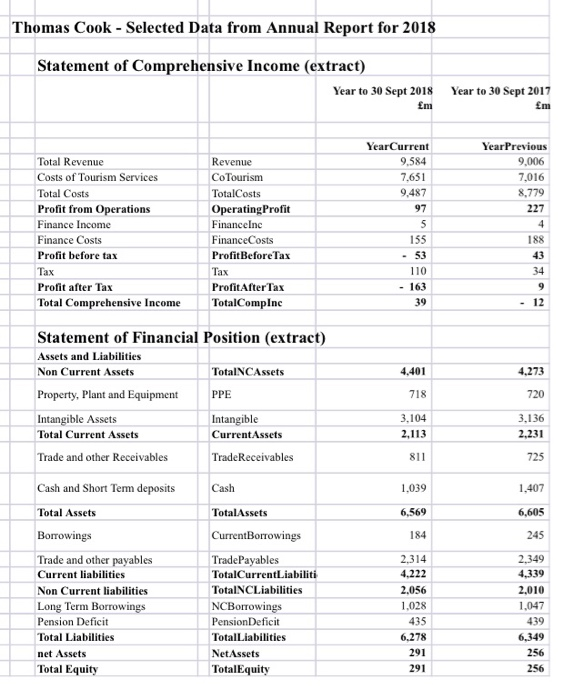

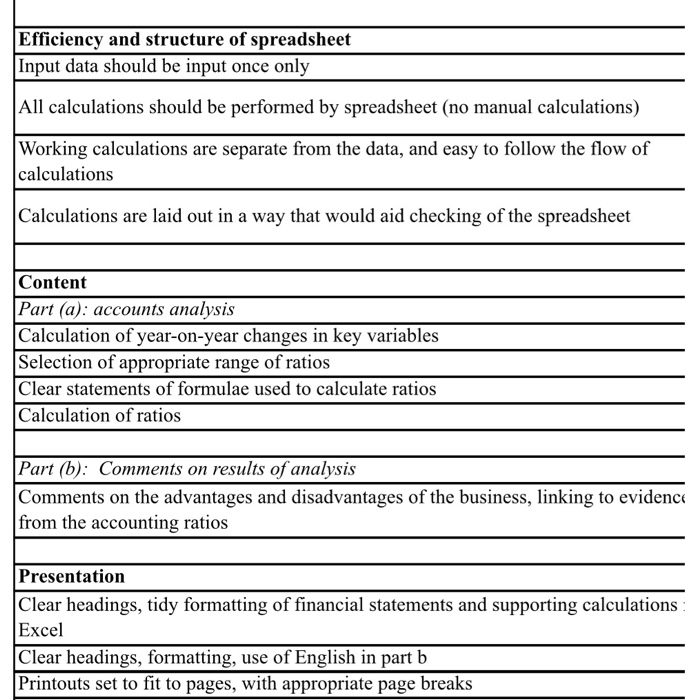

(a) Perform an analysis for the Thomas Cook Group for the years ending 30 September 2018 and 30 September 2017. Your analysis should include identifying the percentage change in key SoCI and SFP items between the two years, as well as covering a range of standard accounting ratios. You should clearly specify the formulae you are using for each ratio. (b) Based on these accounting ratios, and further information from these Accounts, discuss the extent to which is was foreseeable that Thomas Cook would become insolvent. (You may in particular wish to consider the comments on Risks, statements about the Going Concern position, and the Reports of the Audit Committee and Auditor.) [Guide word limit: 400 words ] Thomas Cook - Selected Data from Annual Report for 2018 Statement of Comprehensive Income (extract) Year to 30 Sept 2018 m Year to 30 Sept 2017 m YearCurrent 9.584 7.651 9,487 Total Revenue Costs of Tourism Services Total Costs Profit from Operations Finance Income Finance Costs Profit before tax Year Previous 9,006 7,016 8,779 227 97 5 Revenue Co Tourism TotalCosts Operating Profit FinanceInc FinanceCosts ProfitBefore Tax Tax ProfitAfter Tax TotalCompInc 155 188 - 53 110 34 Profit after Tax Total Comprehensive Income - 163 39 Statement of Financial Position (extract) Assets and Liabilities Non Current Assets TotalNCAssets 4.401 4,273 720 Property, Plant and Equipment PPE 718 Intangible Assets Total Current Assets Intangible Current Assets 3,104 2,113 3,136 2,231 725 Trade and other Receivables TradeReceivables 811 Cash and Short Term deposits Cash 1,039 1,407 Total Assets Total Assets 6,569 6,605 Borrowings Current Borrowings 184 245 Trade and other payables Current liabilities Non Current liabilities Long Term Borrowings Pension Deficit Total Liabilities net Assets Total Equity TradePayables TotalCurrent Liabiliti TotalNCLiabilities NCBorrowings Pension Deficit TotalLiabilities NetAssets TotalEquity 2,314 4.222 2,056 1,028 435 6.278 2.349 4,339 2.010 1,047 439 6,349 256 256 291 291 Efficiency and structure of spreadsheet Input data should be input once only All calculations should be performed by spreadsheet (no manual calculations) Working calculations are separate from the data, and easy to follow the flow of calculations Calculations are laid out in a way that would aid checking of the spreadsheet Content Part (a): accounts analysis Calculation of year-on-year changes in key variables Selection of appropriate range of ratios Clear statements of formulae used to calculate ratios Calculation of ratios Part (b): Comments on results of analysis Comments on the advantages and disadvantages of the business, linking to evidence from the accounting ratios Presentation Clear headings, tidy formatting of financial statements and supporting calculations Excel Clear headings, formatting, use of English in part b Printouts set to fit to pages, with appropriate page breaks