A portfolio consisting of Stocks 1 and has an expected return of 14%. What is the standard deviation of this portfolio given the information

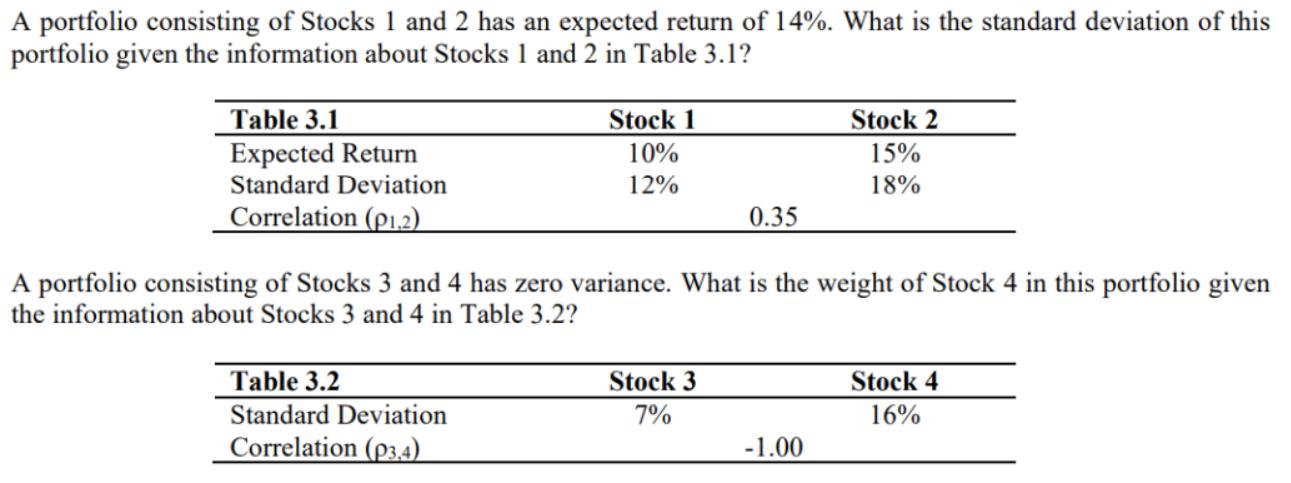

A portfolio consisting of Stocks 1 and has an expected return of 14%. What is the standard deviation of this portfolio given the information about Stocks 1 and 2 in Table 3.1? Table 3.1 Expected Return Standard Deviation Correlation (P1,2) Stock 1 10% 12% Table 3.2 Standard Deviation Correlation (p3,4) 0.35 A portfolio consisting of Stocks 3 and 4 has zero variance. What is the weight of Stock 4 in this portfolio given the information about Stocks 3 and 4 in Table 3.2? Stock 3 7% Stock 2 15% 18% -1.00 Stock 4 16%

Step by Step Solution

3.46 Rating (166 Votes )

There are 3 Steps involved in it

Step: 1

Get step-by-step solutions from verified subject matter experts

100% Satisfaction Guaranteed-or Get a Refund!

Step: 2Unlock detailed examples and clear explanations to master concepts

Step: 3Unlock to practice, ask and learn with real-world examples

See step-by-step solutions with expert insights and AI powered tools for academic success

-

Access 30 Million+ textbook solutions.

Access 30 Million+ textbook solutions.

-

Ask unlimited questions from AI Tutors.

-

Order free textbooks.

-

100% Satisfaction Guaranteed-or Get a Refund!

Claim Your Hoodie Now!

Authors: Eugene F. Brigham, Joel F. Houston

Concise 6th Edition

324664559, 978-0324664553

Study Smart with AI Flashcards

Access a vast library of flashcards, create your own, and experience a game-changing transformation in how you learn and retain knowledge

Explore Flashcards