Answered step by step

Verified Expert Solution

Question

1 Approved Answer

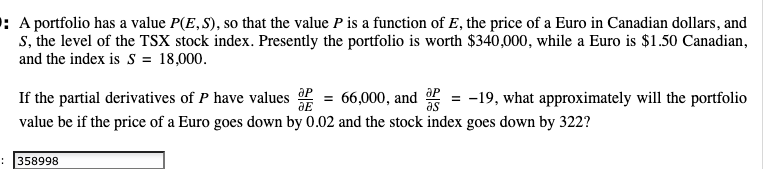

A portfolio has a value P ( E , S ) , so that the value P is a function of E , the price

A portfolio has a value PES so that the value P is a function of E the price of a Euro in Canadian dollars, and S the level of the TSX stock index. Presently the portfolio is worth $ while a Euro is $ Canadian, and the index is S

If the partial derivatives of P have values

P

E

and

P

S

what approximately will the portfolio value be if the price of a Euro goes down by and the stock index goes down by A portfolio has a value so that the value is a function of the price of a Euro in Canadian dollars, and

the level of the TSX stock index. Presently the portfolio is worth $ while a Euro is $ Canadian,

and the index is

If the partial derivatives of have values and what approximately will the portfolio

value be if the price of a Euro goes down by and the stock index goes down by

NO please answer question

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Theoretical Foundations For Quantitative Finance

Authors: Luca Spadafora, Gennady P Berman

1st Edition

9813202475, 978-9813202474