Answered step by step

Verified Expert Solution

Question

1 Approved Answer

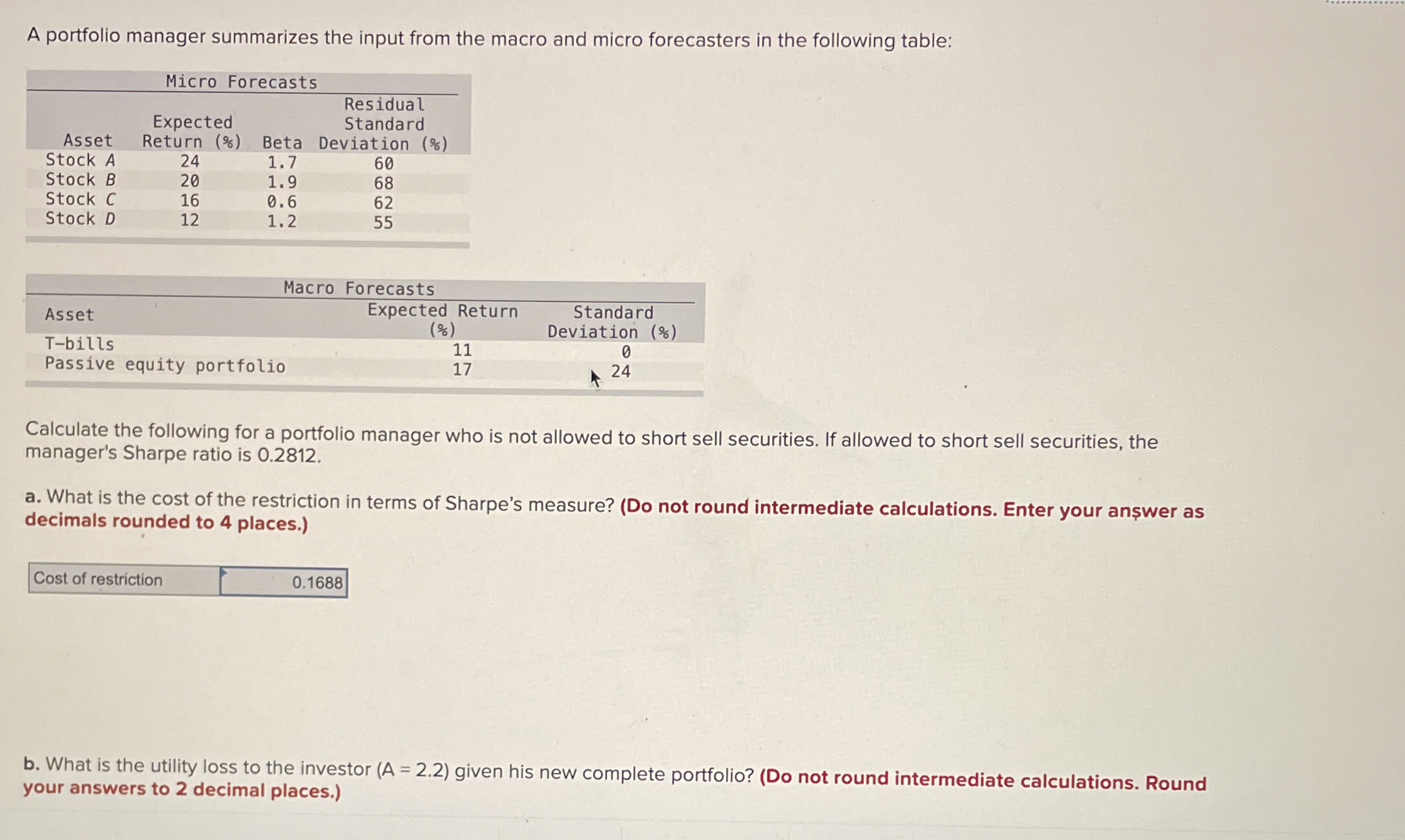

A portfolio manager summarizes the input from the macro and micro forecasters in the following table: table [ [ Micro Forecasts ] , [

A portfolio manager summarizes the input from the macro and micro forecasters in the following table:

tableMicro ForecastsResidualAssetandardExpected,,Return Beta,Deviation Stock AStock BStock CStock D

tableMacro Forecasts,AssetExpected Return,Standard,,Tbills,Deviation Passive equity portfolio,

Calculate the following for a portfolio manager who is not allowed to short sell securities If allowed to short sell securities the manager's Sharpe ratio is

a What is the cost of the restriction in terms of Sharpe's measure? Do not round intermediate calculations. Enter your answer as decimals rounded to places.

Cost of restriction

b What is the utility loss to the investor

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started