Question

A portfolio manager, who has a bond portfolio with a value of $10 million and duration of 6 years, is interested in immunizing the portfolio

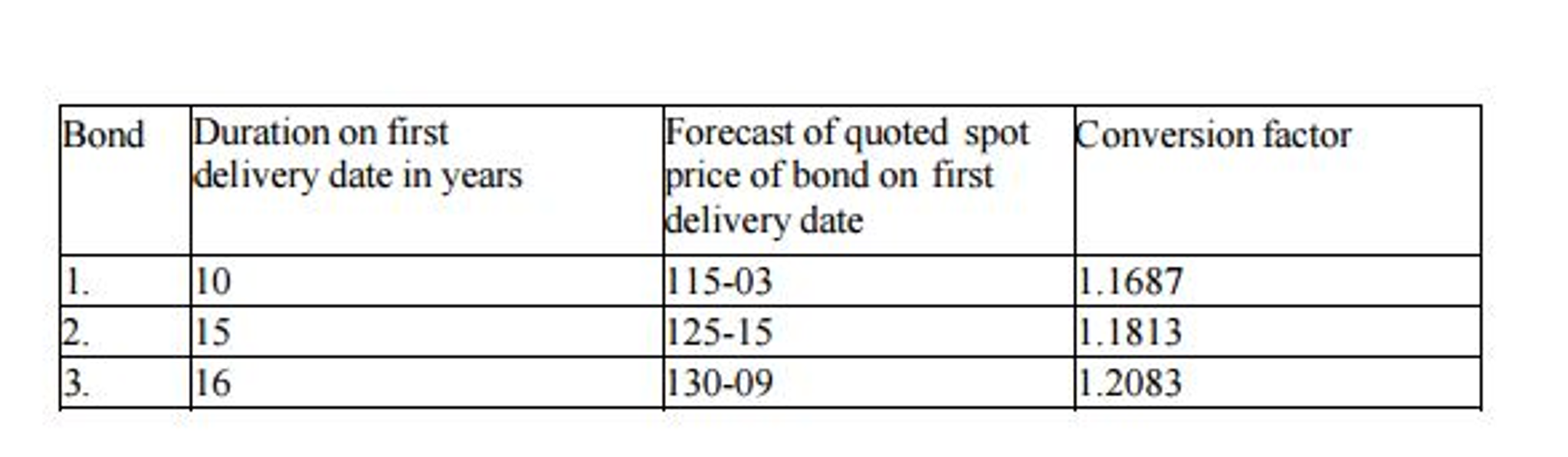

A portfolio manager, who has a bond portfolio with a value of $10 million and duration of 6 years, is interested in immunizing the portfolio against changes in interest rates over the next 2 months. Suppose that the closest-to-maturity Treasury bond futures contract traded on the Chicago Board of Trade has a size of $100,000 face value, a quoted futures price of 98-15, and a delivery month in 3 months. Assume that the following three bonds are eligible for delivery.

a) Which of the above three bonds is cheapest to deliver (CTD)?

b) How should the portfolio manager immunize the bond portfolio against changes in interest rates over the next 2 months? In your answer clearly specify his position in the Treasury bond futures contract (buy/sell) and the number of contracts.

Forecast of quoted spot price of bond on first elivery date 115-03 125-15 130-09 Duration on first delivery date in years Bond Conversion factor 10 15 16 1.1687 1.1813 1.2083 3

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Lifestyle Investor

Authors: Justin Donald, Ryan Levesque, Mike Koenigs

1st Edition

1636800130, 978-1636800134