Answered step by step

Verified Expert Solution

Question

1 Approved Answer

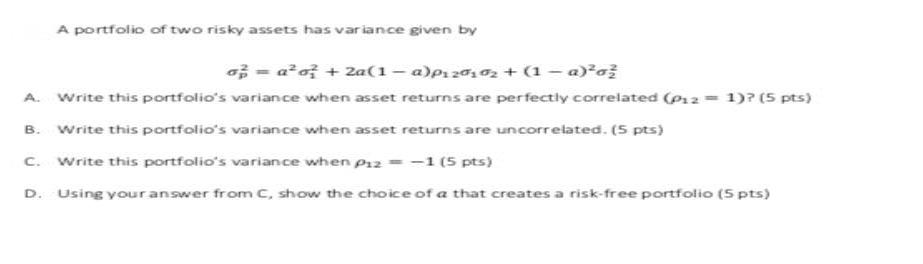

A portfolio of two risky assets has variance given by o = a?o? + 2a(1- a)p120,02 + (1 - a)*a A. Write this portfolio's

A portfolio of two risky assets has variance given by o = a?o? + 2a(1- a)p120,02 + (1 - a)*a A. Write this portfolio's variance when asset returns are perfectily correlated (P2= 1)? (5 pts) B. Write this portfolio's variance when asset returns are uncorrelated. (5 pts) c. write this portfolio's variance when p12 = -1 (5 pts) D. Using youranswer from C, show the choice of a that creates a risk-free portfolio (5 pts)

Step by Step Solution

★★★★★

3.39 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

when P12 1 of ao1 1 ao2 b when ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials of Investments

Authors: Zvi Bodie, Alex Kane, Alan Marcus

9th edition

78034698, 978-0077502287, 77502280, 978-0078034695