Answered step by step

Verified Expert Solution

Question

1 Approved Answer

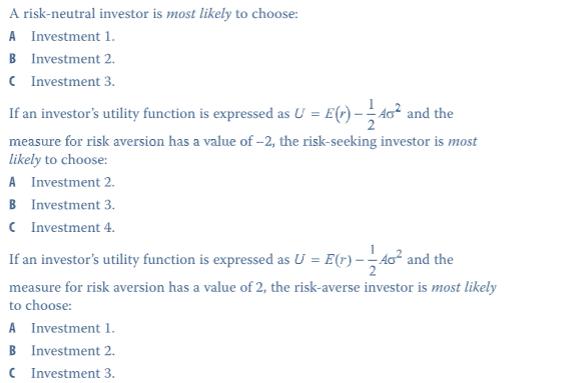

A risk-neutral investor is most likely to choose: A Investment 1. B Investment 2. (Investment 3. If an investor's utility function is expressed as

A risk-neutral investor is most likely to choose: A Investment 1. B Investment 2. (Investment 3. If an investor's utility function is expressed as U = E() ---40 and the measure for risk aversion has a value of -2, the risk-seeking investor is most likely to choose: A Investment 2. B Investment 3. C Investment 4. If an investor's utility function is expressed as U = E(r) - - -40 and the measure for risk aversion has a value of 2, the risk-averse investor is most likely to choose: A Investment 1. B Investment 2. C Investment 3. Investment 1 2 3 Return (%) 18. 19 20 18. Standard Deviation (%) 2859 15 30

Step by Step Solution

★★★★★

3.52 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microeconomics An Intuitive Approach with Calculus

Authors: Thomas Nechyba

1st edition

538453257, 978-0538453257