Answered step by step

Verified Expert Solution

Question

1 Approved Answer

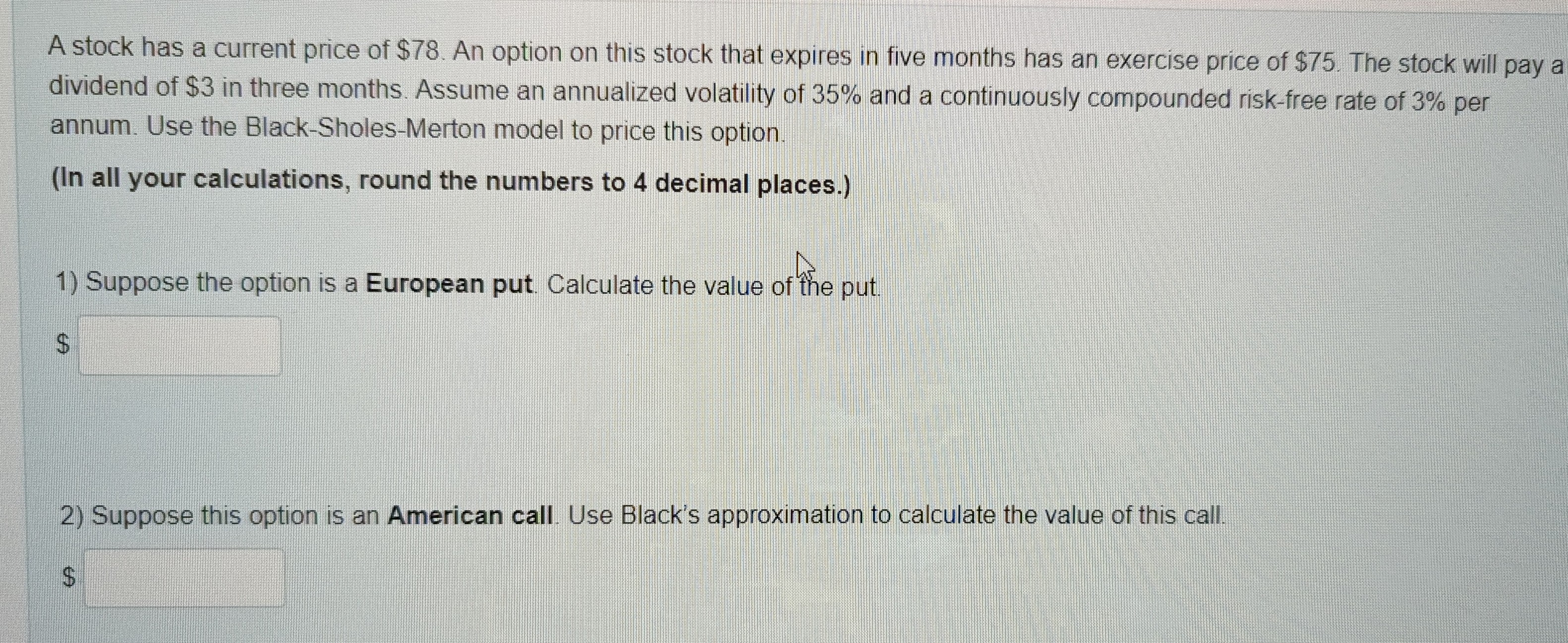

A stock has a current price of $ 7 8 . An option on this stock that expires in five months has an exercise price

A stock has a current price of $ An option on this stock that expires in five months has an exercise price of $ The stock will pay a

dividend of $ in three months. Assume an annualized volatility of and a continuously compounded riskfree rate of per

annum. Use the BlackSholesMerton model to price this option.

In all your calculations, round the numbers to decimal places.

Suppose the option is a European put. Calculate the value of the put.

$

Suppose this option is an American call. Use Black's approximation to calculate the value of this call.

$

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Sustainable Development

Authors: Magdalena Ziolo

1st Edition

0367819767, 978-0367819767