Answered step by step

Verified Expert Solution

Question

1 Approved Answer

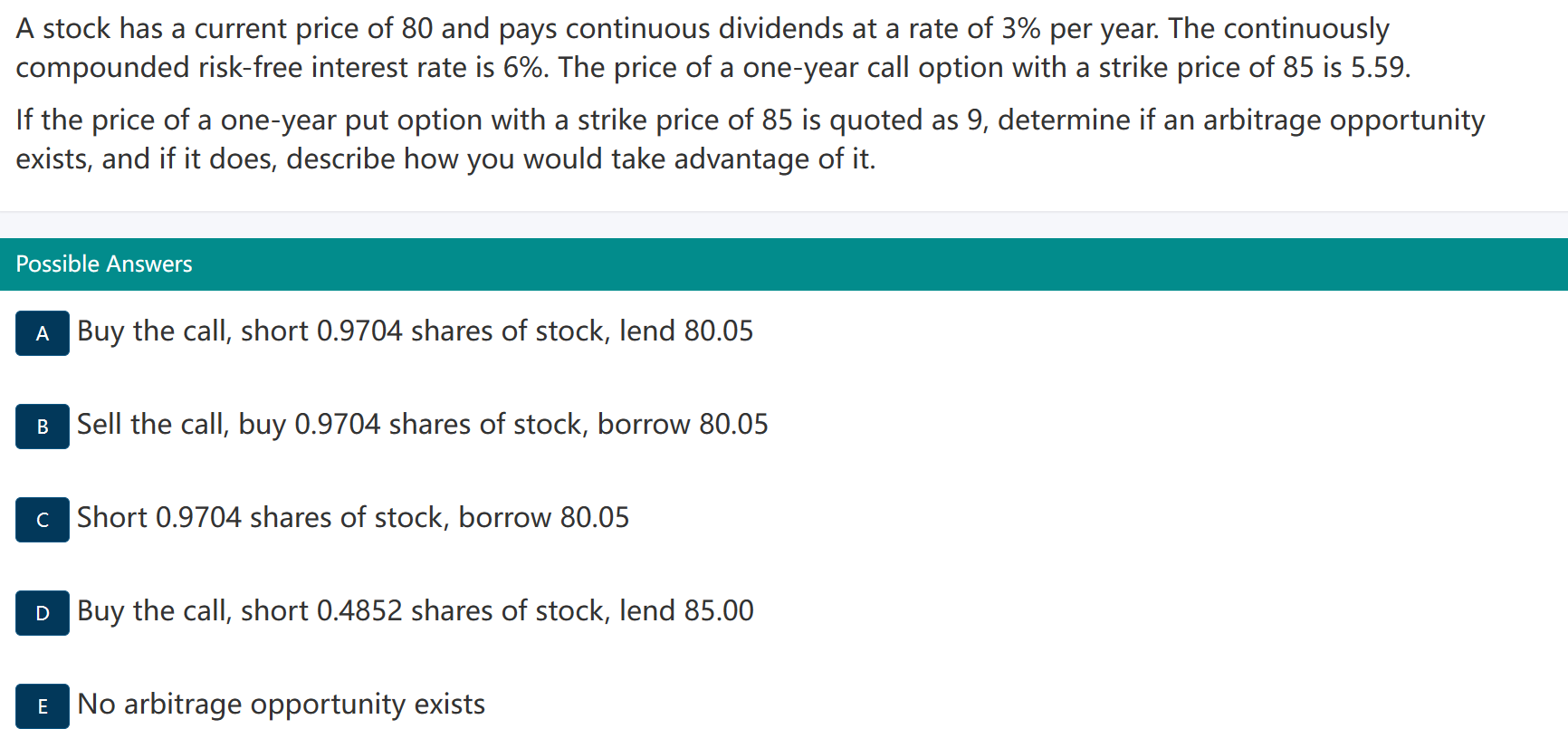

A stock has a current price of 80 and pays continuous dividends at a rate of 3% per year. The continuously compounded risk-free interest rate

A stock has a current price of 80 and pays continuous dividends at a rate of 3% per year. The continuously compounded risk-free interest rate is 6\%. The price of a one-year call option with a strike price of 85 is 5.59 . If the price of a one-year put option with a strike price of 85 is quoted as 9 , determine if an arbitrage opportunity exists, and if it does, describe how you would take advantage of it. Possible Answers Buy the call, short 0.9704 shares of stock, lend 80.05 Sell the call, buy 0.9704 shares of stock, borrow 80.05 Short 0.9704 shares of stock, borrow 80.05 Buy the call, short 0.4852 shares of stock, lend 85.00 No arbitrage opportunity exists

A stock has a current price of 80 and pays continuous dividends at a rate of 3% per year. The continuously compounded risk-free interest rate is 6\%. The price of a one-year call option with a strike price of 85 is 5.59 . If the price of a one-year put option with a strike price of 85 is quoted as 9 , determine if an arbitrage opportunity exists, and if it does, describe how you would take advantage of it. Possible Answers Buy the call, short 0.9704 shares of stock, lend 80.05 Sell the call, buy 0.9704 shares of stock, borrow 80.05 Short 0.9704 shares of stock, borrow 80.05 Buy the call, short 0.4852 shares of stock, lend 85.00 No arbitrage opportunity exists Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Asset Pricing Theory

Authors: Claus MUNK

1st Edition

0198716451, 978-0198716457