Answered step by step

Verified Expert Solution

Question

1 Approved Answer

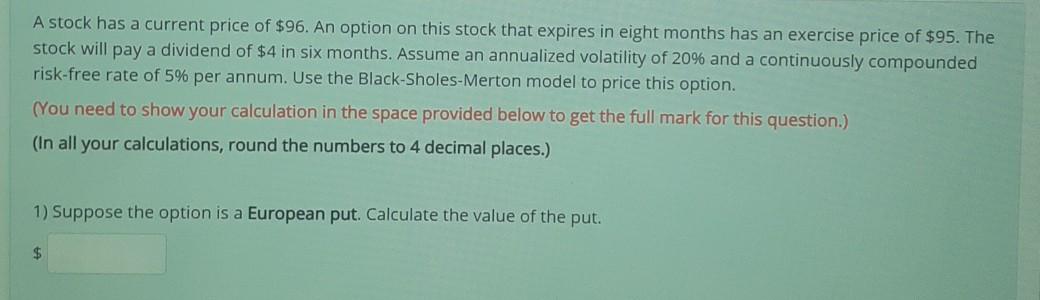

A stock has a current price of $96. An option on this stock that expires in eight months has an exercise price of $95. The

A stock has a current price of $96. An option on this stock that expires in eight months has an exercise price of $95. The stock will pay a dividend of $4 in six months. Assume an annualized volatility of 20% and a continuously compounded risk-free rate of 5% per annum. Use the Black-Sholes-Merton model to price this option. (You need to show your calculation in the space provided below to get the full mark for this question.) (In all your calculations, round the numbers to 4 decimal places.) 1) Suppose the option is a European put. Calculate the value of the put. $

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Economics Discussion Series Errors In The Measurement Of The Output Gap And The Design Of Monetary Policy

Authors: United States Federal Reserve Board, Athanasios Orphanides

1st Edition

1288717849, 9781288717842