Answered step by step

Verified Expert Solution

Question

1 Approved Answer

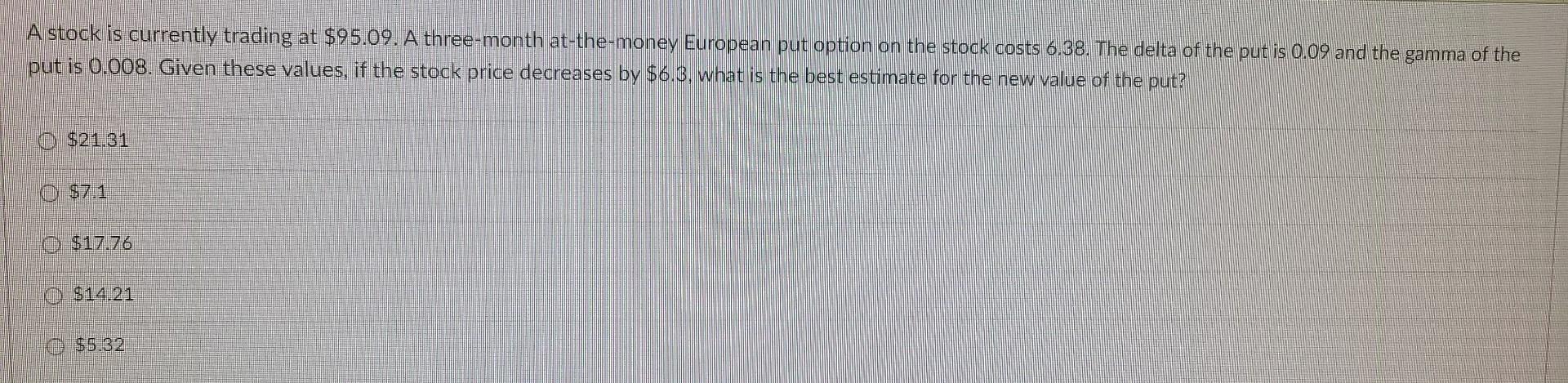

A stock is currently trading at $95.09. A three-month at-the-money European put option on the stock costs 6.38 . The delta of the put is

A stock is currently trading at \$95.09. A three-month at-the-money European put option on the stock costs 6.38 . The delta of the put is 0.09 and the gamma of the put is 0.008 . Given these values, if the stock price decreases by $6.3, what is the best estimate for the new value of the put? $21.31 $7.1 $17.76 $14.21 $5.32

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin Guidebook 32 Funny And Surprising Stories Of Real Experiences With Bitcoin

Authors: Gabriella Garverick

1st Edition

979-8354122462