A stock price is currently $100. A call option on this stock with a strike price of $100 and one year to maturity costs $13.61.

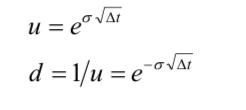

A stock price is currently $100. A call option on this stock with a strike price of $100 and one year to maturity costs $13.61. The continuous-time interest rate is 5%. By using a one-step binomial tree, estimate the expected volatility level (σ) for the stock. Assume that u and d are modeled as below.

( Excel's Goal Seek will help solving this and will be much appreciated to be posted to see how it has been used to solve this problem, thanks)

u = eVAr d = 1/u = e oV

Step by Step Solution

3.40 Rating (147 Votes )

There are 3 Steps involved in it

Step: 1

Design the template like this Feed the formula like ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: John C. Hull

8th edition

978-1292155036, 1292155035, 132993341, 978-0132993340