Answered step by step

Verified Expert Solution

Question

1 Approved Answer

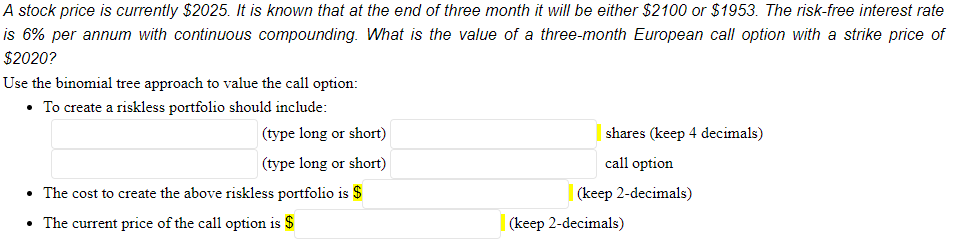

A stock price is currently $2025. It is known that at the end of three month it will be either $2100 or $1953. The risk-free

A stock price is currently $2025. It is known that at the end of three month it will be either $2100 or $1953. The risk-free interest rate is 6% per annum with continuous compounding. What is the value of a three-month European call option with a strike price of $2020? Use the binomial tree approach to value the call option: - To create a riskless portfolio should include: (typelongorshort)(typelongorshort)calloptionlessportfoliois$(keep2-decimals)shares(keep4decimals)(keep2-decimals)

A stock price is currently $2025. It is known that at the end of three month it will be either $2100 or $1953. The risk-free interest rate is 6% per annum with continuous compounding. What is the value of a three-month European call option with a strike price of $2020? Use the binomial tree approach to value the call option: - To create a riskless portfolio should include: (typelongorshort)(typelongorshort)calloptionlessportfoliois$(keep2-decimals)shares(keep4decimals)(keep2-decimals) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Family Matters Making The Right Financial Decision For Your Filipino Family

Authors: Belen Loreto Grand

1st Edition

1683509544, 978-1683509547