Answered step by step

Verified Expert Solution

Question

1 Approved Answer

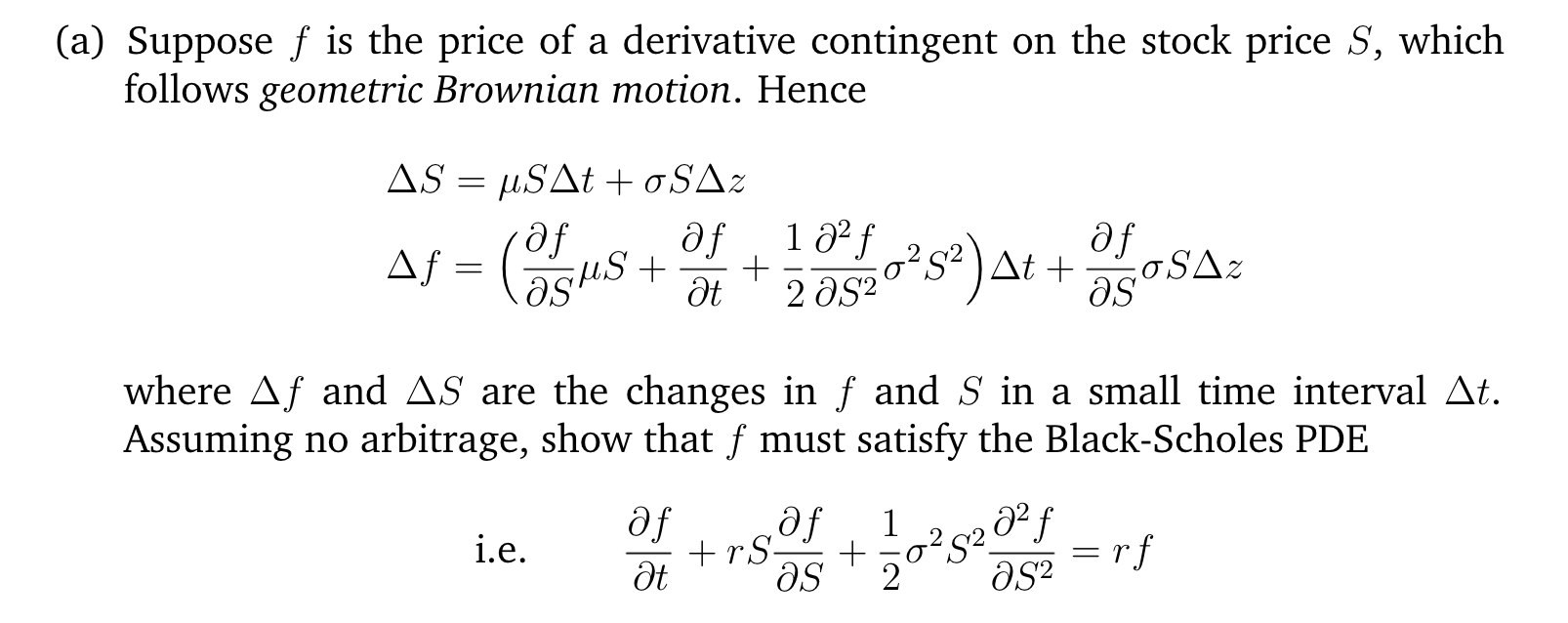

a) Suppose f is the price of a derivative contingent on the stock price S, which follows geometric Brownian motion. Hence S=St+Szf=(SfS+tf+21S22f2S2)t+SfSz where f and

a) Suppose f is the price of a derivative contingent on the stock price S, which follows geometric Brownian motion. Hence S=St+Szf=(SfS+tf+21S22f2S2)t+SfSz where f and S are the changes in f and S in a small time interval t. Assuming no arbitrage, show that f must satisfy the Black-Scholes PDE i.e.tf+rSSf+212S2S22f=rf

a) Suppose f is the price of a derivative contingent on the stock price S, which follows geometric Brownian motion. Hence S=St+Szf=(SfS+tf+21S22f2S2)t+SfSz where f and S are the changes in f and S in a small time interval t. Assuming no arbitrage, show that f must satisfy the Black-Scholes PDE i.e.tf+rSSf+212S2S22f=rf Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Healthcare Financial Management

Authors: Louis C. Gapenski, George H. Pink

6th Edition

1567933629, 9781567933628