Answered step by step

Verified Expert Solution

Question

1 Approved Answer

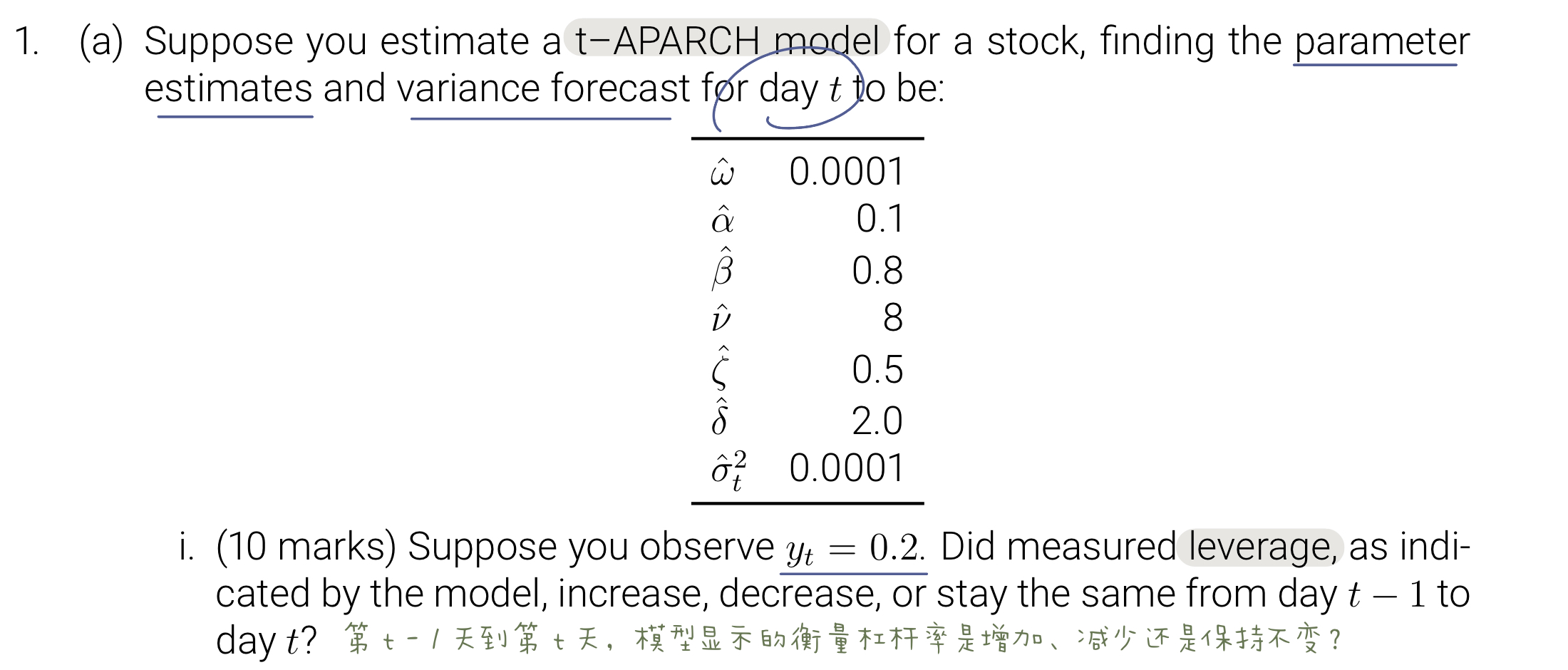

( a ) Suppose you estimate a t - APARCH model for a stock, finding the parameter estimates and variance forecast for day t to

a Suppose you estimate a tAPARCH model for a stock, finding the parameter estimates and variance forecast for day to be: i marks Suppose you observe Did measured leverage, as indi cated by the model, increase, decrease, or stay the same from day to day

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Database And Expert Systems Applications Dexa 2023 Workshops 34th International Conference Dexa 2023 Penang Malaysia August 28 30 2023 Proceedings

Authors: Gabriele Kotsis ,A Min Tjoa ,Ismail Khalil ,Bernhard Moser ,Atif Mashkoor ,Johannes Sametinger ,Maqbool Khan

1st Edition