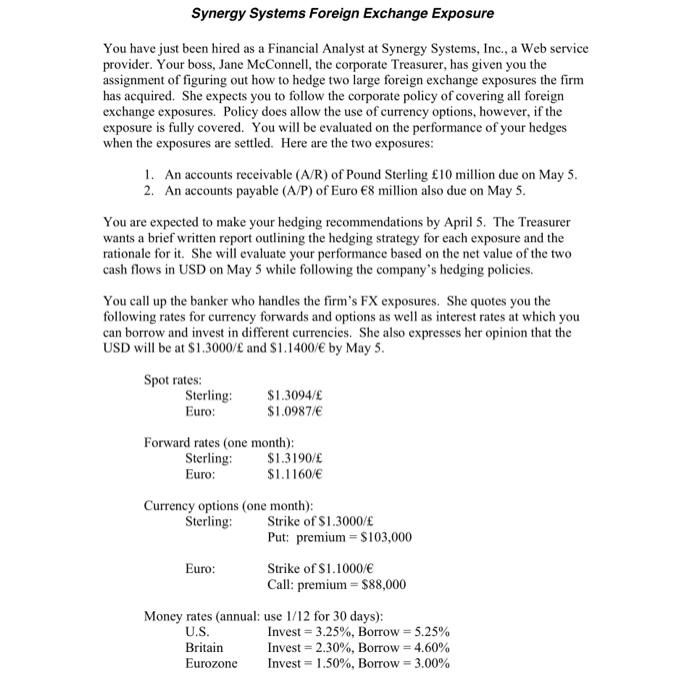

a Synergy Systems Foreign Exchange Exposure You have just been hired as a Financial Analyst at Synergy Systems, Inc., a Web service provider. Your boss, Jane McConnell, the corporate Treasurer, has given you the assignment of figuring out how to hedge two large foreign exchange exposures the firm has acquired. She expects you to follow the corporate policy of covering all foreign exchange exposures. Policy does allow the use of currency options, however, if the exposure is fully covered. You will be evaluated on the performance of your hedges when the exposures are settled. Here are the two exposures: 1. An accounts receivable (A/R) of Pound Sterling 10 million due on May 5. 2. An accounts payable (A/P) of Euro 8 million also due on May 5. You are expected to make your hedging recommendations by April 5. The Treasurer wants a brief written report outlining the hedging strategy for each exposure and the rationale for it. She will evaluate your performance based on the net value of the two cash flows in USD on May 5 while following the company's hedging policies. You call up the banker who handles the firm's FX exposures. She quotes you the following rates for currency forwards and options as well as interest rates at which you can borrow and invest in different currencies. She also expresses her opinion that the USD will be at $1.3000/ and $1.1400/ by May 5. Spot rates: Sterling: Euro: $1.3094/ $1.0987/ Forward rates (one month): Sterling: $1.3190/ Euro: $1.1160/ Currency options (one month); Sterling: Strike of $1.3000/ Put: premium = $103,000 Euro: Strike of S1.1000 Call: premium = $88,000 Money rates (annual: use 1/12 for 30 days): U.S. Invest = 3.25%, Borrow = 5.25% Britain Invest = 2.30%, Borrow = 4.60% Eurozone Invest = 1.50%, Borrow 3.00% a Synergy Systems Foreign Exchange Exposure You have just been hired as a Financial Analyst at Synergy Systems, Inc., a Web service provider. Your boss, Jane McConnell, the corporate Treasurer, has given you the assignment of figuring out how to hedge two large foreign exchange exposures the firm has acquired. She expects you to follow the corporate policy of covering all foreign exchange exposures. Policy does allow the use of currency options, however, if the exposure is fully covered. You will be evaluated on the performance of your hedges when the exposures are settled. Here are the two exposures: 1. An accounts receivable (A/R) of Pound Sterling 10 million due on May 5. 2. An accounts payable (A/P) of Euro 8 million also due on May 5. You are expected to make your hedging recommendations by April 5. The Treasurer wants a brief written report outlining the hedging strategy for each exposure and the rationale for it. She will evaluate your performance based on the net value of the two cash flows in USD on May 5 while following the company's hedging policies. You call up the banker who handles the firm's FX exposures. She quotes you the following rates for currency forwards and options as well as interest rates at which you can borrow and invest in different currencies. She also expresses her opinion that the USD will be at $1.3000/ and $1.1400/ by May 5. Spot rates: Sterling: Euro: $1.3094/ $1.0987/ Forward rates (one month): Sterling: $1.3190/ Euro: $1.1160/ Currency options (one month); Sterling: Strike of $1.3000/ Put: premium = $103,000 Euro: Strike of S1.1000 Call: premium = $88,000 Money rates (annual: use 1/12 for 30 days): U.S. Invest = 3.25%, Borrow = 5.25% Britain Invest = 2.30%, Borrow = 4.60% Eurozone Invest = 1.50%, Borrow 3.00%