Answered step by step

Verified Expert Solution

Question

1 Approved Answer

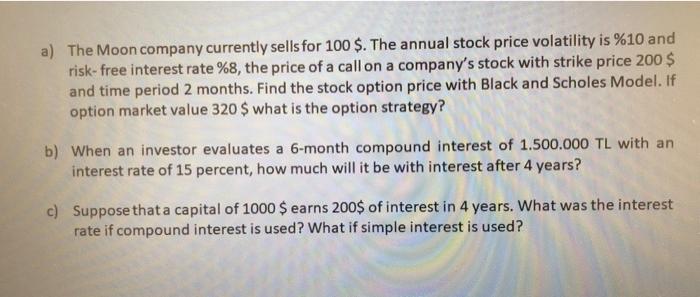

a) The Moon company currently sells for 100 $. The annual stock price volatility is %10 and risk- free interest rate %8, the price of

a) The Moon company currently sells for 100 $. The annual stock price volatility is %10 and risk- free interest rate %8, the price of a call on a companys stock with strike price 200 $ and time period 2 months. Find the stock option price with Black and Scholes Model. If option market value 320 $ what is the option strategy

b) When an investor evaluates a 6-month compound interest of 1.500.000 TL with an interest rate of 15 percent, how much will it be with interest after 4 years?

c) Suppose that a capital of 1000 $ earns 200$ of interest in 4 years. What was the interest rate if compound interest is used? What if simple interest is used?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Essential Nonprofit Fundraising Handbook

Authors: Michael A. Sand, Linda Lysakowski

1st Edition

1601630727, 978-1601630728