Question

A trader holds a complicated portfolio whose value depends on the price of a stock. The trader wants to manage this risk. To do so,

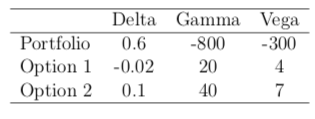

A trader holds a complicated portfolio whose value depends on the price of a stock. The trader wants to manage this risk. To do so, the trader can take positions (long or short) in the underlying stock and in two options on the stock. The Delta, Gamma, and Vega of the portfolio and the two options are given below. What position in the two options and the stock (in addition to the portfolio already held) can make the traders combined position Gamma neutral, Vega neutral, and Delta neutral?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Swing And Position Trading For Beginners Easy To Learn High Profit Method For Beginners

Authors: J.r. Lira

1st Edition

1542338522, 978-1542338523