Answered step by step

Verified Expert Solution

Question

1 Approved Answer

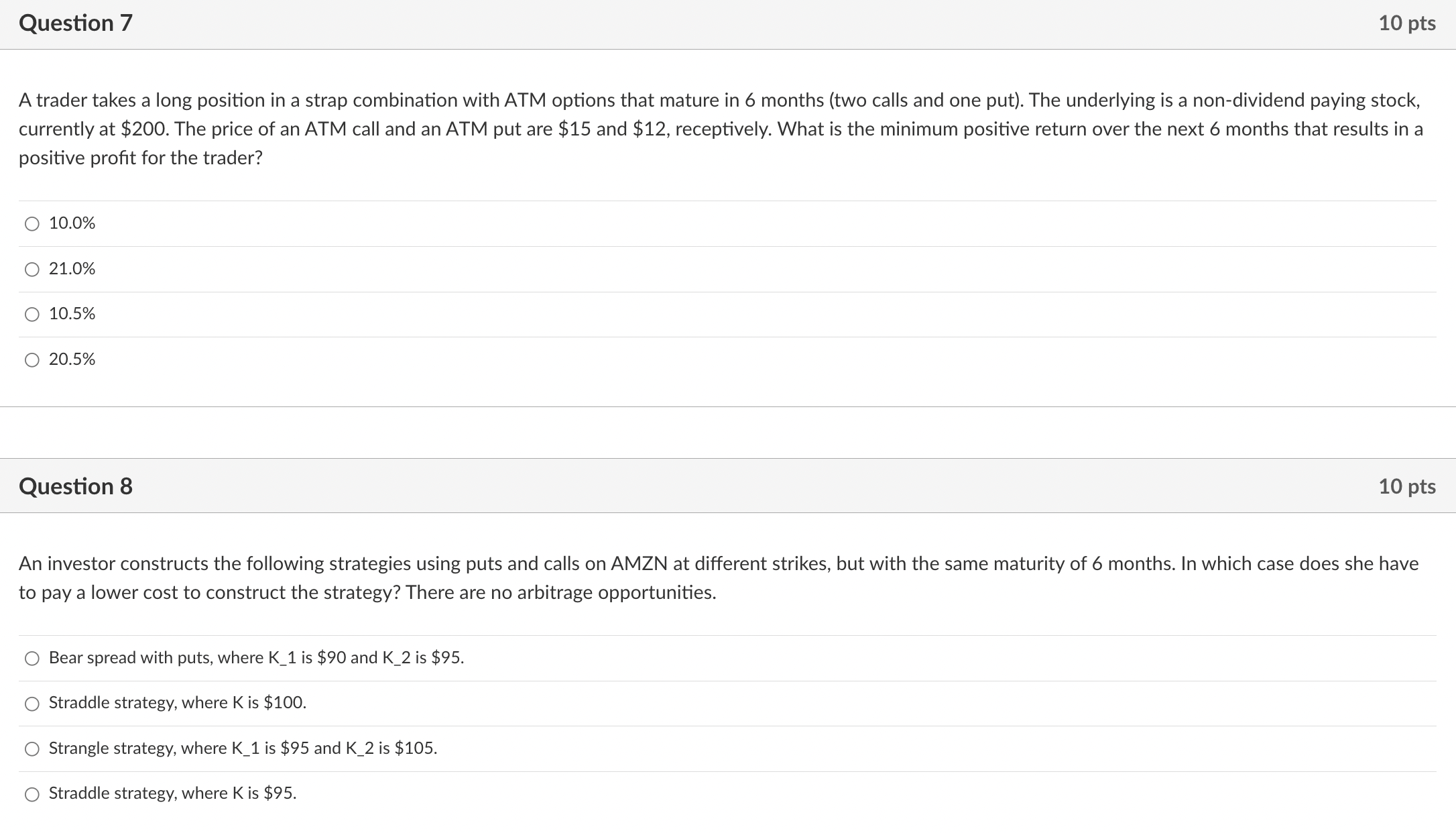

A trader takes a long position in a strap combination with ATM options that mature in 6 months (two calls and one put). The underlying

A trader takes a long position in a strap combination with ATM options that mature in 6 months (two calls and one put). The underlying is a non-dividend paying stock, currently at $200. The price of an ATM call and an ATM put are $15 and $12, receptively. What is the minimum positive return over the next 6 months that results in a positive profit for the trader? Question 8 10 pts An investor constructs the following strategies using puts and calls on AMZN at different strikes, but with the same maturity of 6 months. In which case does she have to pay a lower cost to construct the strategy? There are no arbitrage opportunities. Bear spread with puts, where K1 is $90 and K2 is $95. Straddle strategy, where K is $100. Strangle strategy, where K_1 is $95 and K_2 is $105. Straddle strategy, where K is $95. A trader takes a long position in a strap combination with ATM options that mature in 6 months (two calls and one put). The underlying is a non-dividend paying stock, currently at $200. The price of an ATM call and an ATM put are $15 and $12, receptively. What is the minimum positive return over the next 6 months that results in a positive profit for the trader? Question 8 10 pts An investor constructs the following strategies using puts and calls on AMZN at different strikes, but with the same maturity of 6 months. In which case does she have to pay a lower cost to construct the strategy? There are no arbitrage opportunities. Bear spread with puts, where K1 is $90 and K2 is $95. Straddle strategy, where K is $100. Strangle strategy, where K_1 is $95 and K_2 is $105. Straddle strategy, where K is $95

A trader takes a long position in a strap combination with ATM options that mature in 6 months (two calls and one put). The underlying is a non-dividend paying stock, currently at $200. The price of an ATM call and an ATM put are $15 and $12, receptively. What is the minimum positive return over the next 6 months that results in a positive profit for the trader? Question 8 10 pts An investor constructs the following strategies using puts and calls on AMZN at different strikes, but with the same maturity of 6 months. In which case does she have to pay a lower cost to construct the strategy? There are no arbitrage opportunities. Bear spread with puts, where K1 is $90 and K2 is $95. Straddle strategy, where K is $100. Strangle strategy, where K_1 is $95 and K_2 is $105. Straddle strategy, where K is $95. A trader takes a long position in a strap combination with ATM options that mature in 6 months (two calls and one put). The underlying is a non-dividend paying stock, currently at $200. The price of an ATM call and an ATM put are $15 and $12, receptively. What is the minimum positive return over the next 6 months that results in a positive profit for the trader? Question 8 10 pts An investor constructs the following strategies using puts and calls on AMZN at different strikes, but with the same maturity of 6 months. In which case does she have to pay a lower cost to construct the strategy? There are no arbitrage opportunities. Bear spread with puts, where K1 is $90 and K2 is $95. Straddle strategy, where K is $100. Strangle strategy, where K_1 is $95 and K_2 is $105. Straddle strategy, where K is $95 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Behavioral Finance

Authors: Edwin Burton, Sunit N. Shah

1st Edition

111830019X, 978-1118300190