Question

a) Under the Expectations Theory, calculate the expected (1-year) interest rates implied by the 10/05/20 yield curve for next year and the year after that;

a) Under the Expectations Theory, calculate the expected (1-year) interest rates implied by the 10/05/20 yield curve for next year and the year after that; i.e. find i2021 and iżo22.

Liquidity Premium Incorporated uses the Liquidity Premium Theory. On 10/05/20 they forecasts that (1-year) interest rates are going to be higher over the next two years at .19%; i.e. i oz1 = 2022 = 0.19%.

b) What risk premiums are they using?

(c) Using the liquidity premiums you have calculated in part (b), update the nominal interest rate forecast for 2022 using the data from the next day (10/06/20).

(d) Nowadays Germany and France in Europe are issuing 10-year bonds of negative yields. Why investors still buying them? Give two reasons. The YTM on the bond is 3% and the coupon rate is 7% with annual coupons.

(e) What is its price if it is a 30-year bond and has a face value of 10,000

(f) What is the one-year Rate of Return (RET) on the bond if the yield to maturity rises to 5%?

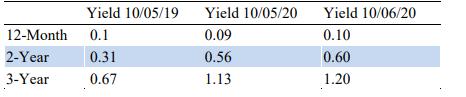

The following are Canadian government bond yields.

Yield 10/05/19 Yield 10/05/20 Yield 10/06/20 12-Month 0.1 0.09 0.10 2-Year 0.31 0.56 0.60 3-Year 0.67 1.13 1.20

Yield 10/05/19 12-Month 0.1 2-Year 0.31 3-Year 0.67 Yield 10/05/20 0.09 0.56 1.13 Yield 10/06/20 0.10 0.60 1.20

Step by Step Solution

3.42 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

a Under the Expectations Theory the expected 1year interest rates implied by the 100520 yield curve ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Core Concepts

Authors: Raymond M Brooks

2nd edition

132671034, 978-0132671033